The Fed’s Balancing Act: Why Market Liquidity Matters More Than Interest Rates

Words: 1,250 Time: 6 Minutes

- Quantitative Tightening (QT): The silent driver of asset volatility.

- The "Neutral" Mirage: Why finding the right rate is a guessing game.

- Liquidity vs. Inflation: The Fed"s high-stakes dual mandate.

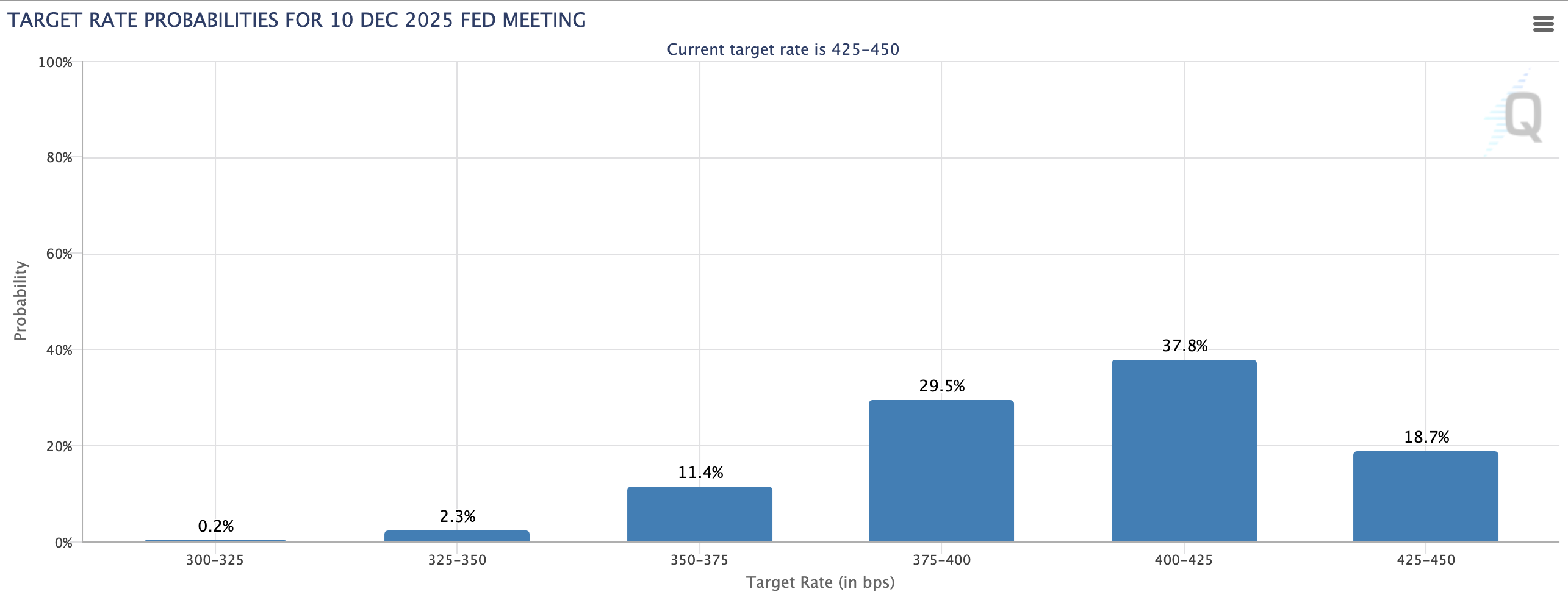

The financial headlines are usually dominated by one question: "Will they cut or will they hold?" While interest rates are important, they are only one part of the monetary plumbing. The more critical, and often overlooked, factor is liquidity—specifically, the pace at which the Federal Reserve reduces its massive balance sheet.

The Liquidity Lifeblood

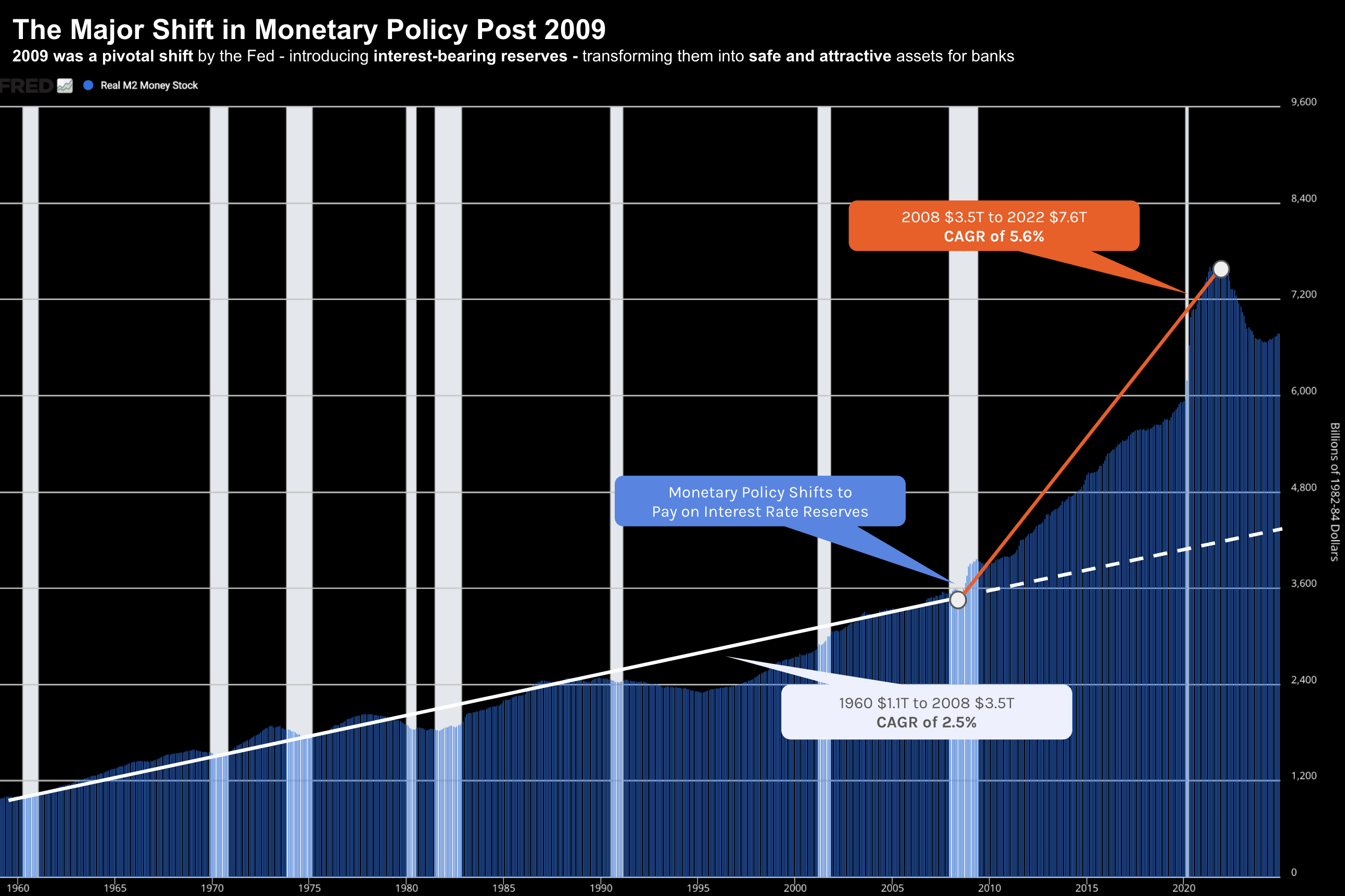

Quantitative Tightening (QT) is the process of the Fed shrinking its balance sheet by allowing bonds to "run off" without reinvesting the proceeds. In plain English: it pulls money out of the system. This is intended to cool inflation by ensuring less cash is chasing goods, but it also removes the "cushion" that has supported asset prices for over a decade.

Over the last 15 years, the growth of the S&P 500 has almost perfectly mirrored the expansion of the Fed"s balance sheet. When the "spigots" are open, assets rise; when they tighten too aggressively, we risk a "liquidity crunch."

A "Perfect Storm" for the Consumer?

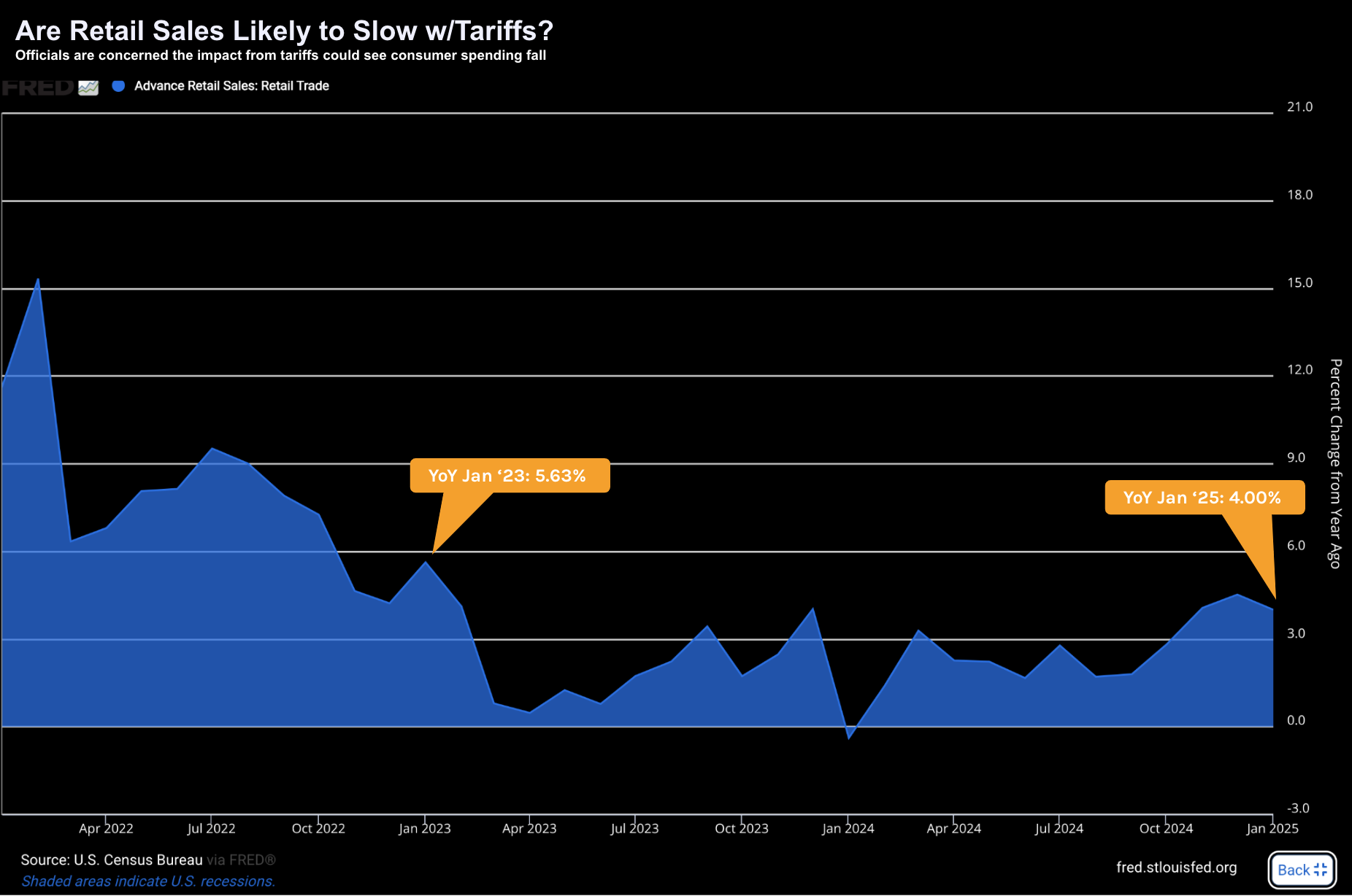

The challenge for the Fed is timing. If they tighten too quickly while the economy is facing external shocks—such as new tariffs or shifting trade policies—they risk a "perfect storm." We are already seeing early warning signs in retail data and corporate guidance, suggesting the consumer is starting to feel the pinch of higher borrowing costs and reduced circulating capital.

When Fed officials express "uncertainty" about balance sheet reduction, they are essentially admitting that they don"t know where the "floor" for liquidity is. Tightening until something breaks is a dangerous strategy, and the memory of the 2019 repo market spike remains a cautionary tale for the committee.

The Pivot to Value

If the Fed chooses to pause or slow QT, it creates a shift in market leadership. While high-flying tech names are sensitive to rates, sectors like Energy, Materials, and Consumer Staples often react more directly to changes in broad system liquidity. We are already seeing "value" start to outpace "growth" as investors anticipate a more cautious Fed stance.

- Energy & Materials: Often benefit from a "looser" monetary environment and a stable dollar.

- Consumer Staples: Provide a defensive moat if the "growth scare" becomes a reality.

The Hard-Hitting Reality: No Free Lunch

The Fed"s primary mandate is to maintain price stability and full employment. If inflation remains stubbornly above the 2% target, the Fed is effectively "boxed in." They cannot easily add liquidity back into the system without risking a secondary spike in prices. This is why the "victory laps" we see from policy makers are often premature—inflation is a "sticky" problem that doesn"t resolve in a straight line.

Conclusion: Watch the Plumbing, Not the Headlines

As an investor, your job isn"t to predict the next 25-basis-point move. Your job is to understand the positioning of the market. If the Fed is forced to pause QT to support a flagging economy, it may provide a temporary tailwind for stocks, but it also signals that the underlying economic engine is struggling.

Keep your "dry powder" ready. The most attractive valuations often appear when liquidity is tightest and the crowd is rushing for the exits. To understand how I apply this macro view to individual stock selection, read my recent breakdown: "Quality and Value: Defining the Strike Zone."