AI Infrastructure ROI: Why Investors are Questioning the $1 Trillion Capex Cycle

Words: 1,565 Time: 6 Minutes

- The Infrastructure Dilemma: High capex vs. uncertain returns.

- Valuation Sensitivity: Why high-quality businesses can still be poor investments.

- The Paradigm Shift: Lessons from the 1990s tech reset.

Since the emergence of sophisticated Large Language Models (LLMs) in late 2022, the global markets have focused intensely on Artificial Intelligence (AI). This enthusiasm is logical; AI is set to transform productivity and problem-solving over the coming decades. However, for investors, the primary concern has shifted from "What can it do?" to "What is the Return on Invested Capital (ROIC)?"

The poster child for this era has been Nvidia (NVDA). With an unparalleled lead in GPU architecture, the stock has seen historic gains. Yet, as the long-term chart demonstrates, the stock traded sideways for years prior to the current AI catalyst. The question now is whether the current growth trajectory is sustainable or a byproduct of a massive, one-time infrastructure build-out.

Recent market volatility, sparked by lower-cost international competitors like DeepSeek, highlights a critical vulnerability. If sophisticated models can be developed more cost-effectively than previously thought, it raises questions about the sustainability of U.S. AI infrastructure investments, which are forecast to exceed $1 Trillion annually.

Consider the scale of the 2025 projected capex:

- Microsoft: Projecting $80B for data center infrastructure.

- The Stargate Initiative: A collective $500B investment led by OpenAI, Oracle, and SoftBank.

- Meta: Forecasting up to $65B in annual spend.

- Google & Amazon: Estimated $60B to $80B each in infrastructure investment.

The Importance of Challenging Valuations

Savvy investors don"t need a specific market event to question the long-term Return on Invested Capital (ROIC). When you pay a lofty premium for a stock, you are implicitly assuming that current investments will be exceptionally profitable for years to come. You are betting on a greater return on the incremental capital being put to work.

When applying a 5-year discounted cash flow (DCF) model for NVDA, even aggressive assumptions—such as 40% revenue growth and 35% net income margins—result in an intrinsic value significantly below the peak market prices. This demonstrates how sensitive these valuations are to assumptions about future competition and margin compression.

Inversion Question #1: What if the $1 Trillion being spent on AI infrastructure is not "growth capital" but "defensive capital"? If companies are spending billions just to maintain their existing market share rather than create new revenue streams, the ROIC will be significantly lower than the market currently expects.

Microsoft: Quality vs. Price

Microsoft (MSFT) remains one of the highest-quality businesses globally. However, the risk for investors lies in the valuation, not the business model. You can lose a significant amount of capital buying a great company if you pay a price that leaves no margin for error.

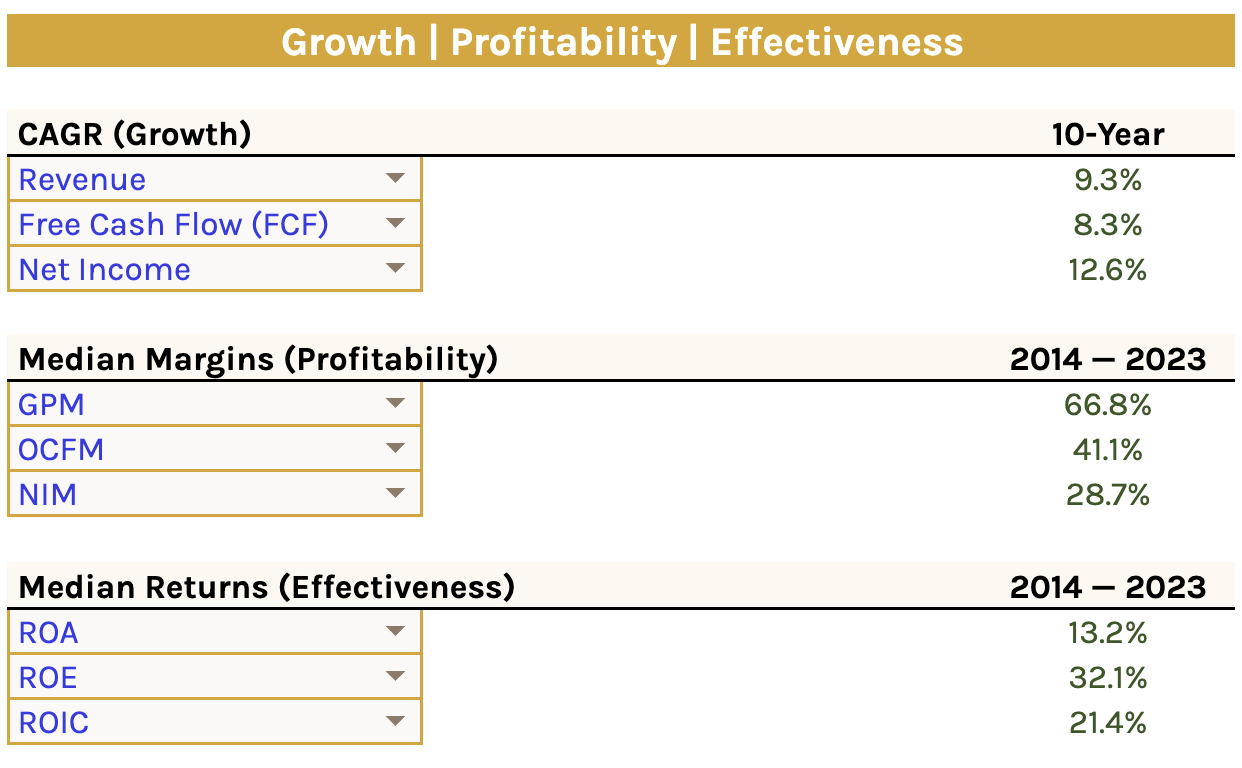

The 15/15 Rule and Quality Metrics

To evaluate these giants, I utilize the 15/15 Rule. This framework looks for companies that consistently deliver a 15% Return on Equity (ROE) and a 15% Return on Invested Capital (ROIC). ROE measures how efficiently a company handles shareholder money, while ROIC measures the return generated on all capital (debt and equity) used by the business. When a company meets this threshold, it proves it has a durable competitive advantage—or "moat."

Microsoft"s 10-year averages are stellar: a 21.4% average ROIC and an operational cash flow margin of 41.1%. It is a "cash machine." But does that justify its current price?

The Valuation Gap

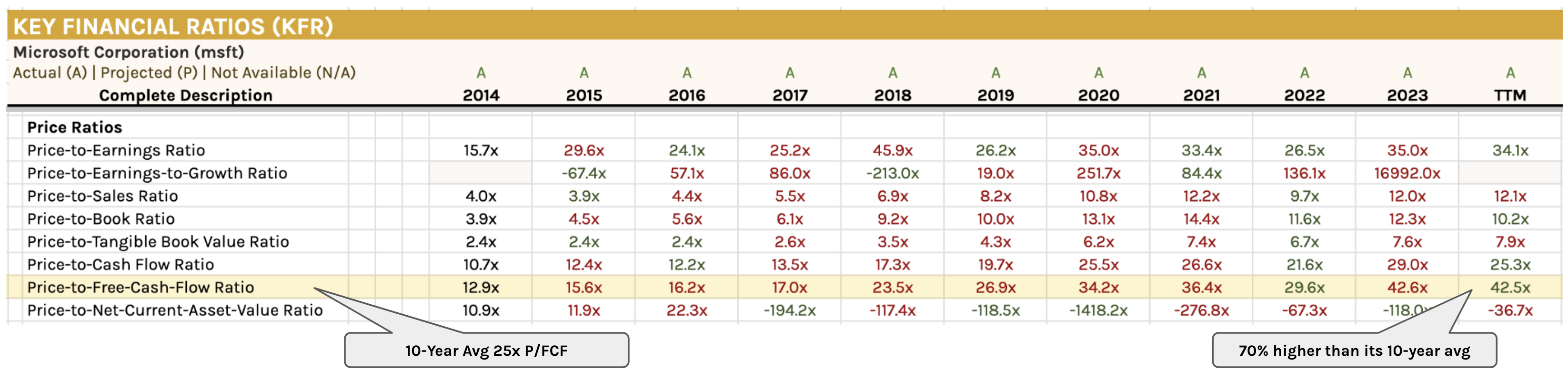

Historically, MSFT"s Price to Free Cash Flow (P/FCF) averages ~25x. Recently, it has traded above 40x, representing a Free Cash Flow yield of just 2.3%. For an investor seeking a margin of safety, a yield closer to 4-5% (or a P/FCF of 20-25x) is more appropriate.

Inversion Question #2: If we assume Microsoft"s cloud gross margins (which recently decreased to 70%) continue to contract due to high AI operating costs, what happens to the stock"s "quality" status? If the 15/15 rule is breached, is the stock still an "automatic" buy?

Market Momentum and the S&P 500

The broader market (S&P 500) faces resistance at high valuations (roughly 22x forward earnings). We are seeing negative divergence in technical indicators like the RSI and MACD, suggesting that the "Bulls" are losing momentum. A healthy correction of 10-15% would bring the index closer to 18x forward earnings, providing a more reasonable entry point for long-term capital.

Putting it All Together

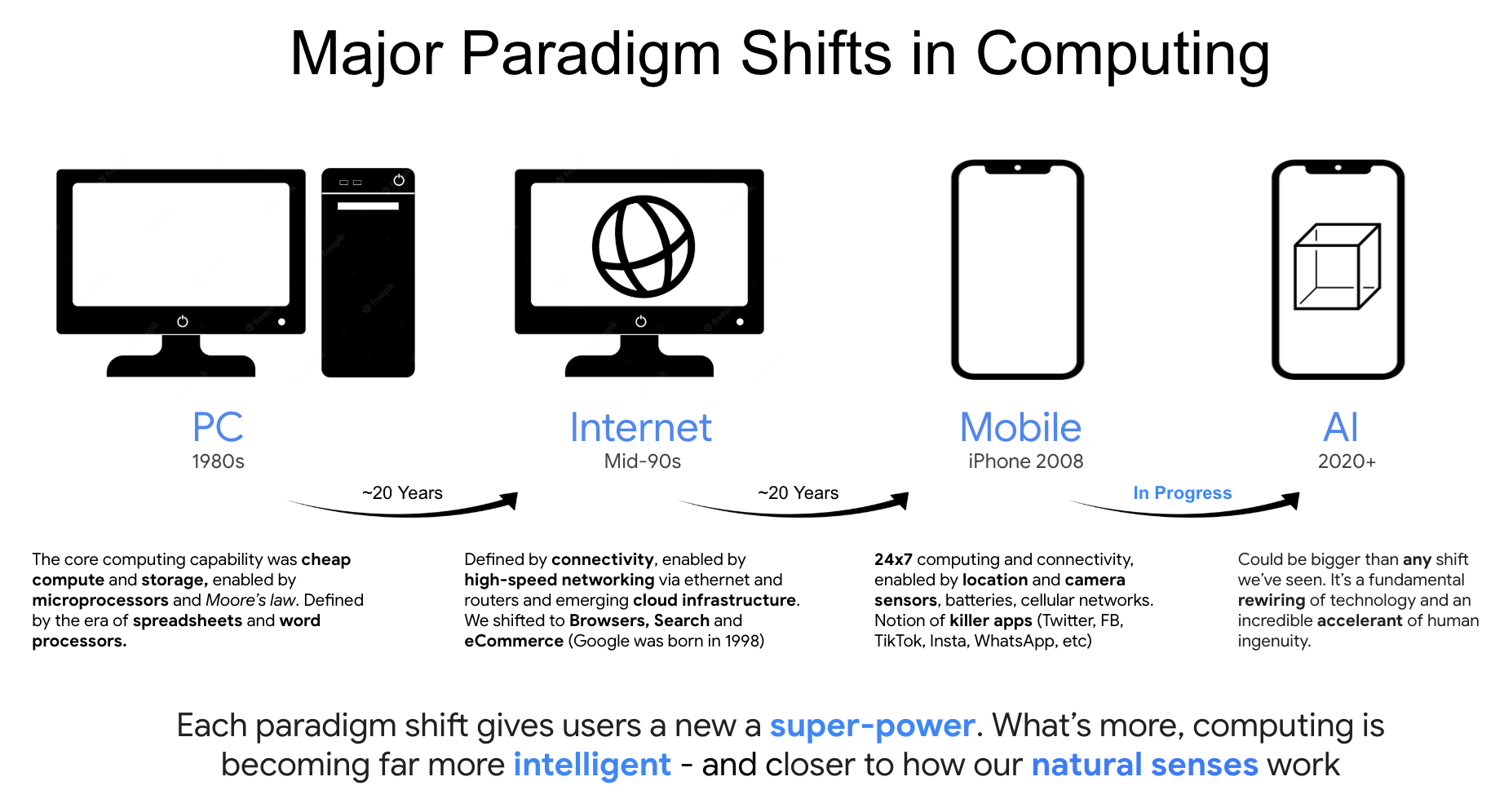

The current AI trade mirrors the internet boom of the mid-1990s. While the internet did eventually transform the world, it took over a decade for its true potential to manifest as sustainable corporate profits. Many of the early leaders in that era soared on promise only to face a harsh reality check in 2000.

Inversion Question #3: We focus on the risk of paying too much. But what if the "DeepSeek" effect means the barriers to entry in AI are actually lower than expected? If the tech becomes a commodity, which businesses actually capture the value? (Hint: Usually the ones *using* the tech, not the ones *building* it).

We are still in the early stages of finding product-market fit for AI. Because we cannot predict the next technological disruption, investors must remain mindful of the risks that come with overpaying for growth. Paradigm shifts take time, and a disciplined approach to valuation—anchored by metrics like ROIC and the 15/15 Rule—is the best way to survive the cycle.