A Reactive Fed: Why Trade Policy Now Dictates Interest Rate Volatility

Words: 1,407 Time: 6 Minutes

- The Federal Reserve warns that risks to both employment and inflation have shifted higher.

- Policy Uncertainty: Why the Fed has moved from a proactive to a reactive stance.

- The "Three Pillar" Challenge: Calibrating the impact of tariffs, tax cuts, and deregulation.

What currently dictates market direction:

- Policy shifts announced via social media regarding trade deals; or

- The formal statements on monetary policy from the Federal Reserve?

Currently, the market is proving far more sensitive to the former.

The latest statement from the Federal Reserve was largely a non-event for price action. While Chair Powell maintained interest rates in the 4.25% to 4.50% target range as expected, his commentary revealed a significant shift in the internal risk assessment.

Powell noted that the risks of "higher unemployment and higher inflation" have risen simultaneously since the last FOMC meeting. This creates a policy dilemma: rising unemployment typically necessitates lower rates, while the threat of persistent inflation above the 2% target could require further tightening.

The market is currently pricing in a high probability of easing, with 75 basis points of cuts expected by year-end. However, the probability of a cut in the immediate next meeting remains low at roughly 20%.

The logic is simple: why would the Fed commit to a move before the current tariff pause expires on July 8?

Powell was firm in dismissing preemptive action while inflation remains above target:

"It"s not a situation where we can be preemptive, because we actually don"t know what the right responses to the data will be until we see more data."

This marks a fundamental shift. We are no longer dealing with a proactive Fed that attempts to get ahead of the curve. Instead, we have a reactive Fed forced into a "wait-and-see" posture by external trade policy.

Furthermore, if the economy requires three or four rate cuts this year, that should be viewed as a warning sign rather than a catalyst for growth. Such aggressive easing would imply a significant structural breakdown in economic activity.

As Powell attempts to balance the risks of recession versus inflation, the energy markets are already signaling a slowdown. Crude oil prices have sunk to levels not seen since 2021, falling below $60/b, which typically suggests a cooling of global demand.

The Search for Policy Optionality

Maintaining optionality is currently the Fed"s only viable strategy. To commit to a specific path now would be premature given the volatile geopolitical landscape. While growth is clearly moderating, the risk of an inflation shock remains potent.

When the Fed mentions "higher unemployment and higher inflation" in the same breath, they are describing the early stages of stagflation—a condition where stagnant demand meets persistent price increases. While the current 4.2% unemployment rate remains healthy, the path forward is clouded by trade policy.

If new trade barriers result in baseline tariffs above 20-30%, the U.S. could face a direct inflationary shock. A move toward "deglobalization" and mercantilist trade policies inevitably raises the cost of goods, an economic burden ultimately carried by the domestic consumer.

Analyzing the Three Pillar Strategy

The current administration"s strategy for achieving 3.0%+ GDP growth centers on three primary pillars: tariffs, tax cuts, and deregulation. While the goal is robust growth, the market faces a significant calibration problem. It is difficult for investors to measure the net impact when the variables are constantly shifting:

- What is the final "equilibrium" level for tariffs after negotiations?

- What is the true scope of tax cuts that can realistically pass through Congress?

- How deep will deregulation go, and how quickly will it impact the bottom line?

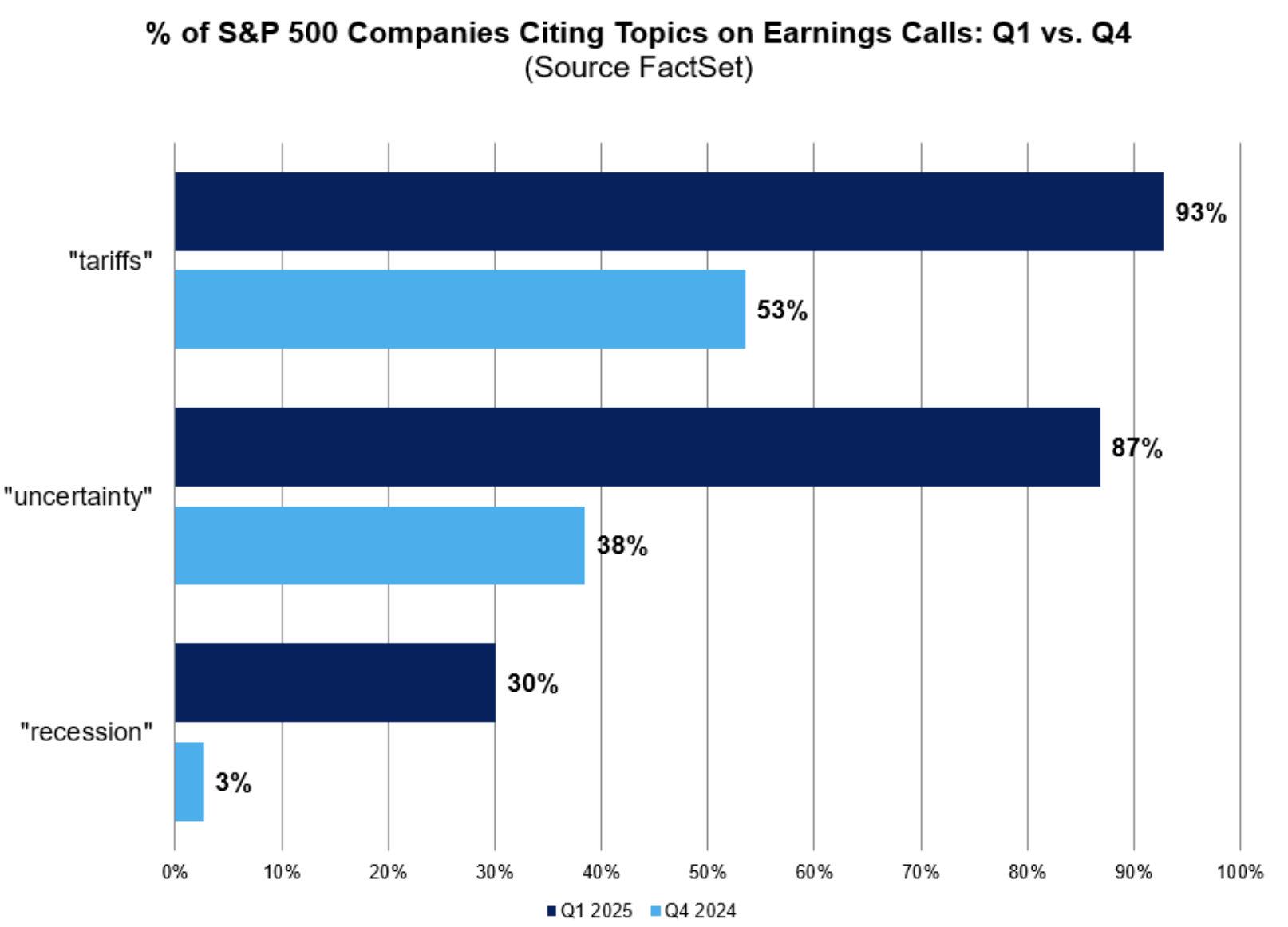

The primary concern for corporate leadership remains the uncertainty surrounding trade costs. Factset"s review of Q1 earnings calls confirms that trade barriers are the top concern for management teams across the S&P 500.

Warren Buffett noted the risks of aggressive protectionism during his recent shareholder meeting, suggesting that a strategy that alienates global trading partners can have long-term unintended consequences.

While there are legitimate concerns regarding fair trade and intellectual property, tariffs are not the only tool available. Policymakers could also focus on:

1. Surgical Export Controls: Tightening restrictions on sensitive and dual-use technologies.

2. Strategic Investment Screening: Reviewing and potentially blocking foreign investment in critical infrastructure and strategic land acquisitions.

3. Multilateral Countermeasures: Working within international frameworks to challenge subsidies and trade violations.

The fundamental issue with broad-based tariffs is that they act as a regressive sales tax. They increase the cost of living for the very people they are intended to help. While protectionist measures may offer minor wins for specific manufacturing sectors, they are unlikely to move the needle for the broader economy.

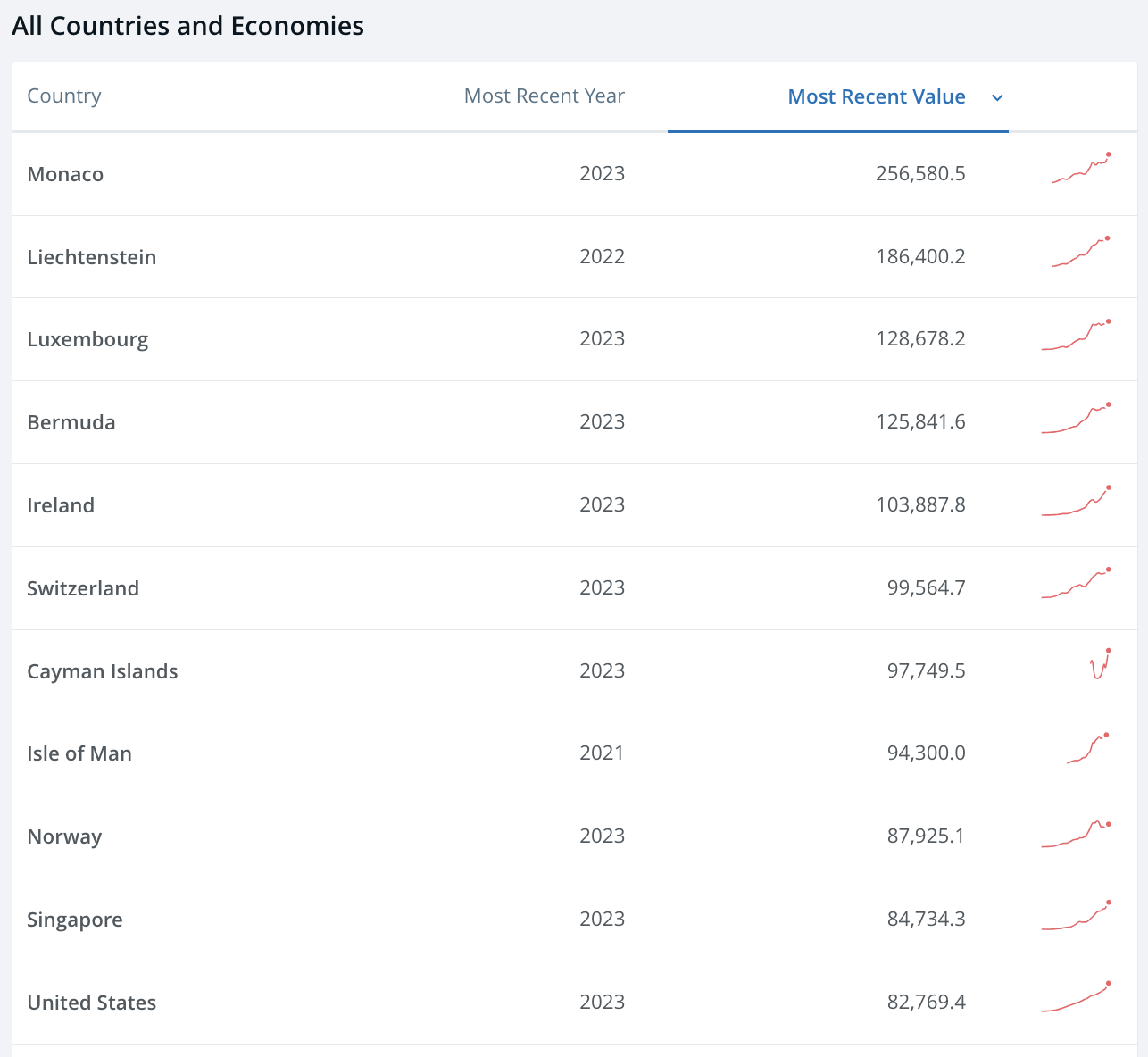

U.S. manufacturing currently accounts for only 5% of the workforce. The United States has successfully transitioned into a knowledge-based economy, which is why it maintains one of the highest rates of GDP per capita globally.

By comparison, China generates approximately US$12,614 per capita, reflecting its role as a manufacturing hub. High-value "knowledge work" yields significantly higher income levels than high-volume manufacturing. For the U.S. to focus on competing for low-margin factory work like apparel or basic electronics would be a move down the value chain.

While it is strategic to locally produce sensitive goods—such as national security components and pharmaceuticals—the U.S. benefits from letting lower-cost nations handle the production of general consumer goods. This allows American capital and labor to focus on intellectual property and innovation, where the margins and wages are far higher.

Strategic Outlook

The Federal Reserve"s cautious, reactive tone is the only logical response to the current policy landscape. Chair Powell is essentially "on hold" until the trajectory of trade policy becomes clearer.

Markets will remain hypersensitive to the risk of recession and the potential for higher unemployment unless concrete trade agreements are reached before the July 8 deadline. Until then, investors should expect bond and equity markets to take their cues from social media updates rather than the formal deliberations of the FOMC.