AI Capex vs. ROIC: Why Investors are Questioning Big Tech’s $1 Trillion Bet

Words: 1,762; Time: 7 Minutes

- Strategic Evolution: Why focusing on business quality matters more than ticker symbols.

- The DeepSeek Catalyst: How a low-cost model challenged Big Tech"s "infinite moat" theory.

- The Network Effect Fallacy: Why AI users don"t scale value like social media users.

You may have noticed a structural shift in my digital home. Tradethetape has officially transitioned to adriantout.com. Since 2011, my objective has remained constant: exploring the macro landscape and analyzing economic policy to make smarter, lower-risk investing decisions. I felt the old moniker didn"t fully capture the depth of analyzing a company"s financial condition—the ultimate arbiter of value.

In the world of investing, if there is a single factor crucial in determining long-term success, it is the quality and quantity of a firm"s resources. Market sentiment is fleeting, but a business with considerable financial strength and flexibility can create future wealth that eventually manifests in earnings and, ultimately, price. Today, that flexibility is being tested by a massive surge in Artificial Intelligence (AI) expenditure.

The DeepSeek Disruption and the Capex Explosion

Recently, the investment community began a serious pivot, moving from "AI excitement" to questioning Return on Invested Capital (ROIC). To understand the scale of this concern, look at the projected 2025 infrastructure spends for the "Magnificent 7":

- Microsoft: Projecting $80B for data center expansion.

- The "Stargate" Initiative: A collective $500B investment involving OpenAI, Oracle, and SoftBank.

- Meta: Forecasting up to $65B in annual capex.

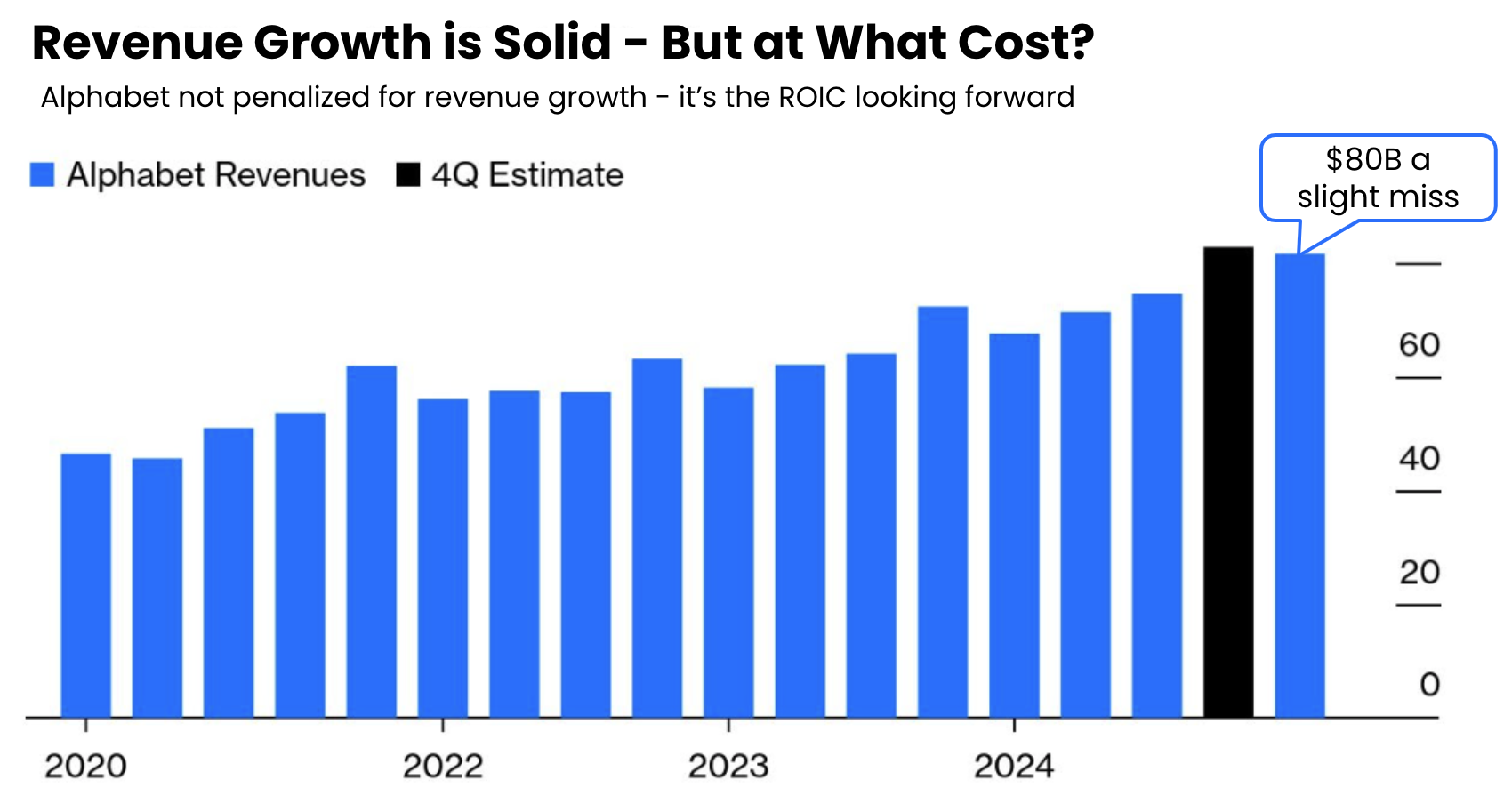

- Alphabet (Google): Recently committed $75B, significantly above initial market expectations of $50B.

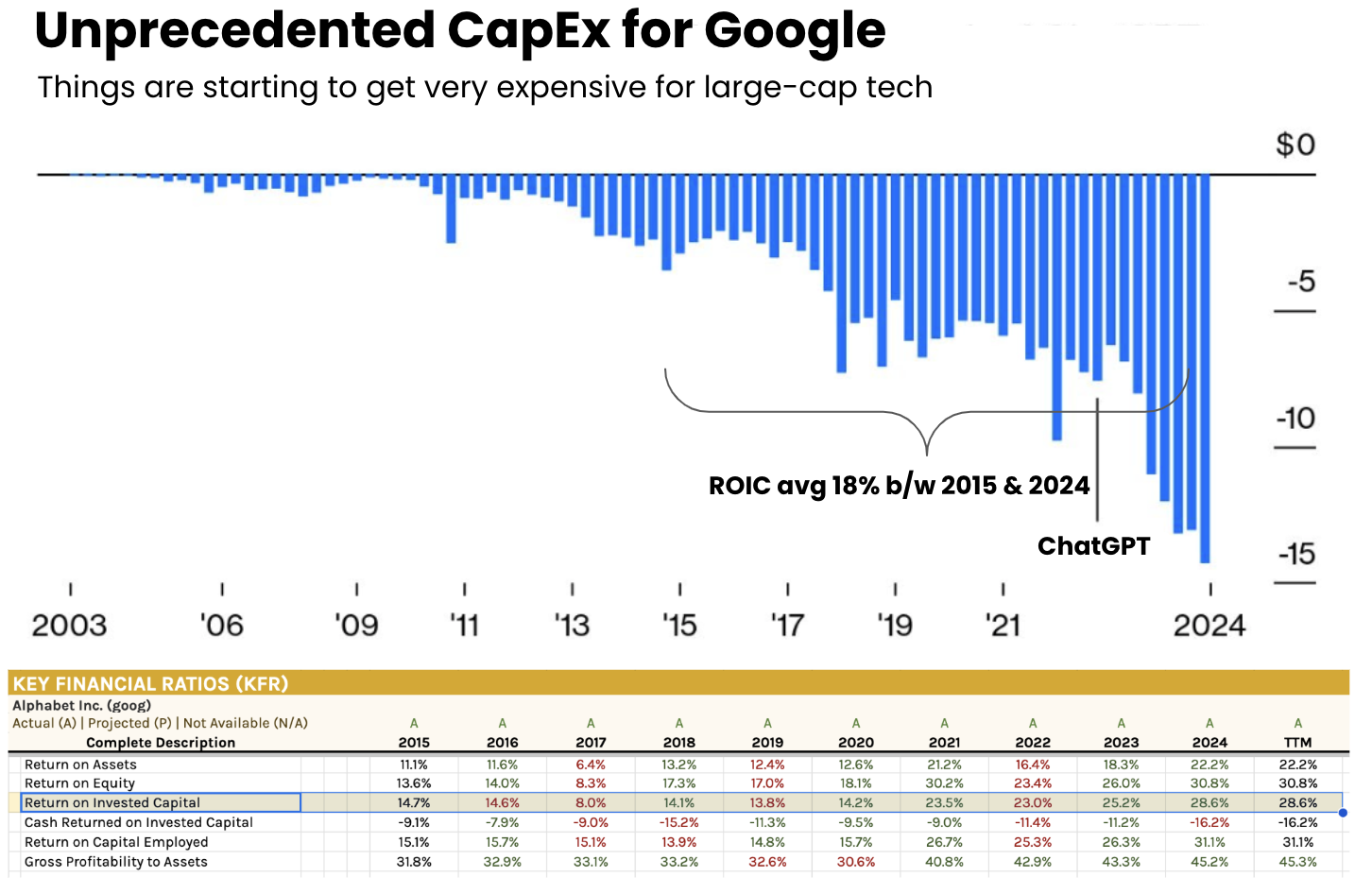

The core of the "Google problem" identified by analysts is two-fold: First, is the return on AI investment as apparent as it is in Meta"s core advertising business? Second, is the sustainability of Search growth threatened? When capex explodes, the ROIC—which for Google averaged 18% between 2015 and 2024—comes under immense pressure.

Inversion Question #1: What if this massive capex isn"t an "investment" for growth, but a mandatory "maintenance cost" just to prevent existing business moats from being breached by new competitors? If so, should these companies still trade at "growth" multiples?

Challenging the "Limitless Resource" Assumption

Before the emergence of DeepSeek, it was assumed that Big Tech"s deep pockets created an unassailable moat. But if a sophisticated Large Language Model (LLM) can be developed at a fraction of the cost, the "moat" might be shallower than investors paid for. We must ask: If LLMs can be commoditized, will the same disruption happen in Computer Vision, Robotics, or Cyber Security? If development costs collapse, the premium paid for "early movers" like Microsoft (44x P/FCF) or Google (32x P/FCF) may be at risk.

Why More Users May Not Mean More Value

In previous tech cycles, we relied on Network Effects—the idea that a platform becomes more valuable to every user as more people join (think Facebook or iOS). However, AI models like ChatGPT or DeepSeek do not necessarily follow this rule. The utility of a model for an individual user remains largely the same whether one million or one billion people are using it. In fact, because these models are extremely expensive to operate (energy and chips), a larger user base can actually reduce profitability if monetization doesn"t scale linearly.

Inversion Question #2: If AI utility doesn"t grow with the user base, does the "first-mover advantage" even exist, or will the "second-movers" (who don"t have to pay the $1T in R&D "tuition") eventually capture all the profit?

The 15/15 Rule: A Filter for Sanity

To navigate this uncertainty, I apply the 15/15 Rule. This is a disciplined filter requiring a company to maintain a 15% Return on Equity (ROE) and a 15% Return on Invested Capital (ROIC).

This rule is highly relevant to the AI debate because it separates "busy-ness" from "business." ROE tells us how effectively management is using shareholder funds, while ROIC tells us if the massive capex (like Google"s $75B) is actually generating a return higher than the cost of that capital. If a company"s ROIC begins to trend toward its cost of capital (as we see in the capital-intensive airline industry), it ceases to be a high-quality compounder and becomes a "value trap."

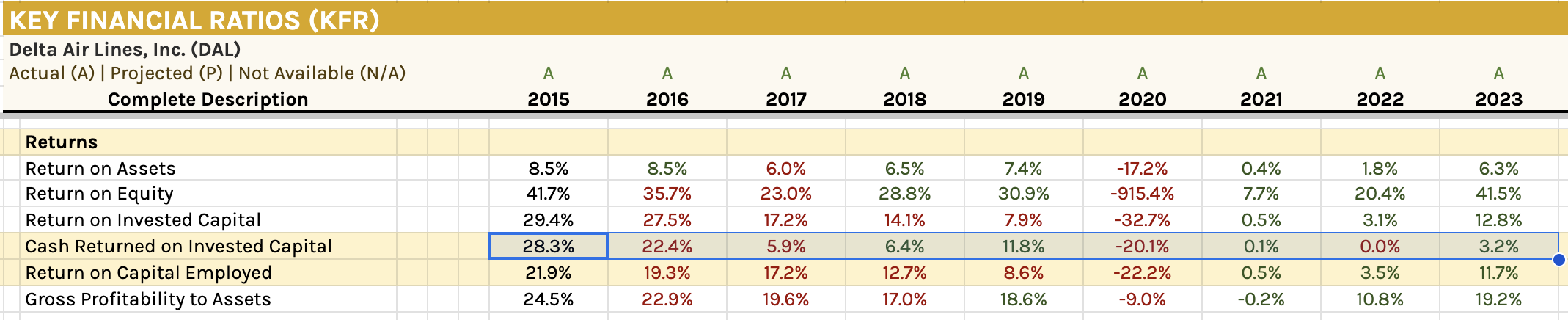

Consider Delta (DAL). Despite being well-run, its ROIC is often in the mid-single digits. There is no room for error. When Big Tech starts spending like an airline or a utility provider, investors must ensure they aren"t paying "SaaS multiples" for "industrial-heavy" business models.

Summary: The Price of Optimism

Inversion Question #3: We are focused on the risk of losing money on AI. But what is the risk of not spending? If a company like Amazon stops its $60B capex while competitors continue, do they become the next Kodak or Nokia? Is "reckless spending" actually the only "safe" path?

I personally welcome the advent of open systems like DeepSeek. Innovation thrives in the open. However, as a risk-averse investor, it pays to remember that tech moats can evaporate overnight (just ask the former leaders at BlackBerry or Palm). When the divergence between price and value becomes too great, the safest move is often to watch from the sidelines until valuations return to historical averages. In the end, your risk isn"t defined by the technology—it"s defined by what you pay for it.