Consumer Confidence Sinks: Be Wary of this Market Bounce

Words: 1,119 Time: 5 Minutes

- Confidence falls off a cliff… I wonder why?

- Keep your eye on the quarterly YoY change in Real PCE.

- Stocks caught a bid today—but nothing fundamental has changed.

It was a roller-coaster week for stocks… maybe a hint of things to come?

As part of my "Buckle up Buttercup" post on March 10th, I concluded with:

The pathway down won"t be a straight line… expect many periods of sharp buying. In fact, I think we will see that soon.

Right on cue, the market bounced. From my perspective, in the very short term, markets were deeply over-sold looking at the Relative Strength Index (RSI). Often, when you see the RSI below a value of 30, buying isn"t too far away.

The last time stocks sank ~10% over a few days was 2020. However, in the absence of a systemic crisis, violent drops generally invite short covering and bargain hunting. The bigger question is whether stocks can follow through.

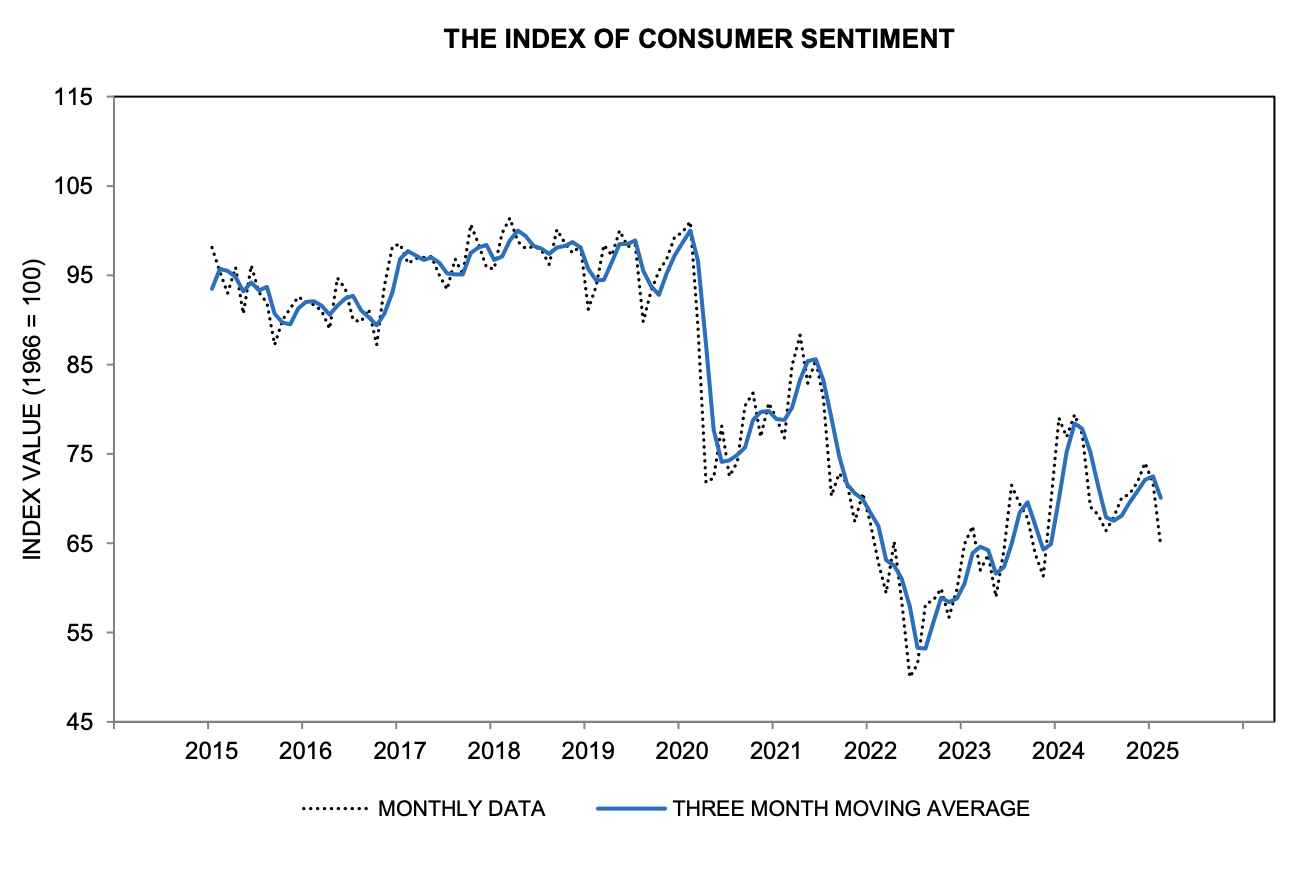

I don"t think we can draw that conclusion yet, although the financial media already is. But first, let"s look at the all-important University of Michigan Consumer Confidence survey that hit the tape today. It sank.

Confidence Plunges

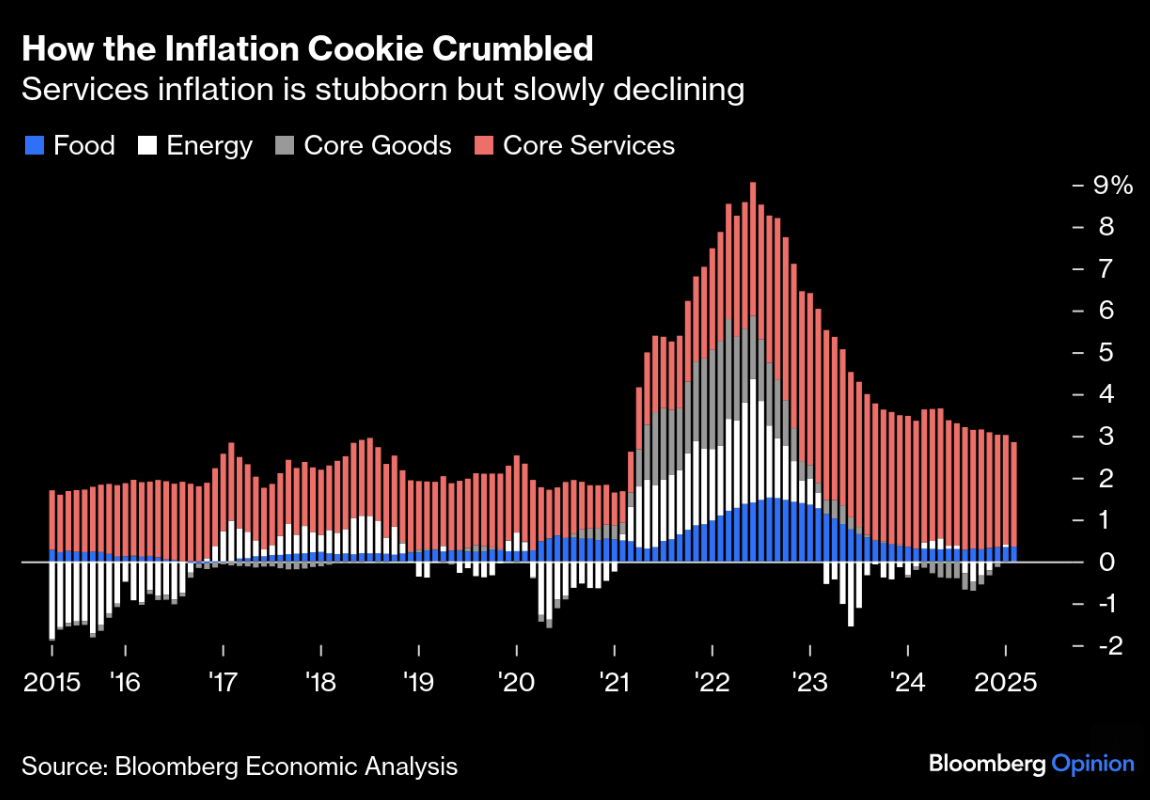

Regular readers will recall I was more interested in the University of Michigan Consumer Sentiment Index than the CPI. CPI came in largely as expected, with Core CPI still above 3.0%. Markets were not moved.

Inflation is proving very sticky, and it is entirely driven by services. Energy, food, and core goods have reverted to normalized levels. However, wages and rents are far stickier and will take longer to come down. Yes, prices are falling, but at a glacial pace. It"s still at a level that"s too high for the Fed"s comfort—and well above pre-COVID levels.

With respect to consumer confidence for March, it plunged to 57.9 from 64.7. This was a significant drop below the consensus of 63.0.

This sharp decline reflects heightened unemployment fears reminiscent of the 2007-2009 recession. And it"s not surprising. The psychological shock of potential loss is powerful. When consumers face uncertainty surrounding economic and fiscal policy—alongside falling stock prices—the reaction is swift and severe: they tighten their wallets.

If they are nervous about losing their livelihoods, watch for consumption growth to slow dramatically during the first quarter. To me, that is a bigger risk than inflation and tariffs put together. Let me explain why.

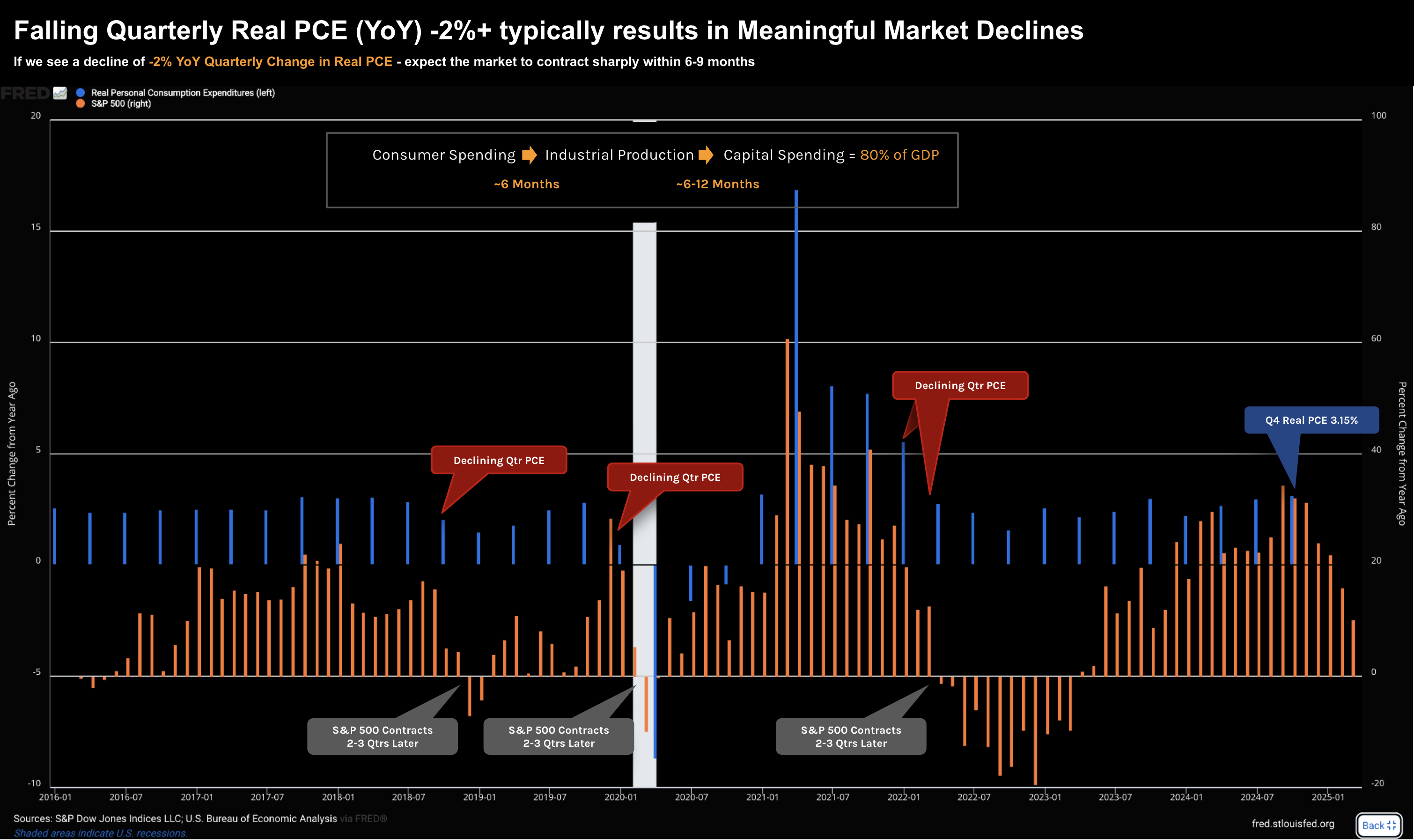

Watching the Change in Real PCE

If you"re a long-term reader, you know my preferred leading economic indicator is measuring the yearly change in Real Personal Consumption Expenditure (PCE) on a quarterly basis. It"s not employment, industrial production, or capital spending.

The reason is reason-respecting logic: it all starts with the consumer and how much they are spending.

At the end of the day, consumer spend drives company profits. With company profits, we get further business investment. This drives greater output, which in turn leads to more employment, and the cycle continues. Therefore, what we see with consumption (which is a direct function of confidence) is critically important.

To be clear, understanding the trend in Real PCE is not a panacea. Many factors influence the market in the short term, including investor sentiment (fear and greed), geopolitics, policy shifts, and valuation multiples. However, over the long-term, the market prices a company"s ability to generate earnings.

Between 2016 and 2024, I"ve labeled three occasions where the YoY % change in Real PCE fell by more than 2% on a quarterly basis. On each occasion, the market plunged 6-12 months later. I"ve run this analysis back to ~1960, and the relationship holds true.

The most recent quarterly Real PCE data (Q4 2024) showed growth of 3.15%. That growth had been increasing, supporting earnings and higher stock prices. Now, I will be watching to see if Q1 2025 growth drops below 1.15% year-over-year in real terms.

If we see a quarterly decline of at least 2.0%, I will forecast a sharp slowdown in growth. And here is the reality: we don"t need to experience an official recession to see stocks decline by 20% or more. We saw a sharp slowdown in consumption at the end of 2021, and stocks went on to lose ~20% in 2022.

Stocks Catch an (Expected) Bid

With stocks deeply oversold in the very short-term, a sharp bounce was inevitable. As it turns out, today was that day. But as the saying goes, "one hot night doesn"t make a summer."

Through my lens, not much has changed on the weekly chart. This was the fourth consecutive negative week, but the weekly RSI is not yet in oversold territory (currently ~41, and I prefer closer to 30). I"m sure bargain hunters stepped in today trying to pick a bottom. I wasn"t one of them. We must guard against the recency bias that assumes every dip is immediately bought to new highs.

The market could rally further, but I need to see the S&P 500 close back above the 35-week EMA (around 5800) and hold that level. I"m not holding my breath.

Putting it All Together

The other week, I warned readers about the folly of forecasting. The average EOY consensus was 6617—about 18% higher from here. The most bearish forecast was 6000 from Cantor Fitzgerald, who is currently looking smart.

Here is my prediction: watch for Wall Street to quietly walk these optimistic targets backward. It highlights exactly why 12-month price targets are largely twaddle.

This week, David Kostin, chief US equity strategist at Goldman Sachs, announced a revision from 6,500 to 6,200. That didn"t take long, David! Less than 3 months? He also reduced earnings estimates, now expecting 7% growth in profits this year, down from 9%.

This perfectly illustrates the danger of over-optimism. Kostin won"t be alone. These institutions operate with a herd mentality. Expect one quiet revision lower after another as reality forces their hands.

By sticking to our circle of competence and relying on objective checklists rather than Wall Street"s guesswork, we remain "10 steps" ahead.