Why This Market Correction May Not Be Finished Yet

- Valuations high despite rising geopolitical and inflation risks

- Multiple compression likely as energy shocks lift discount rates

- Patience preserves capital until repricing or resolution occurs

Markets are under pressure.

But not enough…

Despite recent weakness, equities remain within ~10% of their all-time highs.

At the same time, they continue to trade ~20x forward earnings — a level that leaves very little room for error.

This is the tension.

For example, on one hand, risk is rising with:

- Geopolitical escalation (as the war broadens);

- Energy market instability;

- The prospect of higher-for-longer rates to fight inflation

On the other hand, valuations still reflect a relatively benign outcome.

That gap — between rising risk and only partially adjusted prices — is where patience becomes essential for the longer-term investor.

Valuation Is Still the Anchor

Strip away the noise, and the starting point is simple:

- Over the past decade, the average forward earnings multiple for the S&P 500 is ~18x;

- Over the past 50+ years, it trends closer to ~16x.

With today"s asking price around 20x — and with the US 10-year yield pushing 4.40% — prices remain elevated against historical norms.

For example, if we assume earnings for the S&P 500 is ~$320 p/share — at 18x we get a valuation of 5,760 (~10% lower than current levels).

That implies ~2 turns of compression to reach recent norms; and ~4 turns to revert to longer-term averages.

This matters because multiple compression does not require earnings to fall.

It only requires sentiment — and required returns — to adjust.

And today — sentiment is shifting.

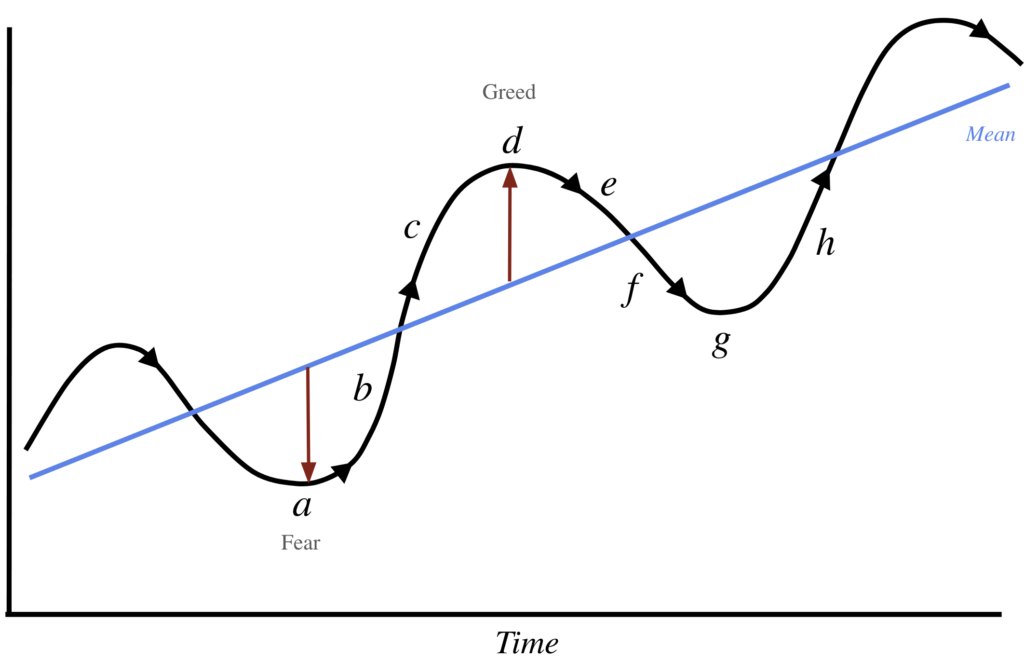

Historically, this adjustment unfolds in phases:

If I were to guess — we are around "e" on this curve.

Shifts like this are typically gradual. Markets have resisted full repricing.

That reflects positioning, expectations, and narrative inertia.

For months, investors have operated under a familiar framework:

- Policy (monetary and fiscal) support will arrive if / when needed ("Fed Put");

- Conflicts will de-escalate within a couple of weeks (not months); and

- Growth (and the American Consumer) will prove resilient

However, these assumptions are about to be tested.

From TACO to WACO

Not long ago, markets traded on "TACO" — Trump Always Chickens Out.

Today, that has shifted to "WACO" — Will the Ayatollahs Chicken Out?

So far, the answer appears to be no.

That changes the structure of the problem.

Unlike prior episodes where outcomes were largely controlled by one side, the current situation introduces a motivated counterparty with:

- Limited downside;

- Significant strategic leverage (particularly via energy markets); and

- A willingness to endure prolonged pressure (even at the expense of their people and economy)

Contrast that with the United States:

- More to lose economically and politically (e.g., Trump promised no more involvement in foreign wars);

- Limited control over the oil price in the near term; and

- Increasing pressure to resolve the conflict quickly

This asymmetry matters.

Because the Strait of Hormuz is not just a geopolitical flashpoint — it is a global economic chokepoint.

The implications are already emerging:

- Oil prices have surged 60% so far this year (a record);

- Shipping costs and insurance premiums are rising;

- Global supply chains are tightening; and

- Input costs (including fertilizers and energy-linked commodities) are also increasing

These are second-order effects. The longer the war goes – the worse it gets.

However, these risks have only been partially priced.

Right now, much of the global macro environment is collapsing into a single variable: energy.

As one strategist put it: "right now – everything is an oil trade."

That matters because oil shocks propagate quickly into:

- Inflation expectations

- Central bank policy

- Discount rates; and ultimately

- Equity multiples.

This is the critical link.

Markets are not just pricing earnings — they are pricing the rate at which those earnings are discounted.

And if energy-driven inflation persists over the coming weeks / months – the adjustment does not stop at commodities.

It moves directly into valuation.

What Hasn"t Been Priced

There is an important nuance in current pricing.

Short-term oil contracts have moved higher. Longer-dated expectations remain relatively contained.

This suggests the market still expects a quickresolution (i.e., within a couple of weeks – not months)

For obvious reasons, one hopes that proves correct.

But if that assumption is wrong — or simply delayed — the repricing is unlikely to be linear. It accelerates.

And it will not be confined to energy. It will extend to:

- Equities (via multiple compression)

- Bonds (via yields); and

- Currencies (via capital flows)

Putting it All Together

One of the defining features of prior corrections is capitulation.

Equity capitulation is where:

- Positioning clears

- Expectations reset; and

- Weak hands exit

We are not there yet.

So far this has been a controlled (orderly) decline — a slow grind lower, with intermittent rallies driven by hope of resolution.

That creates a difficult investment environment:

- Not cheap enough to be very attractive; and

- Not extreme enough to force selling

As a result, the market sits in between — vulnerable, but not yet resolved.

This is where patience stops being philosophical and becomes practical.

Because the opportunity set improves only after one of two things happens:

- Valuations compress to more attractive levels (e.g., below 18x forward earnings)

- Uncertainty resolves decisively (i.e., the United States and Iran agree to terms)

Right now, neither condition is fully met.

Therefore, if adding to positions aggressively (with markets down by approx 10%) – it introduces the same risks discussed before: capital tied up during further downside.

For me, having cash available is not idle. It is a call option on better prices.

In closing, it"s my view that valuations still remain elevated (especially given the risks).

The best opportunities rarely emerge when risk first appears. They emerge when it is fully acknowledged.