The 10-Yr Yield Challenge: The Path to Fiscal Responsibility

Words: 1,682 Time: 7 Minutes

- The Bessent Mandate: Strategic levers for lowering the 10-year yield.

- DOGE and the Fiscal Anchor: Why spending reform is the centerpiece of the transformation.

- The Inflation Balancing Act: Managing tariffs, oil, and consumer expectations.

The role of the US Treasury Secretary is increasingly defined by a single metric: the 10-year Treasury yield. Scott Bessent, with his background in global macro investing, recognizes that the 10-year yield is the "master rate" of the modern economy. Unlike the short-term rates set by the Federal Reserve, the 10-year yield dictates the actual cost of capital for the real world.

For example, the US 10-year yield determines borrowing rates for:

- Federal government debt servicing;

- Fixed-rate residential mortgages;

- Commercial car loans and student debt; and

- Small business credit lines.

The mathematical reality is that the global economy struggles to thrive with a 10-year yield materially above 5.0%. At these levels, the "gravity" of interest rates begins to pull down equity valuations, as the discount rate used to value future cash flows rises. Equities, particularly growth-oriented sectors, are not currently priced for a "higher-for-longer" environment at the long end of the curve.

Securing lower yields requires a transition to fiscal responsibility. This means a reduction in the velocity of government spending and borrowing. While spending cuts often meet political resistance from those benefiting from the status quo, the longer-term sustainability of the economy depends on narrowing the deficit. As Fed Chair Jerome Powell noted in his 60-Minutes interview, the current path of fiscal spending is simply not sustainable.

Growth vs. Fueling Inflation

The structural challenge for the Treasury is achieving robust economic growth without reigniting unwanted inflation. Two primary policy pillars—reducing immigration and imposing tariffs—act as wildcards in this equation.

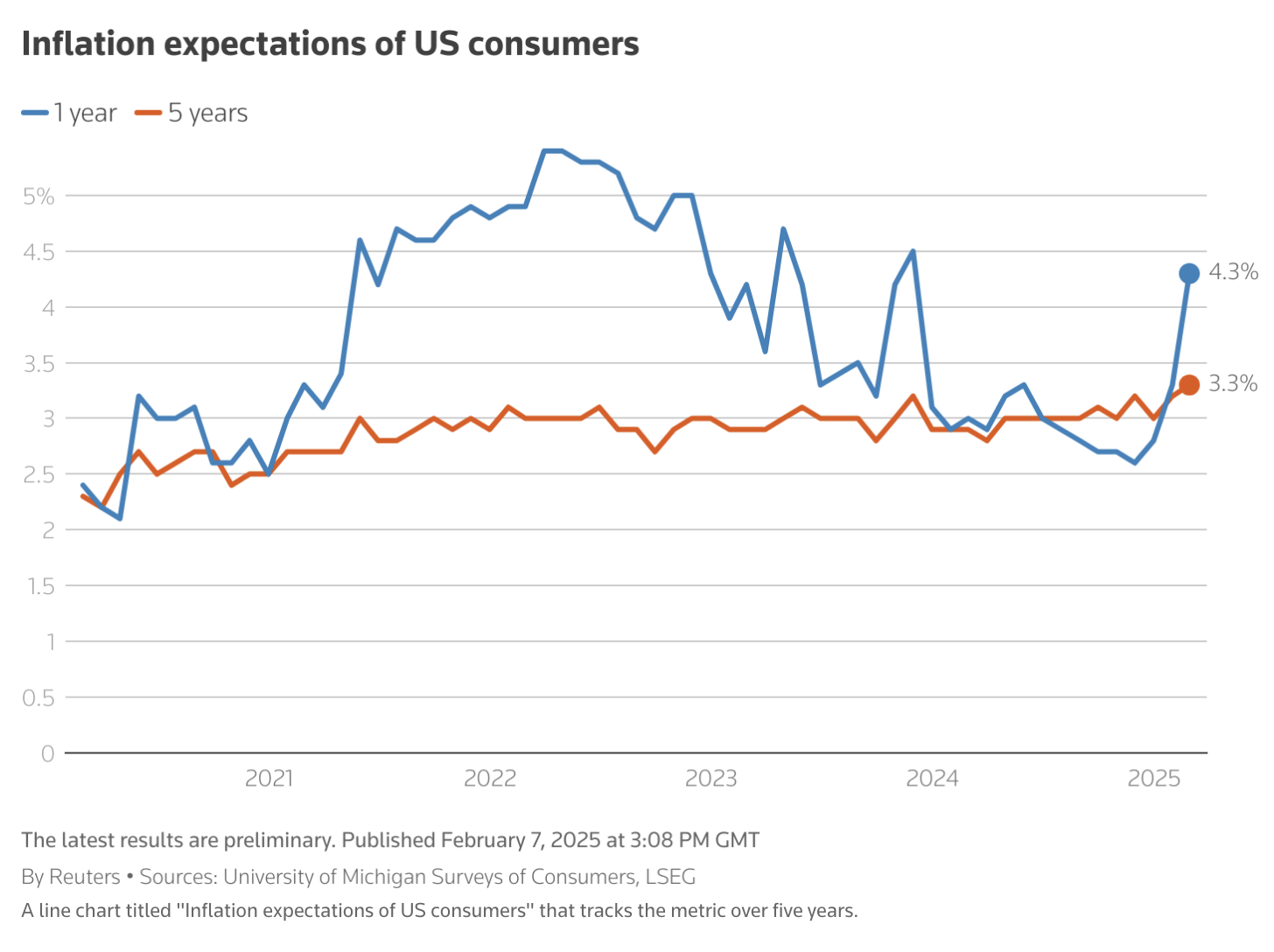

While tariffs are often utilized as a negotiating lever to gain better trade terms, their immediate implementation can lead to higher consumer prices. This sentiment was reflected in the University of Michigan consumer survey, which showed a sharp rise in inflation expectations.

"Year-ahead inflation expectations recently jumped from 3.3% to 4.3%, marking an unusually large increase. Historically, such jumps in expectations correlate with upward pressure on bond yields, complicating the Treasury"s goal of lowering borrowing costs."

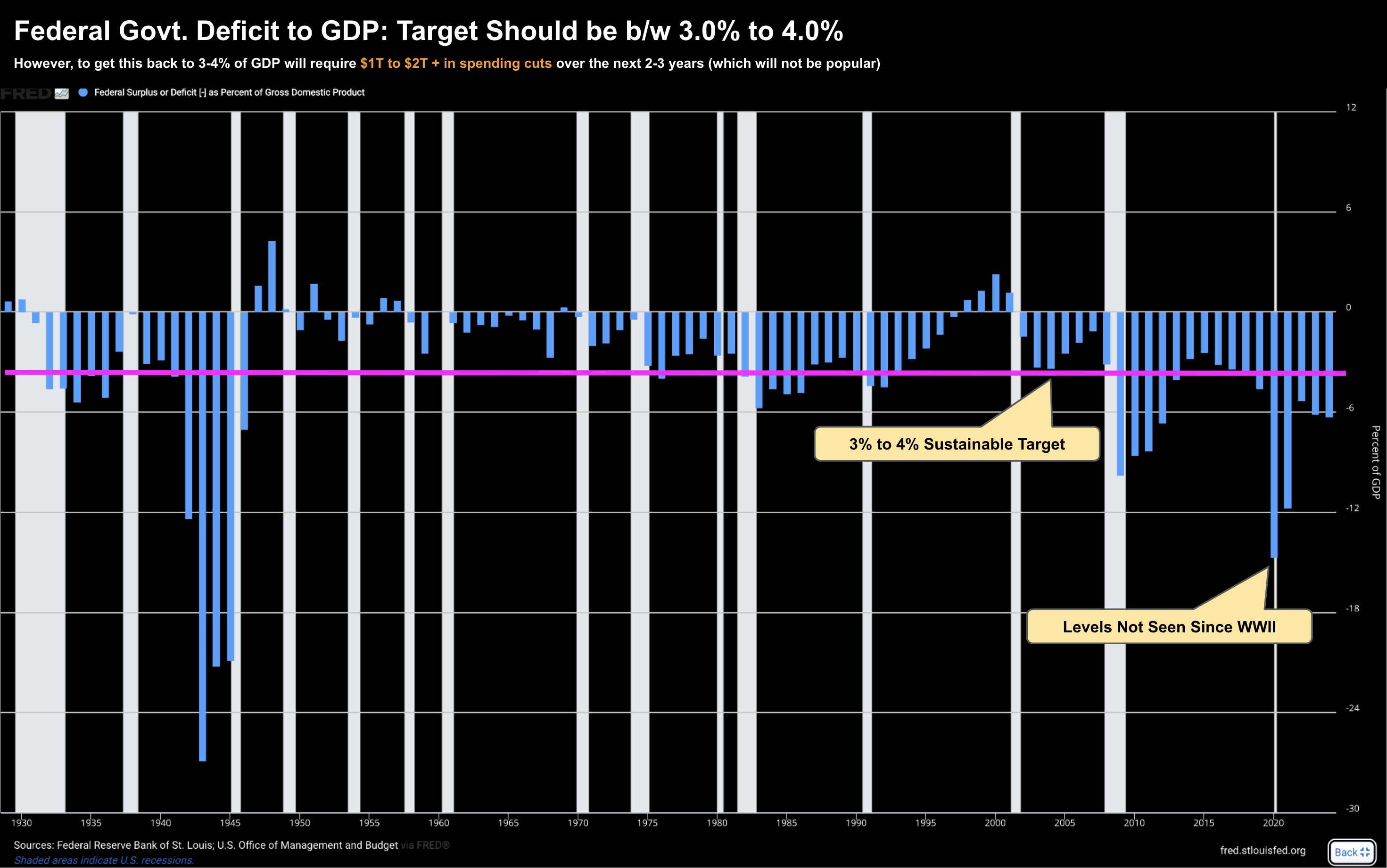

A major hurdle is the current deficit-to-GDP ratio, which sits near 7%. Historically, for a healthy economy with manageable interest rates, this ratio should ideally reside between 3.0% and 4.0%. Reducing this gap is the primary objective of the Department of Government Efficiency (DOGE).

Oil Prices and the Dollar: The Reserve Currency Factor

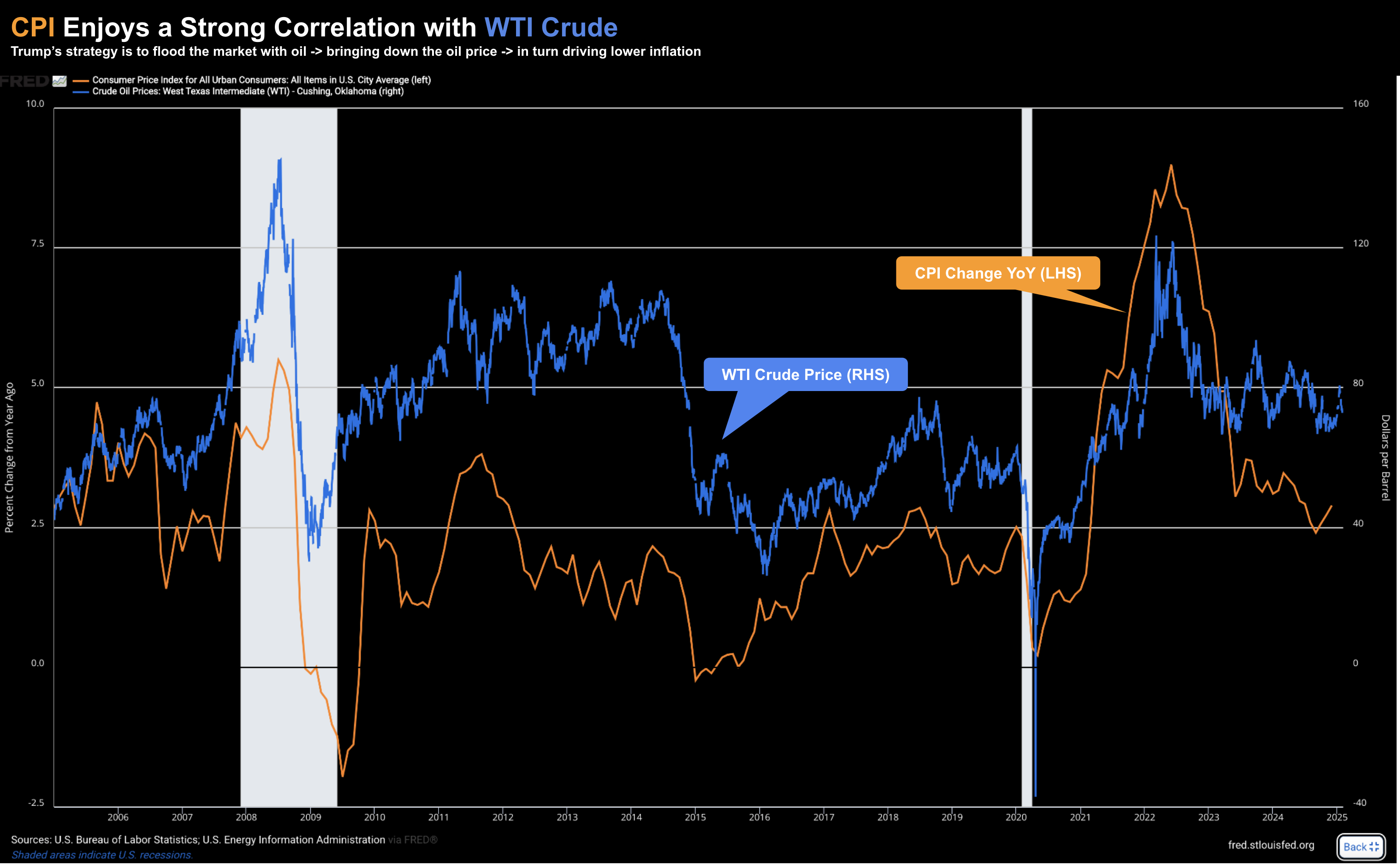

10-year yields are also heavily influenced by the energy complex and the value of the US dollar. Increasing domestic oil supply ("drill baby drill") can help lower inflation expectations, as seen in the historical correlation between CPI and WTI Crude.

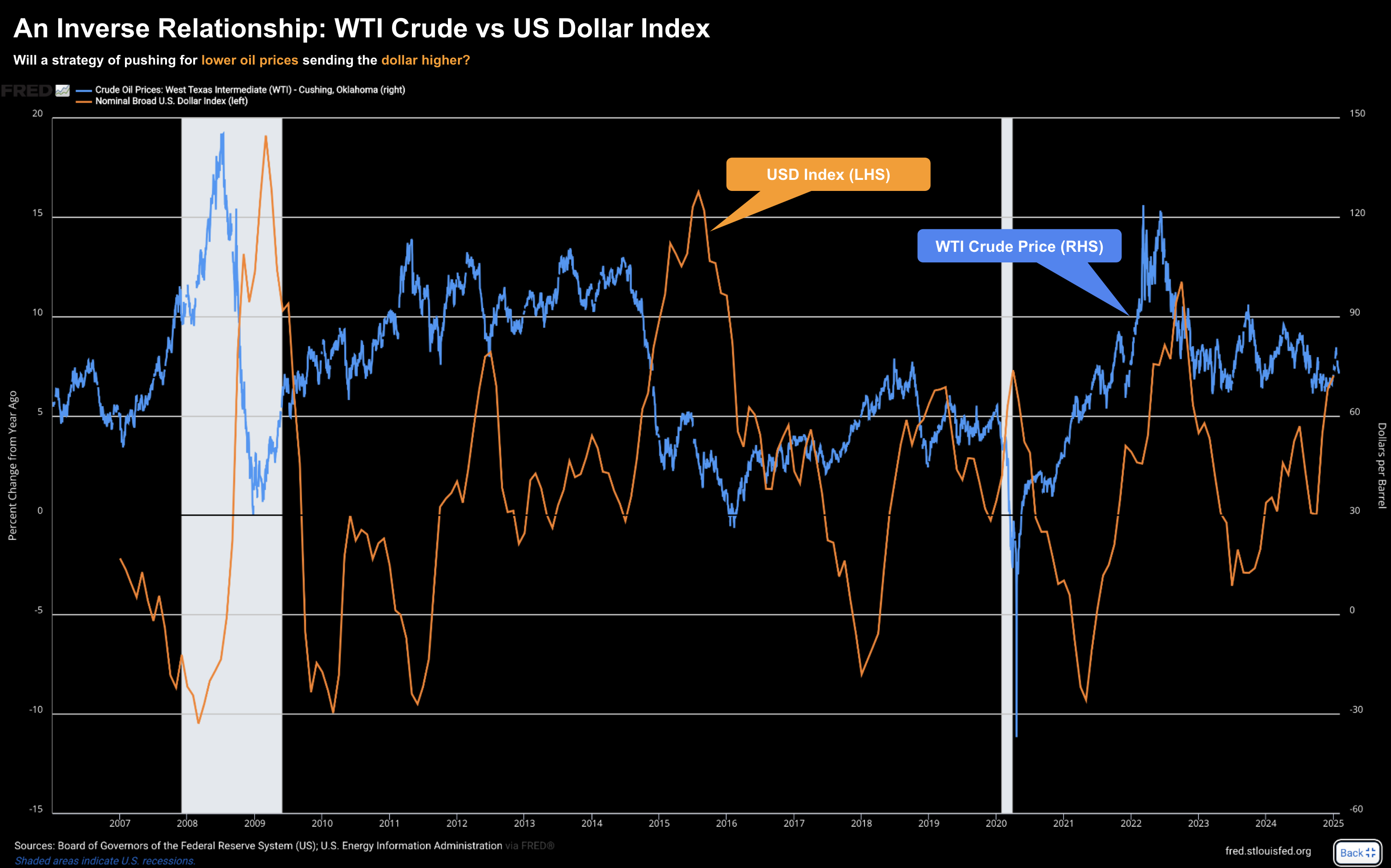

However, there is an inverse relationship between the dollar and oil prices. Because oil is traded globally in US dollars, a stronger dollar typically puts downward pressure on oil prices, making it more expensive for foreign buyers and reducing global demand. Maintaining a strong currency supports the US as a reserve currency, but it requires a delicate balance to ensure exports remain competitive.

Navigating "DOGE" and the Interest Expense Trap

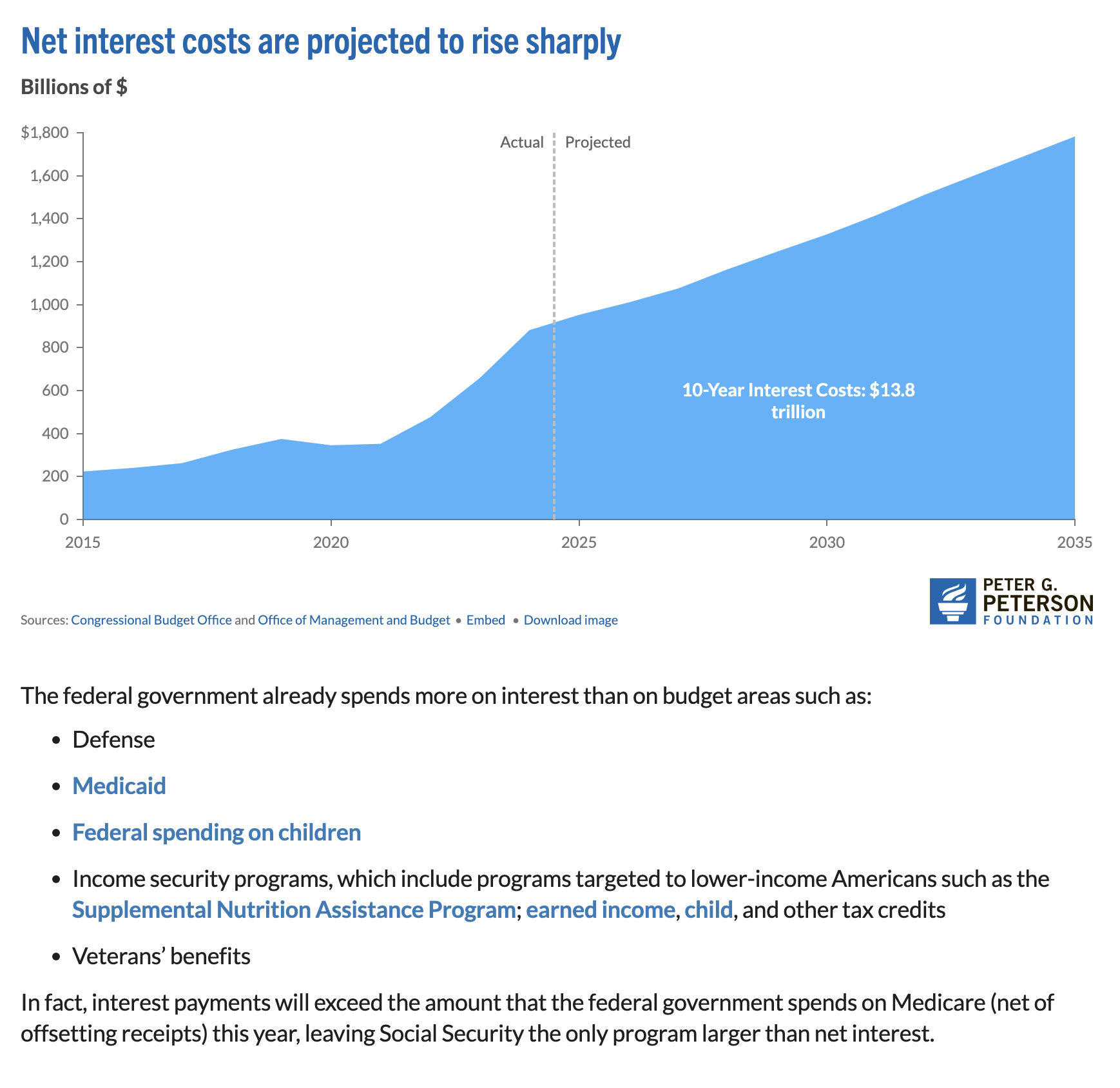

The Department of Government Efficiency (DOGE) is arguably the most critical component of this fiscal transition. Excessive government spending is a primary driver of inflation, and "bond vigilantes" are already pushing yields higher in response to fiscal recklessness. Currently, net interest costs on US debt now exceed spending on both defense and Medicaid.

To stabilize the economy, the administration must navigate a narrow channel between inflation and recession. If spending cuts are too small, the bond market may "riot," sending yields toward 6%. If cuts are too aggressive, they risk triggering a recession. Analysts estimate that federal spending needs to decrease by approximately 3.6% to stabilize the public debt-to-GDP ratio.

Putting it All Together

The Treasury"s path is fraught with political and economic resistance. Lowering the 10-year bond yield is essential for the financial well-being of households and the government alike, yet managing this transition without market distortion is a historic challenge. As yields march toward the 5.0% psychological level, equities will likely face continued pressure. Success will depend on whether DOGE can deliver enough austerity to satisfy the bond market without stalling the economic engine.