The Cost of Capital Reality Check: Why Rising Bond Yields Dictate the Next Market Cycle

Words: 974 Time: 4 Minutes

- The era of cheap debt is over: borrowers across the spectrum face structurally higher costs.

- A global sovereign debt glut is driving a historic "buyers strike" in bond markets.

- Why investors suffering from "Simple Pain-Avoiding Denial" shouldn"t count on the Fed for a bailout.

The defining question for this cycle:

How far can equity multiples expand when the fundamental cost of capital is broken?

That is the tension investors are currently trying to navigate.

As governments worldwide accelerate their already unsustainable borrowing and spending habits, bond yields are structurally forced higher.

The math is undeniable and reason-respecting: demand for debt is falling exactly as supply explodes.

At what point does the broader stock market finally acknowledge the math?

The Sovereign Debt Glut

The short version of this macro reality is simple: the transition back to historical norms is going to hurt.

That is what the bond market—the ultimate arbiter of economic truth—is signaling.

When you see the US 30-year yield hovering around 5.0% and the US 10-year trading near 4.50%, it confirms that governments are being forced to pay a severe premium for fiscal recklessness.

Institutional surveys consistently show that fears are rising among the "smart money."

Outright short positions across central banks, sovereign wealth funds, and real-money traders have frequently climbed to multi-year highs during these spikes.

Fueling this systemic doubt is the deterioration of US creditworthiness and spending bills that casually add $3 to $4 trillion to an eye-watering $37 trillion national debt—in an economy where output (GDP) is only $31 trillion.

This isn"t just a US phenomenon. We have seen massive selloffs in Japan"s long-term bonds, sending their yields to multi-year highs as the global contagion spreads.

Why the sharp, sudden repricing in global yields?

Using Japan as a case study, the 40-year "super-long" JGB yield spiked to a record 3.675% due to mounting anxieties over the sheer weight of the government"s debt load.

These super-long bonds lacked the support of traditional buyers. Life insurers and pension funds have actively scaled back purchases.

This highlights a structural problem:

Governments are relying on bond markets to soak up an unprecedented deluge of debt.

But the compensation (yield) investors receive is no longer sufficient to offset the inflation and default risks.

As long-term yields rise while central banks attempt to manage short-term rates, we witness a dramatic steeping of the yield curve.

Put simply: as buyer demand evaporates, supply continues to grow.

This dynamic puts immense upward pressure on the long end of the curve. And historically, that is a glaring red flag.

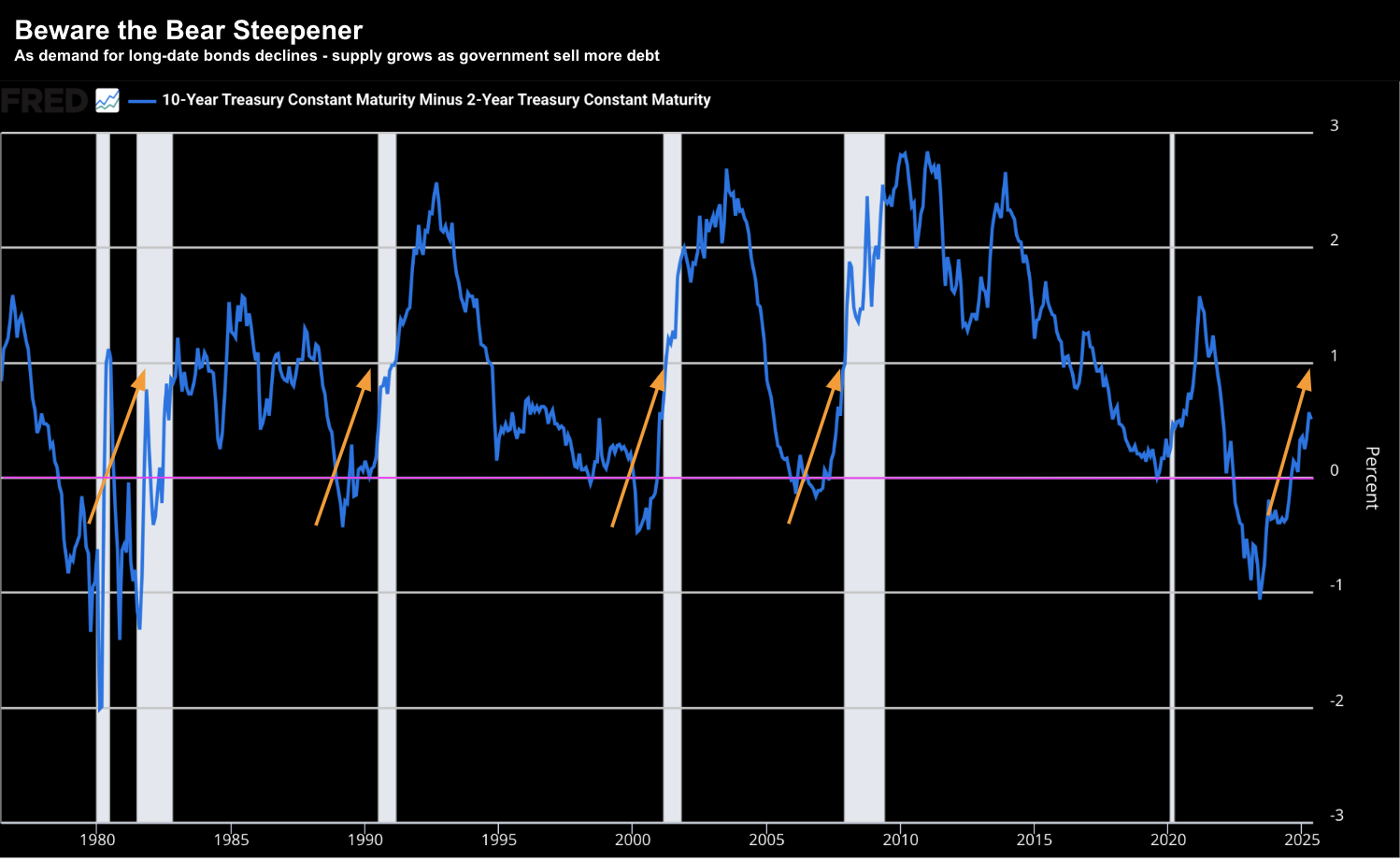

Below is the US 10-year yield minus the 2-year yield (a reliable proxy for the shape of the curve).

Notice the pattern: in almost every instance since 1980 where the 10-year less the 2-year re-steepened from a negative value (orange arrows), a recession followed within roughly 12 months.

Yet, equity markets often suffer from availability-misweighing, ignoring the bond market and rallying back toward all-time highs.

That complacency is a trap.

Structurally high (and rising) borrowing costs choke economic growth.

It acts as a hard limit on what governments can sustainably spend, and more importantly, it crushes the leverage capacity of the private sector (consumers and businesses).

From an investment lens, that is an unavoidable headwind.

The Death of the "Fed Put"

With borrowing costs suffocating growth, the natural question is: when does the Federal Reserve ride to the rescue?

The hard truth is that the "Fed Put" is largely disabled in an inflationary regime.

Protectionist policies, tariffs, and deglobalization have effectively removed the optionality central banks once enjoyed to quickly stimulate the economy.

As discussed in previous posts, central banks are now forced into a "wait and see" posture when inflation remains sticky.

Whenever inflation runs above target, policymakers cannot afford to be preemptive. As Powell himself has noted in the past:

"It"s not a situation where we can be preemptive, because we actually don"t know what the right responses to the data will be until we see more data."

The result is a structurally reactive Fed, rather than the proactive safety net investors grew accustomed to in the 2010s.

Without the persistent risk of inflation and supply chain tariffs, the Fed would have clear runway to cut rates based on three factors:

- Underlying economic growth is visibly slowing;

- The nominal Fed Funds rate remains elevated; and most critically,

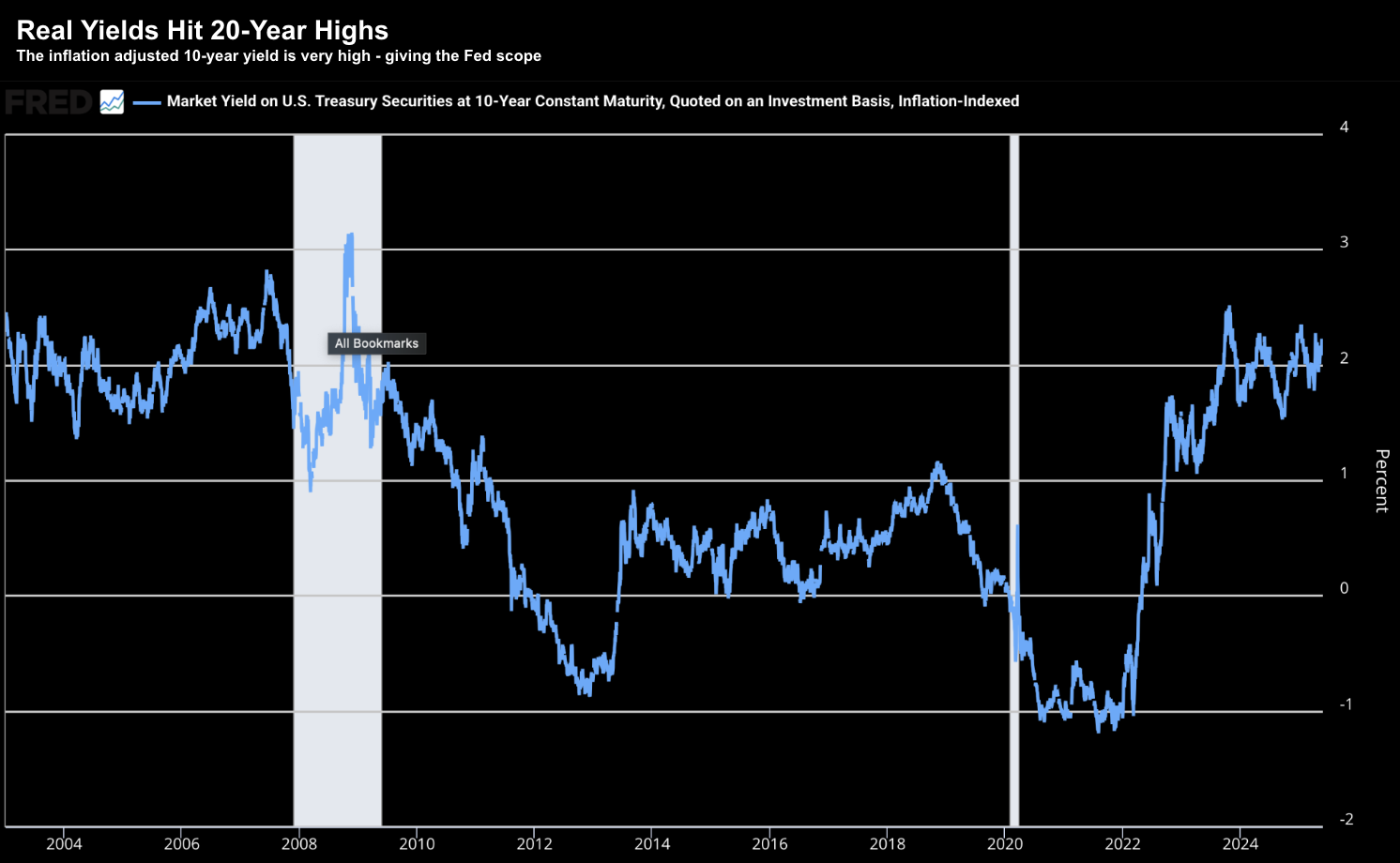

- Real yields remain very high (nominal rates minus inflation).

Only when geopolitical and protectionist shocks fully "pass through"—allowing inflation to completely normalize—can central banks confidently resume a sustained rate-cut cycle.

Until then, their hands are tied.

Putting It All Together

The convergence of widening deficits, ballooning debt, persistent fiscal stimulus, and sticky inflation creates a highly toxic environment for the bond market.

This Lollapalooza effect suggests that longer-term yields are engineered to remain at uncomfortable, elevated levels.

Unless we see a dramatic reversal in fiscal policy or a deep recession, the math simply doesn"t support a return to zero-interest-rate policy.

This has brutal implications not just for sovereign treasuries, but for Main Street consumers.

When sovereign yields rise, all borrowing costs rise.

This permanent repricing flows directly into mortgages, auto loans, credit cards, and small business financing.

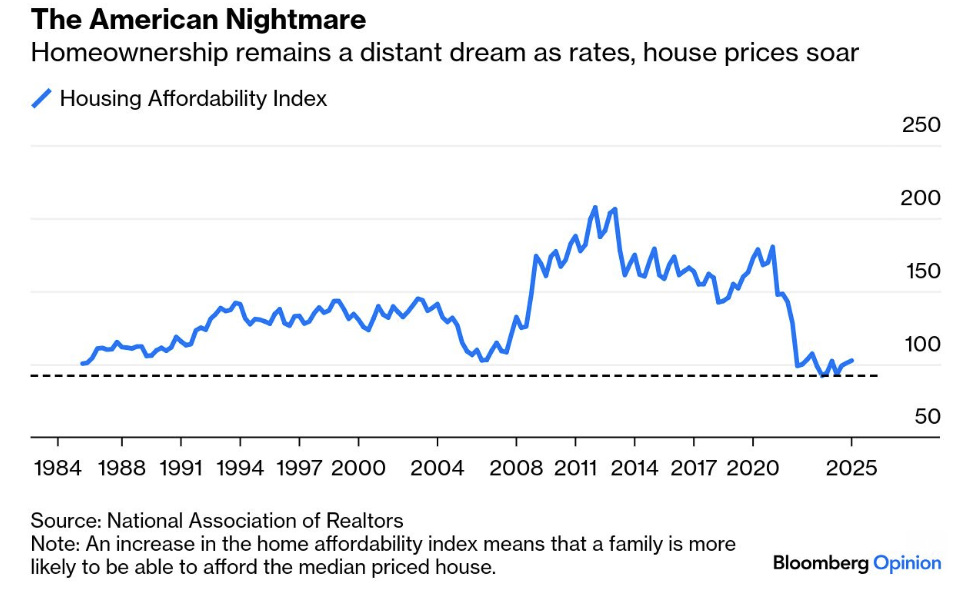

Look no further than the housing market:

Mortgage rates have proven incredibly sticky, severely limiting transaction volumes regardless of minor central bank adjustments.

Consequently, Housing Affordability Indices have repeatedly plunged to historic lows.

These indices measure whether a typical family earns enough to qualify for a mortgage on an average home at prevailing rates. The chart above illustrates the stark reality of what broken capital costs look like in practice.

Sadly, for an entire generation of aspiring homeowners, the math simply requires them to wait on the sidelines.

In closing, bond futures markets are exceptionally efficient at pricing in these structural realities long before the equity crowd catches on.

When traders drastically pare back the odds of rate cuts, they are signaling that the cost of capital will remain a heavy anchor on the broader economy.

Cuts at the short-end of the curve can only provide temporary relief. The structural damage inflicted by the long-end of the curve takes years to absorb.

For now, equities might be ignoring the bond market. But historically, the bond market always has the final word.