The Math of Moats: Why ROIC and Free Cash Flow Trump Revenue Growth

Words: 1,405 Time: 7 Minutes

- The "Buffett Baseline": Understanding the $330+ Billion cash pile.

- Productive Capital: Why government GDP and business ROIC are not the same.

- The Quality Audit: How to benchmark your portfolio against the 15/15 Rule.

Markets are perpetually worried. Whether the headline is inflation, geopolitical tension, or shifting tariffs, the noise is constant. However, for the disciplined investor, the macro-environment is secondary to a single, fundamental question: Is the capital being deployed productively?

Productive vs. Unproductive Spend

There is a fundamental flaw in how we measure economic "growth" via GDP. In the national accounts, every dollar spent by a government is treated as a positive contribution. It doesn"t matter if that dollar goes toward fixing a vital trade artery or a study on rare fish in a distant land—it is all "growth."

A real business does not have this luxury. If a company allocates capital unproductively, it doesn"t just "slow down"—it eventually goes broke. It cannot simply ask taxpayers for more. As fiscal deficits rise, the burden of growth eventually shifts back to private business investment. This is where we find our opportunity.

The Buffett Cash Machine: A Study in Quality

While the broader market frets over "growth scares," Berkshire Hathaway continues to hit record highs. The secret to this "cash machine" isn"t chasing the next hot trend. It is a relentless focus on three evergreen pillars:

- High ROIC: Companies that produce superior returns on the capital they"ve already invested.

- Strong Free Cash Flow: Businesses that generate "owner earnings" without requiring massive debt or constant re-investment just to stay in place.

- Rational Valuation: Only entering these positions when the price offers a "margin of safety"—typically measured on a P/FCF or EV/EBIT basis.

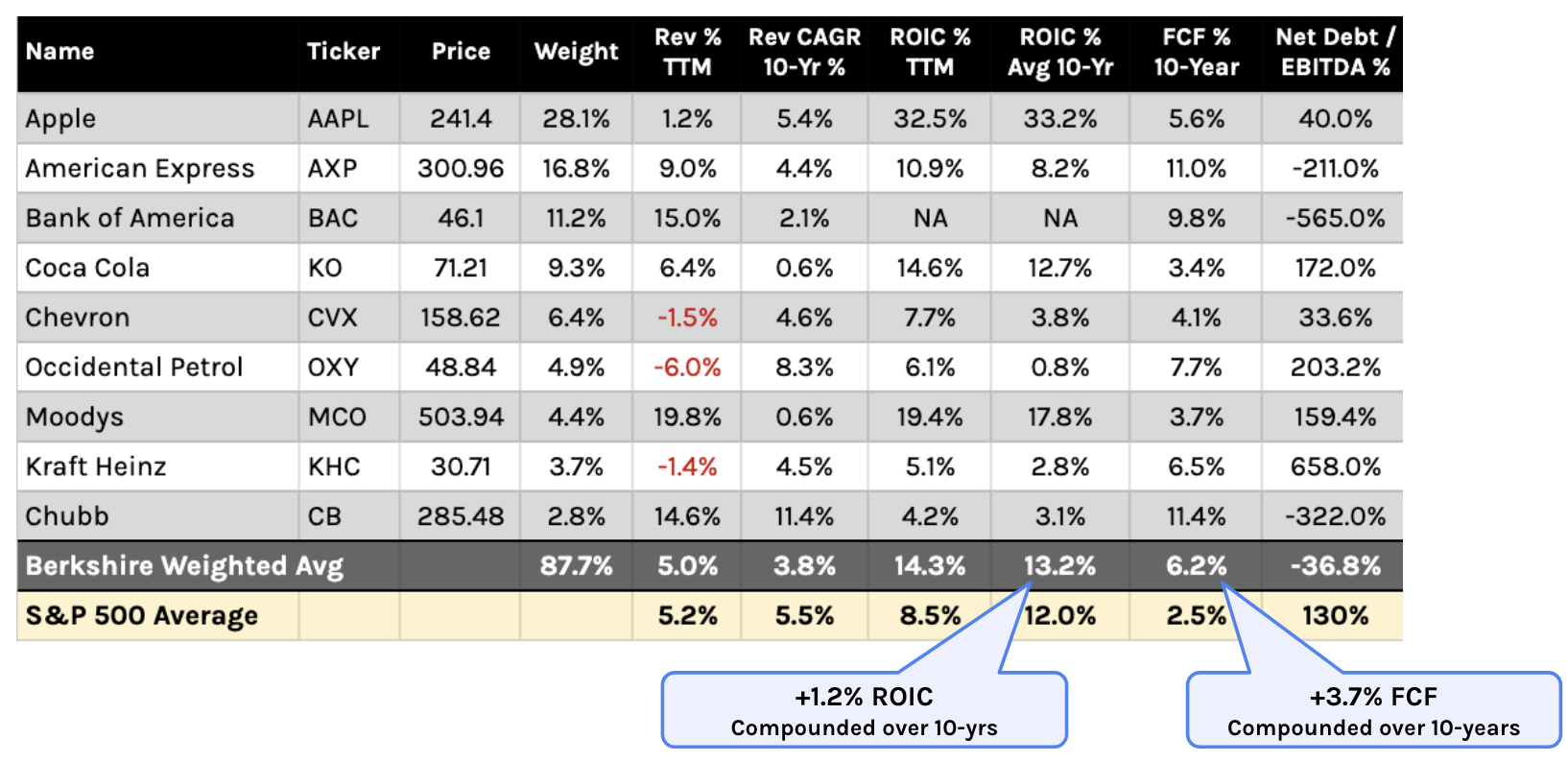

Surprisingly, Buffett"s top holdings—accounting for nearly 90% of his portfolio—rarely boast "explosive" revenue growth. In fact, many have a 10-year revenue CAGR of less than 4%, well below the S&P 500 average. This reveals a profound lesson: Efficiency trumps expansion.

The 15/15 Audit: Benchmarking Your Portfolio

To invest like a professional, you must look past the "narrative" of revenue growth and focus on the incremental return on capital. If a company is growing revenue at 30% but its ROIC is falling, it is destroying value, not creating it.

I use a specific "15/15" framework to filter for quality. If you want to audit your own holdings, build a table that measures the following:

- The 15/15 Rule: Does the company maintain a Return on Equity (ROE) and Return on Invested Capital (ROIC) of at least 15%?

- The 55/30/25 Model: Does the business boast a ~55% Gross Margin, ~30% SG&A, and ~25% EBITDA margin? This identifies a durable moat.

- Free Cash Flow Yield: Is the FCF 10-year average significantly higher than the Index average (typically ~2.5%)?

- Net Debt / EBITDA: Is the company relying on leverage to "manufacture" growth, or is it self-funding?

Consider Buffett"s recent addition of Sirius XM. It wasn"t a play on stellar growth—revenue was flat. It was a play on High ROIC and strong FCF at a deep discount (roughly 7.9x FCF). At that price, you don"t need growth to win; you just need the business to keep doing what it"s doing.

Inversion: How to Build a Failing Portfolio

To find the path to success, we must first define the path to failure. If you want to ensure your portfolio underperforms over the next 10 years, do the following:

- Chase "Hot" Revenue: Buy companies growing at 50% YoY regardless of their margins or cash burn.

- Ignore the Balance Sheet: Invest in high-debt companies that require low interest rates to survive.

- Pay Any Price: Assume that "quality" justifies a 50x multiple, ignoring the mathematical reality of a "perfect storm" when multiples eventually contract.

- Succumb to Recency Bias: Assume that because the market hasn"t had a "buyable dip" in months, it never will again.

Putting it All Together

Buffett famously noted that you don"t need a high intellect to be a great investor—you just need the discipline to stay within your Circle of Competence and the emotional fortitude to avoid self-defeating behaviors.

The math isn"t difficult; it"s the sitting and waiting that is hard. While headlines scream about "dips," a look at the weekly chart shows we are barely off all-time highs. A truly compelling value zone (like the 5200 level representing 19x earnings) requires patience.

Successful investing is built on a "cash flow machine." Focus on the quality metrics that matter, refuse to overpay, and let the compounding do the heavy lifting. If you are ready to dig deeper into these filters, start with my guide on Simplifying Quality and Value.