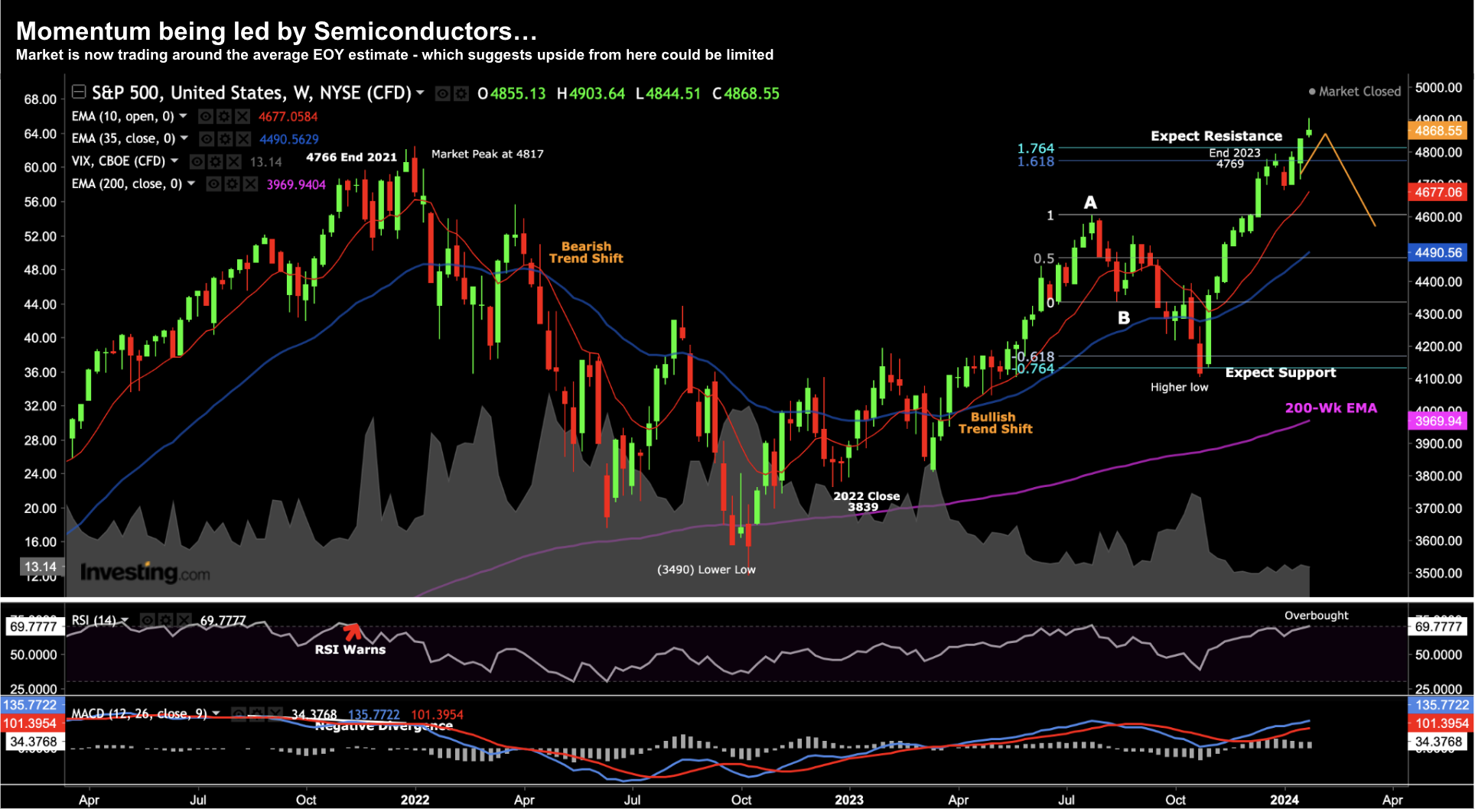

Smart Money Sells Big Tech… Invests in NKE & SBUX

Smart Money Sells Big Tech… Invests in NKE & SBUX

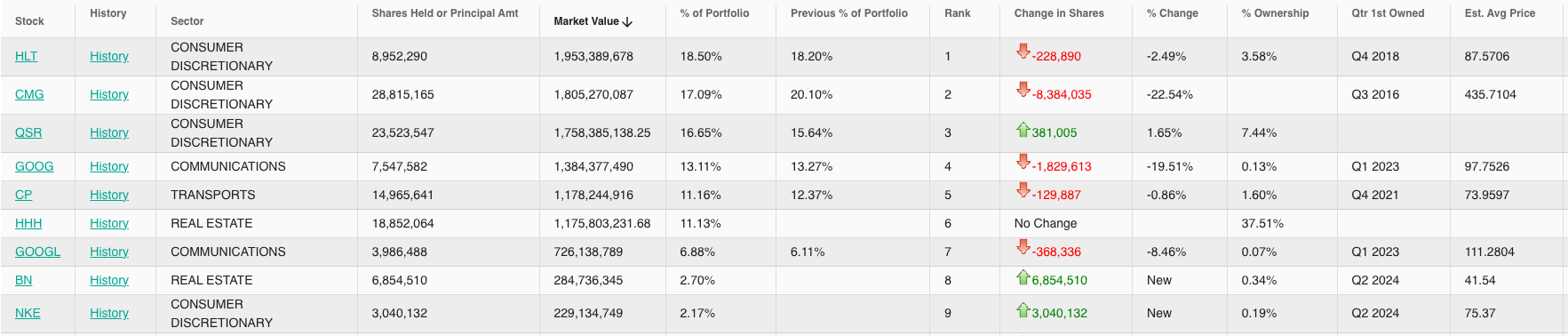

Something I do four times a year is pore through something known as "13Fs". A 13F is a quarterly report that institutional investment managers with over $100 million in assets must file with the US Securities and Exchange Commission. And whilst these filings are submitted around 45 days after the quarter ends (e.g. August 15 deadline for June 30 quarter end) - they offer us insight into how the "smart money" is thinking about certain assets. Some names I follow include (not limited to) Warren Buffett, Bill Ackman, David Tepper, Howard Marks, Stan Druckenmiller and Seth Klarman. Now there was a consistent trend during Q2 - where large cap tech exposure was being reduced.