Powell’s Itchy Trigger Finger

Powell’s Itchy Trigger Finger

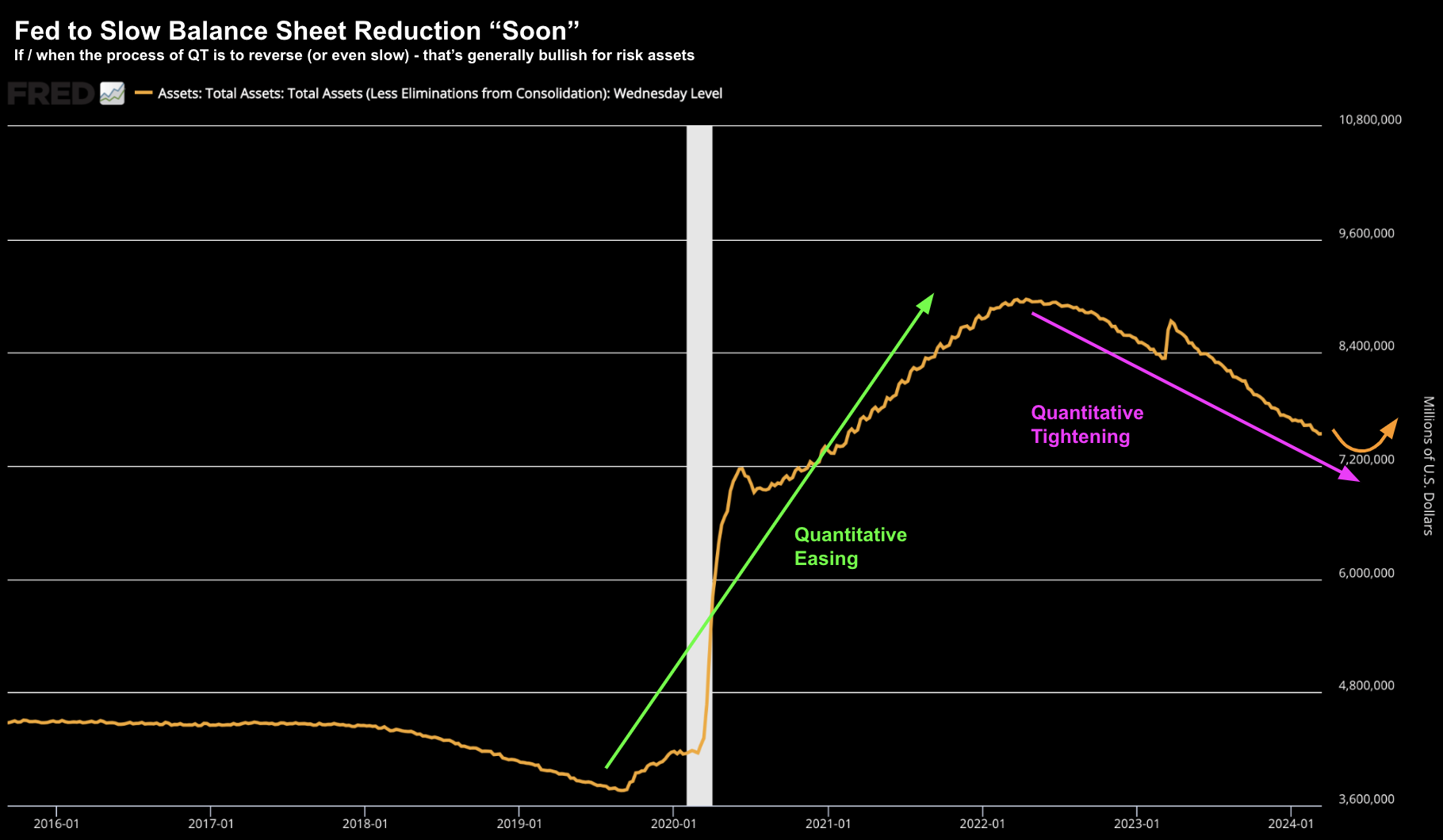

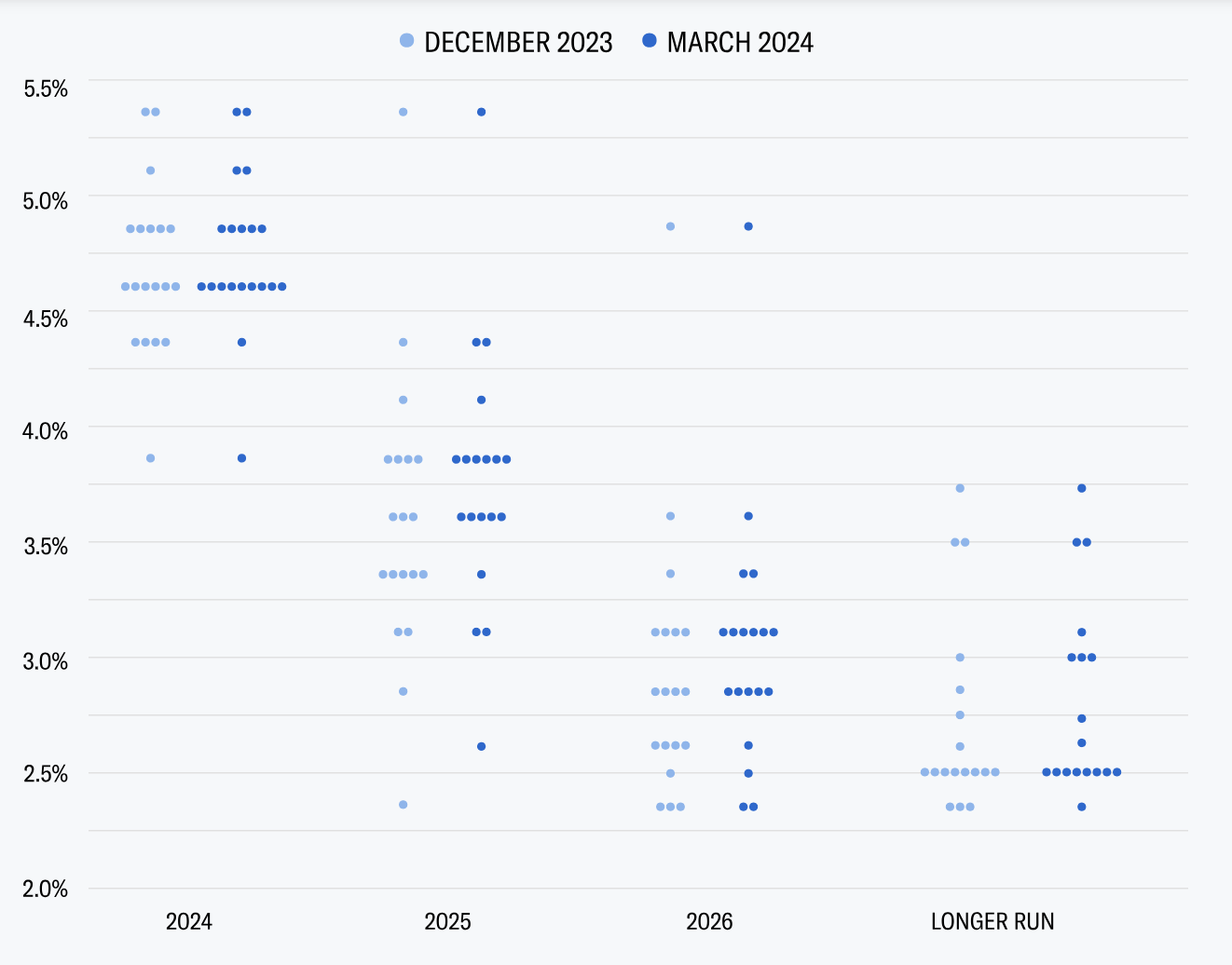

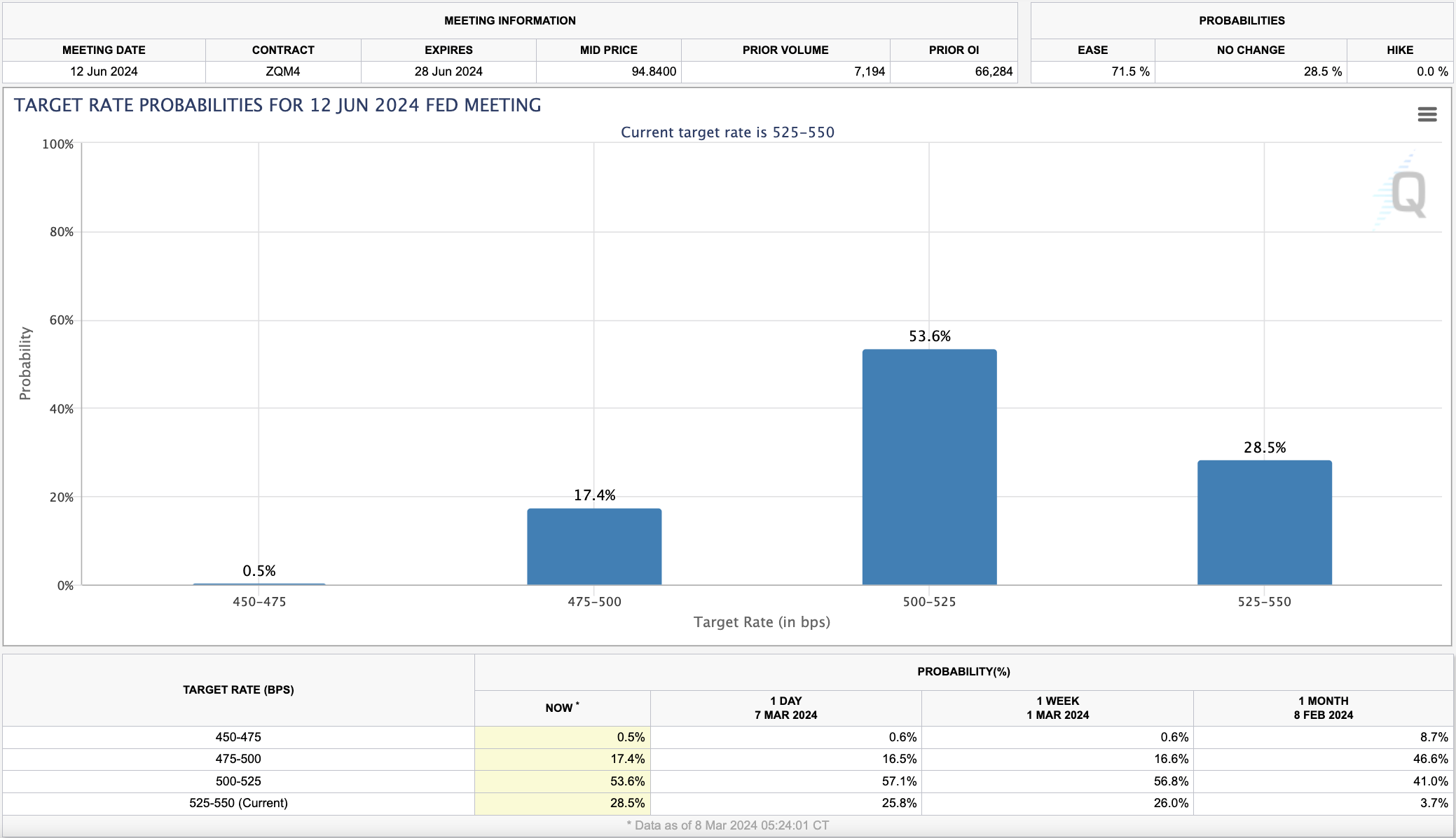

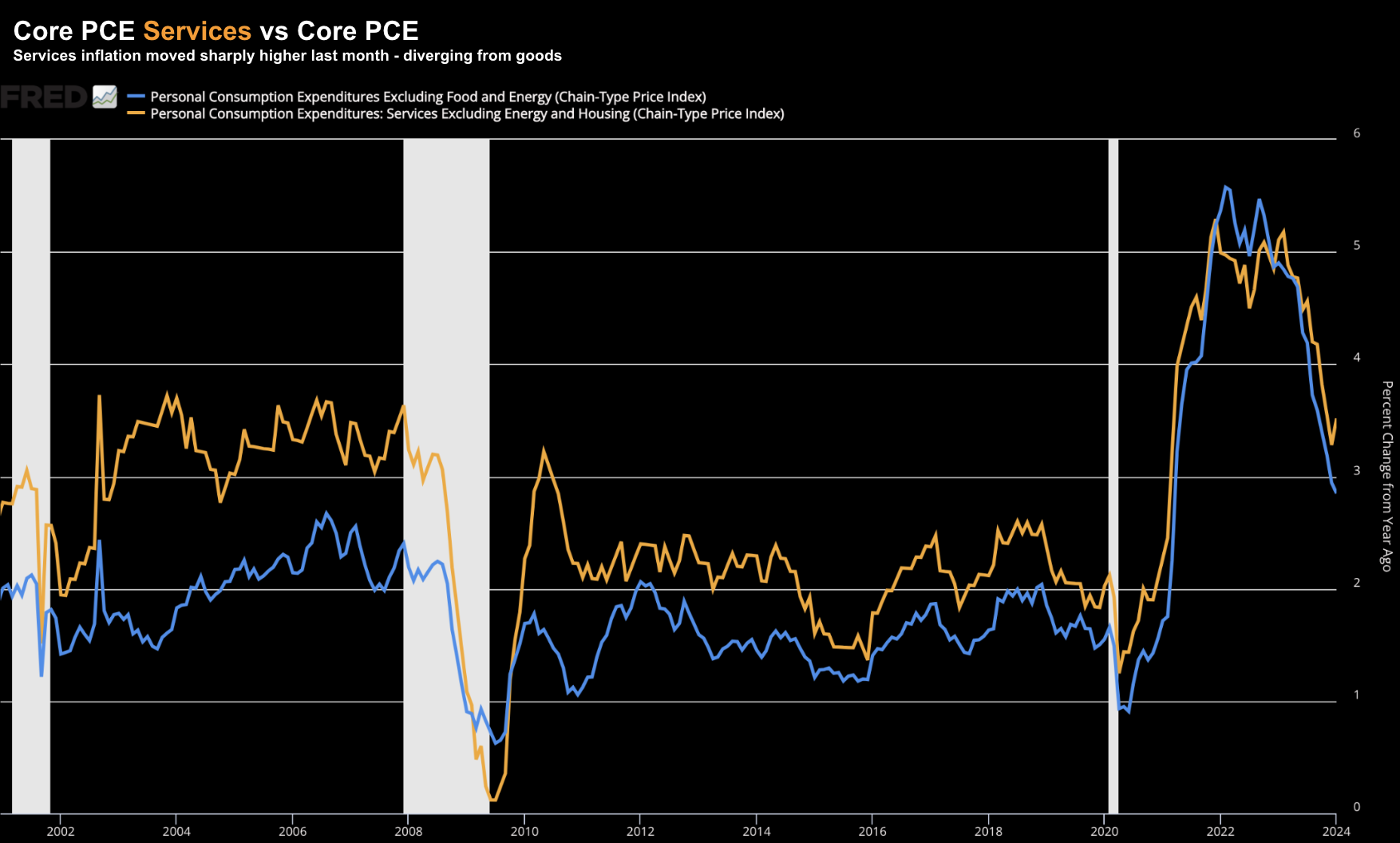

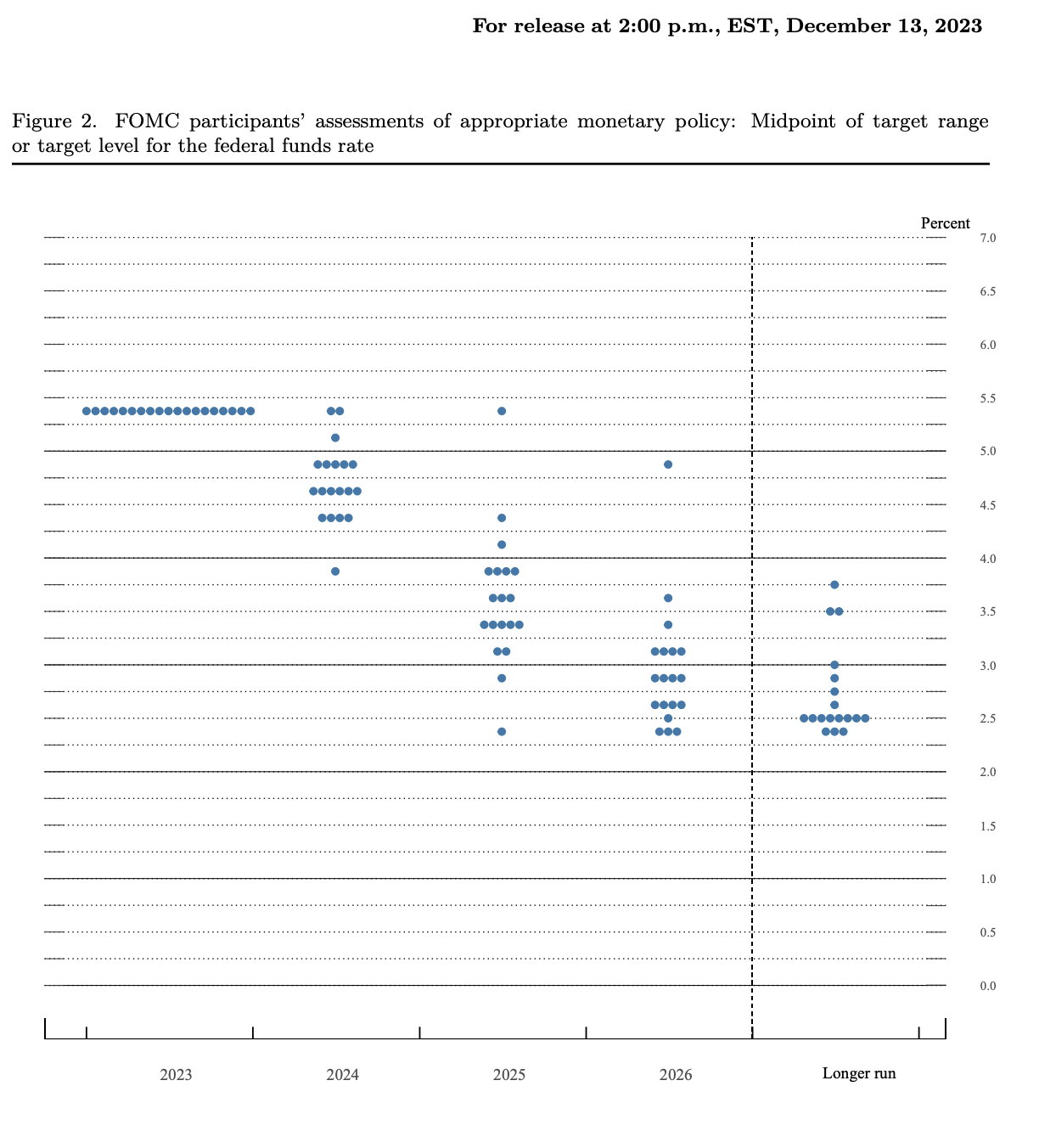

Why does Powell think the Fed needs to cut rates? For me it's curious. Itchy (trigger) finger maybe? What's he so worried about? I was surprised by his (continued) dovish rhetoric and contradiction(s) last meeting. For example, on the one hand, growth is accelerating, inflation is falling and we have a strong labor market. Great! But we still need to cut rates and taper QT (soon!). I must be missing something - it's hard to understand why the Fed is so keen to pull the trigger... what do they see we don't?