Expensive and Risky

Expensive and Risky

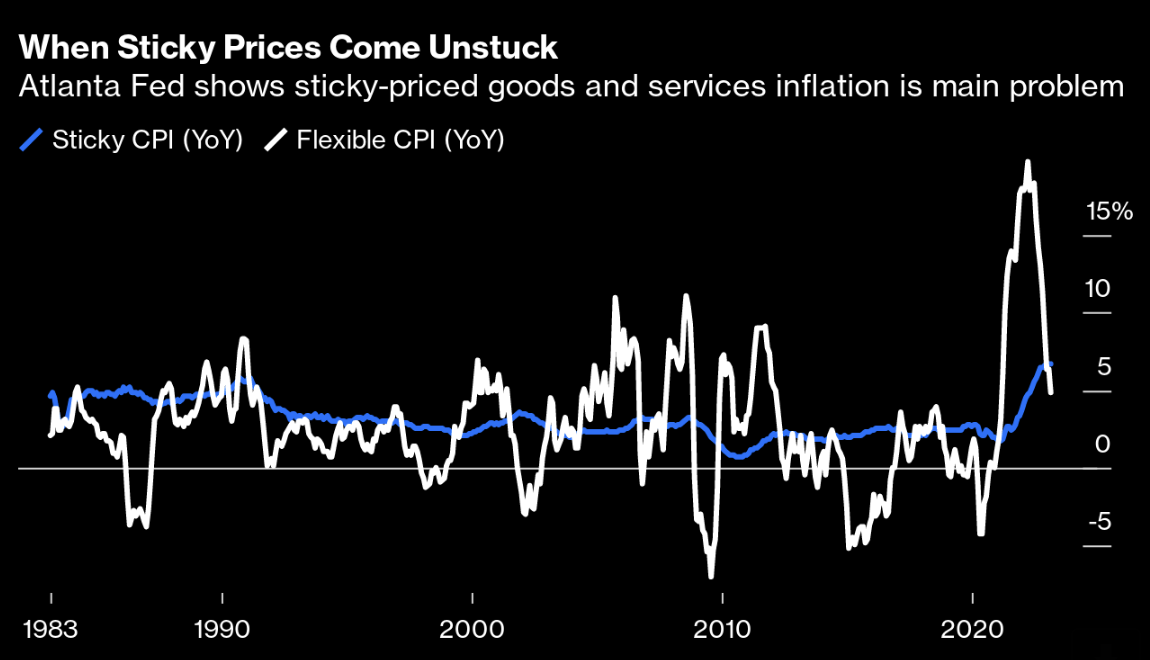

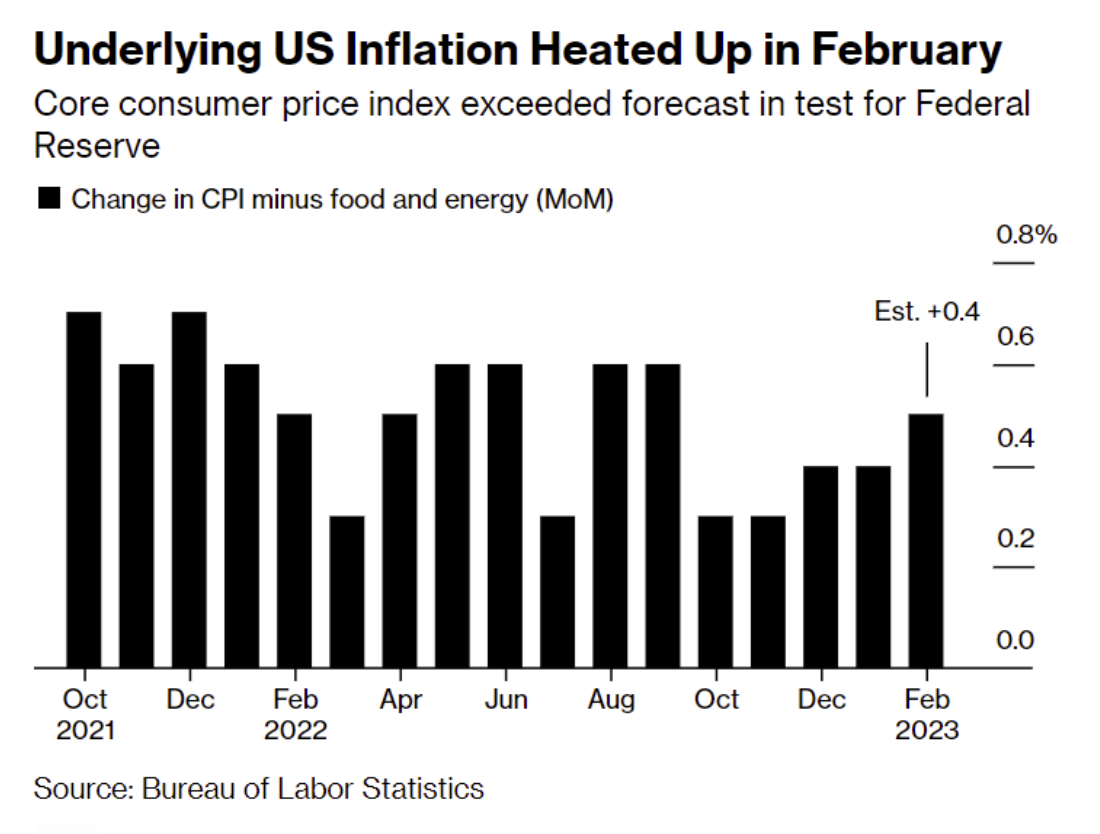

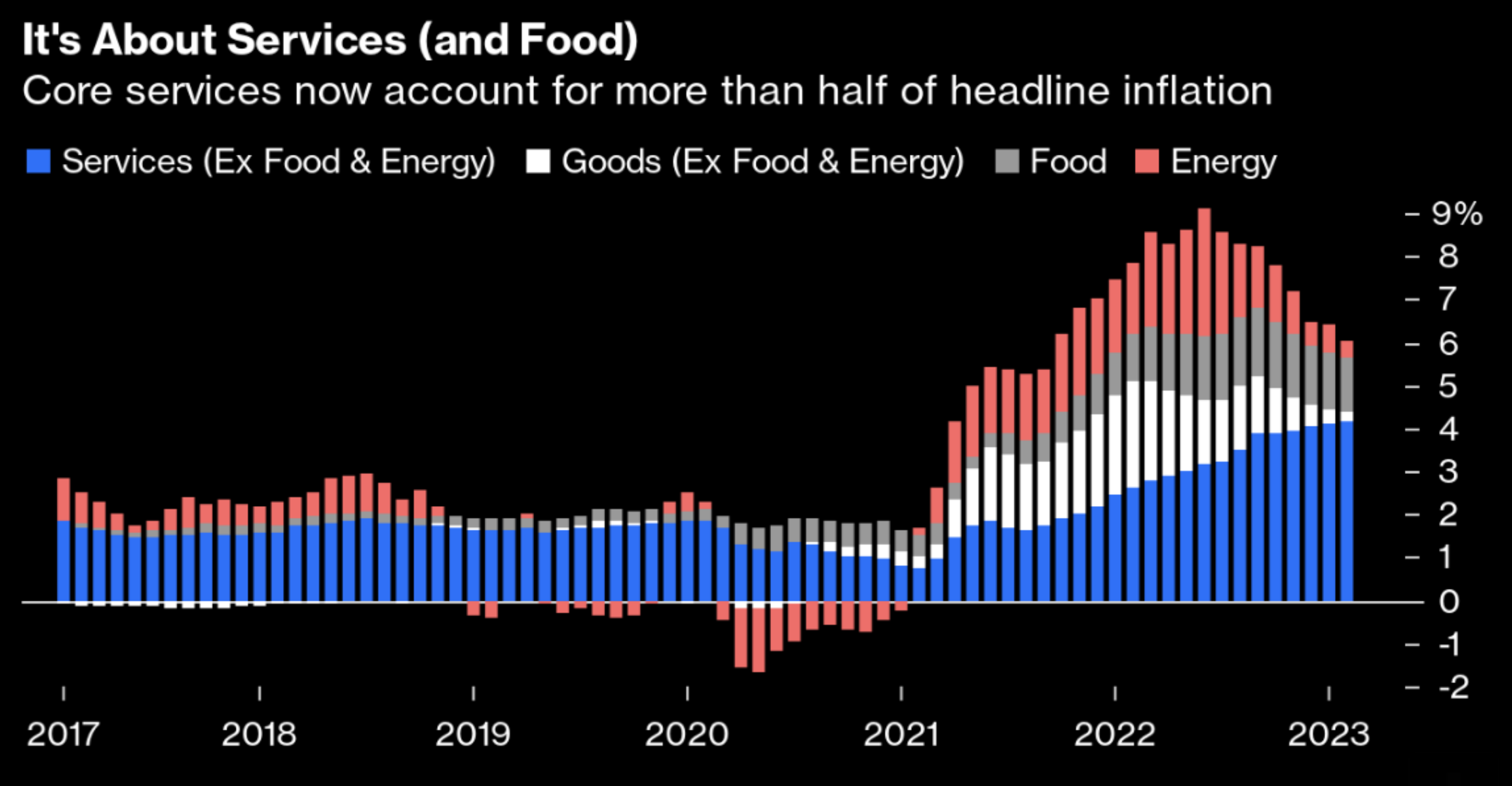

Stan Druckenmiller - one of the greatest investors of all time - is issuing a stark warning. Tread carefully. He echoes much of my sentiment of the past few months; i.e. not only do I think the market is fully valued at 19x forward earnings -- it represents meaningful downside risk. What concerns me most is what the market assumes will happen over the next ~6-9 months. E.g., at the time of writing, it sees rates being slashed three times this year. Is that realistic with Core CPI YoY is still traveling around 5.5%? It also sees earnings growth. Will that happen opposite a recession? It's a long list of assumptions...