The Math of Moats: Why ROIC and Free Cash Flow Trump Revenue Growth

The Math of Moats: Why ROIC and Free Cash Flow Trump Revenue Growth

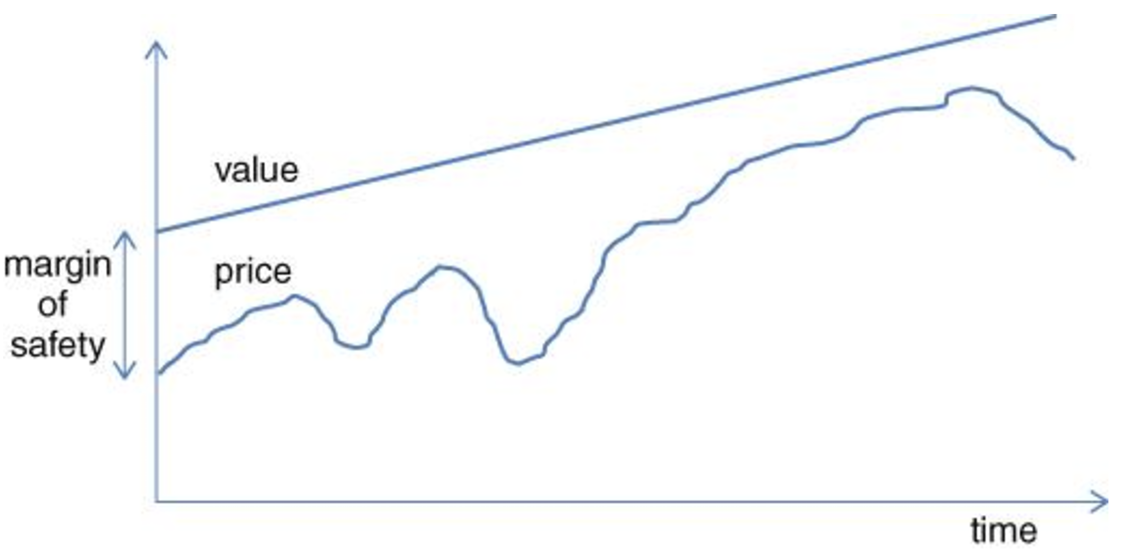

Whilst market's fret about slowing growth ("Ready for a Growth Scare?") - Warren Buffett sits back with a smile. His company - Berkshire Hathaway - rallied to fresh record high this week after the company reported a record high quarterly profit. Its market value is now over $1.1 Trillion. So how did Buffett build this incredible cash machine? I'll outline three (basic) reasons... all of which you can emulate.