Real Retail Sales Continue to Warn

Real Retail Sales Continue to Warn

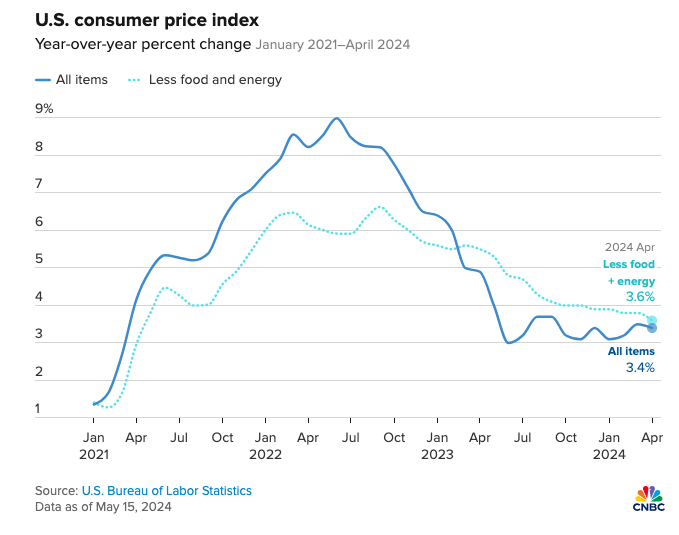

When I caught the headline "retail sales hold up in June - better than expected" - I was curious to read the detail. Yes, it's true that nominal sales were flat MoM. But that's not what it states. They don't mention "nominal". As analysts and investors - nominal values are of very little use. What helps us more when forecasting trends (and assessing risks) is real sales. Real retail sales are those adjusted for inflation. And with inflation stubbornly high ~3.0% year-over-year (approximately) - that makes a big difference. When viewed through this prism - real retail sales have been declining for months.