Math Trap: Why S&P 500 Valuations Lack a Critical Margin of Safety

Words: 893 Time: 4 Minutes

- The fundamental math of risk-and-reward: Why current valuations demand extreme caution.

- Equity Risk Premiums have collapsed to historic lows, removing the incentive to own stocks over bonds.

- The "Bond Vigilantes" are back: How fiscal deficits are dictating the ceiling for equity prices.

The S&P 500 has continued an aggressive rally, climbing over 22% from its recent lows.

At current levels, the market is trading at a forward price-to-earnings (P/E) ratio of ~22x, based on expected earnings per share (EPS) of ~$270 for the year.

To understand the true value of this market, we must look at the earnings yield (the inverse of the P/E ratio). At 22x, the market is offering an earnings yield of just 4.56%.

This figure represents the underlying "interest rate" the stock market pays you for every dollar invested. The question every disciplined investor must ask is: does 4.56% represent an attractive risk-adjusted return?

One of the most reliable ways to answer this is by comparing that 4.56% yield to the "risk-free" return of a government bond, such as the US 10-year Treasury note.

Today, that risk-free return is 4.43%.

Analysis as of May 2025

The math is stark: stocks are only offering an incremental 0.13% yield over "guaranteed" government bonds, despite carrying significantly higher volatility and capital risk.

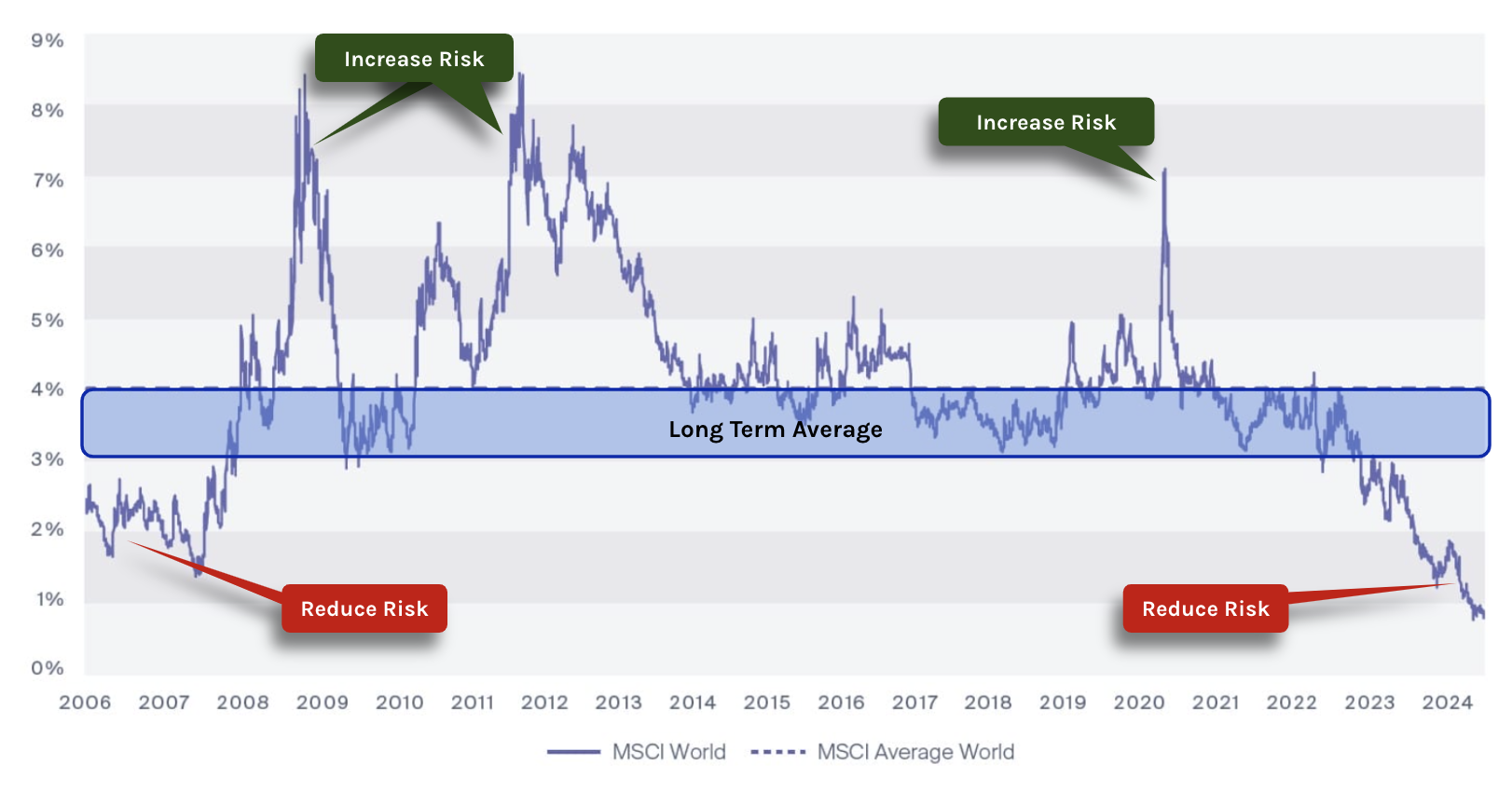

Historically, the Equity Risk Premium (ERP)—the extra return investors demand for choosing stocks over "safe" bonds—usually sits between 3% and 4%.

As this 20-year chart illustrates, when investors add equity exposure during periods of low (or negative) risk premiums, subsequent long-term returns are typically poor.

Conversely, the most successful long-term investors allocate capital when the ERP is high. For instance:

- Adding risk in 2006 and 2007 (when the premium was low) resulted in severe losses.

- Allocating capital in 2009 (when the premium spiked) generated massive compounding returns.

- Buying during the 2020 COVID crisis—when the ERP climbed to 7%—represented an exceptional generational opportunity.

This model forces us to confront several critical questions:

- Is the $270 EPS target too optimistic? If earnings fall short, the P/E ratio effectively rises, making the earnings yield even less attractive.

- What happens if bond prices continue to fall due to fiscal instability? Rising yields will compress equity valuations even further.

- If we see the "double downside" of disappointing earnings and bond yields moving toward 5.0%, where is the floor for the market?

These are the questions investors must weigh before adding meaningful exposure at current prices. The higher the 10-year yield climbs, the harder it becomes to justify aggressive equity valuations.

The Battle for Capital: Stocks vs. 4.50% Yields

It is difficult to build a compelling investment case for stocks when the risk premium is well below 1%. While this is not a precise "market timing" tool, it is a highly accurate directional compass.

With the US 10-year yield trading around 4.50%, "safe" income is beginning to pull capital away from the riskier equity market. However, there is a structural tension at play.

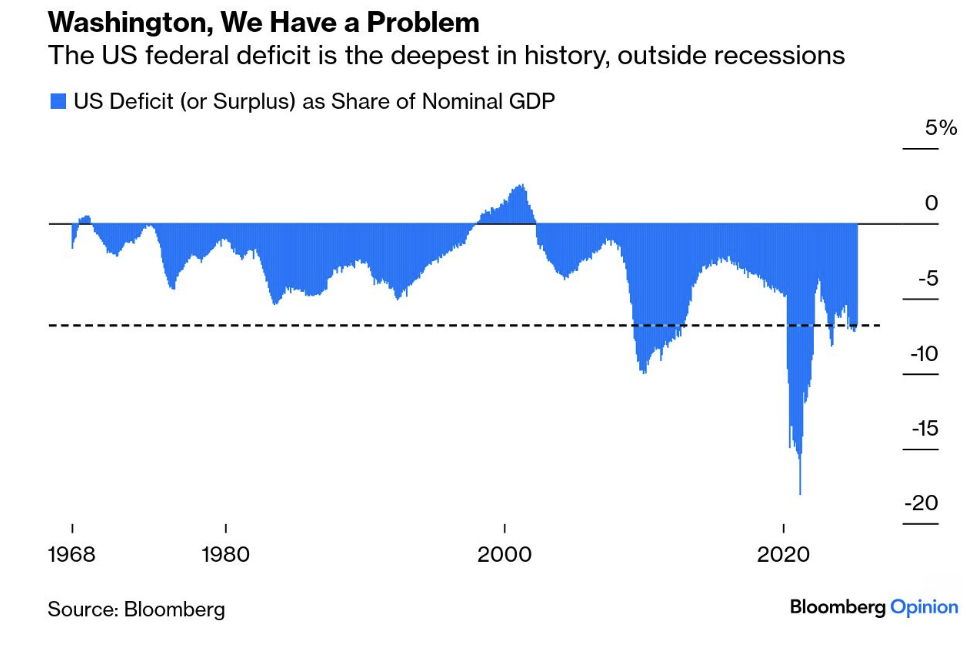

If the government fails to rein in deficits and debt, we should expect "bond vigilantes"—institutional investors who sell bonds to protest inflationary fiscal policy—to keep yields high.

When the national deficit sits at 7% of GDP—a level usually reserved for wartime or economic emergencies—the bond market begins to demand a much higher "inflation protection" premium.

The bond market is currently being driven by two powerful forces:

- Skepticism regarding the government"s ability to address its exploding debt load; and

- Recalibrated expectations for the Federal Reserve"s ability to cut interest rates.

As discussed in recent updates, protectionist trade policies and tariffs represent a significant secondary risk to both inflation and economic growth.

Earlier in the year, the market was pricing in a steady series of rate cuts. That narrative has shifted. The likelihood of an immediate cut has diminished as the market realizes that higher inflation means "higher for longer" interest rates.

The ultimate ceiling?

Longer-term yields are a function of supply and demand. Currently, the demand for US debt is struggling to keep pace with the massive supply being issued. This imbalance is driving yields higher.

If the 10-year yield presses toward the 5.0% mark, the pressure on equity valuations will likely become unsustainable.

Strategic Outlook

The Federal Reserve is currently in no hurry to lower rates. Geopolitical tensions and trade barriers have effectively tied the hands of policymakers.

Without a cooling of inflationary pressures, the Fed cannot provide the proactive support that equity investors are currently pricing in. But the real story isn"t the Fed—it"s the bond market.

If fiscal policy remains on its current trajectory of reckless borrowing and spending, the bond market will dictate the terms of the next cycle. Neither central bankers nor politicians can override the fundamental laws of supply and demand in the debt markets.

In conclusion, keep a close watch on the US 10-year yield. If yields test or exceed 5.0%, the "math" for a 22x P/E ratio on the S&P 500 simply ceases to exist.