The Rules of Engagement: Navigating Market Uncertainty and the Tariff Tug-of-War

Words: 725; Time: 4 Minutes

- Uncertainty is the byproduct of shifting economic rules.

- Strategic Tit-for-Tat: Decoding the symbolic nature of trade barriers.

- Three signals that suggest professional investors are hedging their bets.

For any disciplined investor, success is largely predicated on knowing the "rules of the game." When those rules—the frameworks for trade, taxes, and interest rates—are in constant flux, the natural result is heightened uncertainty. History shows us that when visibility drops, conviction wavers, and capital begins to pull back from the frontier.

Today, investors are grappling with a trifecta of structural shifts:

- A pivot in monetary policy as inflation remains stickier than forecasted;

- A rapid-fire series of policy shifts regarding global trade and domestic spending; and

- A "show me the money" moment for Artificial Intelligence, where the market is now scrutinizing the Return on Invested Capital (ROIC) for massive infrastructure spends.

This environment makes it increasingly difficult to commit to equities with high conviction, and we are seeing this fatigue reflected in the price action.

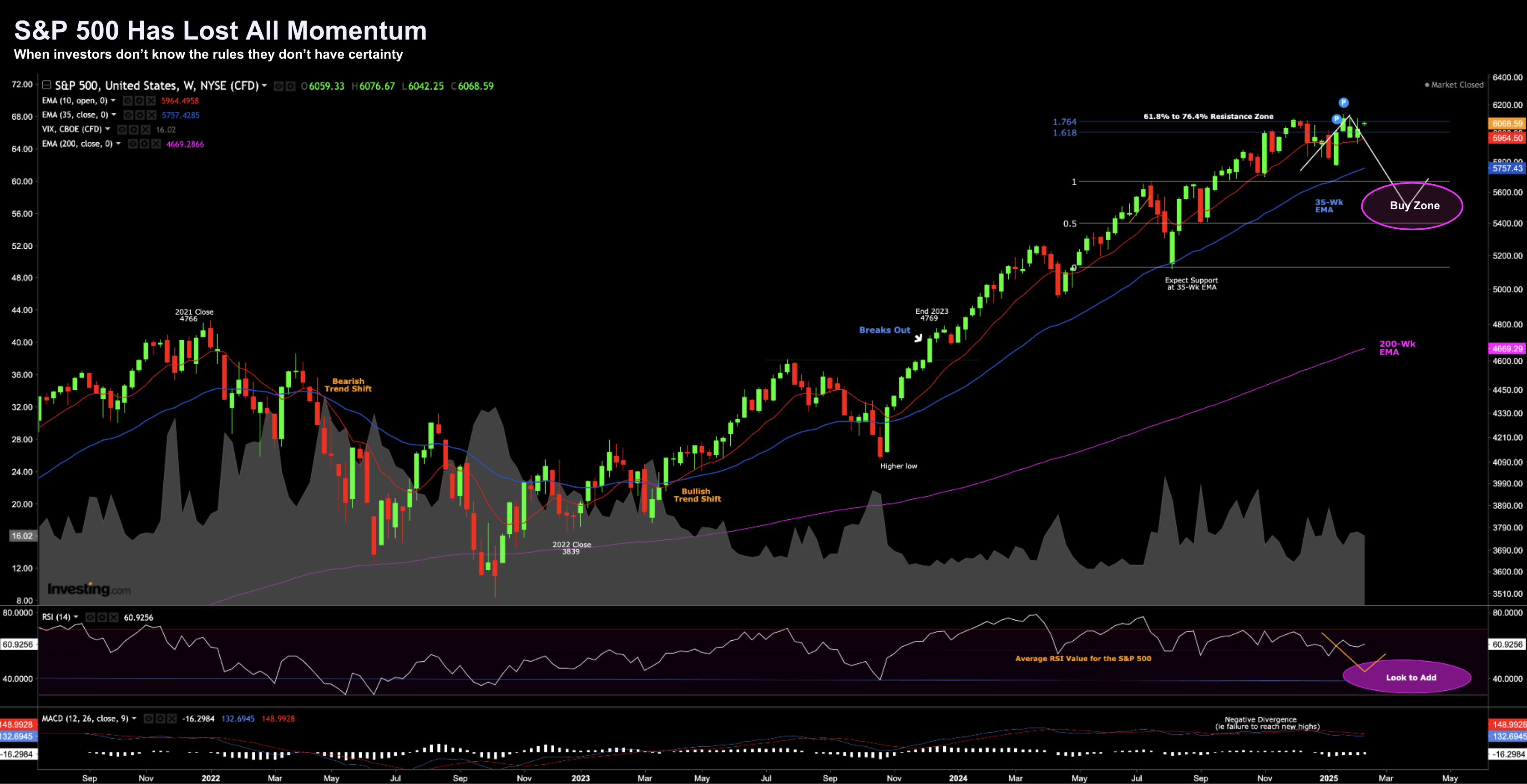

Since the initial post-election surge, the broader market has effectively stalled, marking nearly four months of horizontal movement with no net gains. From a technical perspective, two red flags remain prominent:

- Significant overhead resistance between the 61.8% and 76.4% retracement levels (specifically the 6100 zone); and

- Failing momentum, where the weekly MACD and RSI indicators are forming "negative divergences"—hitting lower highs even as prices attempt to push upward.

While timing a correction of 10% to 15% is a fool"s errand, the objective is not to predict the exact date, but to be positioned to capitalize when the valuation matches the value. My framework suggests a test of the 5600 zone is a mathematical probability when momentum fails to confirm price.

The Reciprocity Game: Trade as a Tactical Tool

The global trade landscape has shifted toward what I call "Symbolic Tit-for-Tat." While retaliatory tariffs often generate aggressive headlines, they are frequently more about political signaling than immediate economic destruction. However, investors cannot afford to dismiss these as mere bluster.

The push for reciprocity—the idea that any country taxing U.S. goods will face an identical duty—is the new baseline. When you consider that the average U.S. tariff is currently around 3%, while partners like India, Brazil, and China maintain averages between 10% and 13%, the gap for adjustment is significant.

In 2024, the U.S. goods trade deficit reached a record $1.2 trillion. According to Marketwatch data, the largest contributors to this deficit include:

- China: ~$295B deficit

- Mexico: ~$172B deficit

- Vietnam: ~$123B deficit

The "delicate dance" here is that the U.S. and China are so economically integrated that prolonged conflict harms both participants. As I noted in "Zero Sum Game", tariffs are rarely the long-term solution. However, they are an effective tool for forced negotiation. The goal for investors is to identify which companies can pass these costs through to the consumer and which will see their margins evaporate.

How the Market is Hedging

Smart money doesn"t wait for the headline to change; it watches the tape. Over the past several weeks, we have seen three distinct hedging behaviors:

- Gold: Pushing toward record highs as a classic "chaos" hedge;

- Commodities: A broad rise in input prices, anticipating supply chain friction; and

- Domestic Rotation: A pivot toward companies with U.S.-based revenue streams that are insulated from cross-border trade skirmishes.

The Defensive Strategy: The 15/15 Rule

In periods of high uncertainty, I rely on my 15/15 Rule to filter out the noise. This strategy requires a company to maintain a 15% Return on Equity (ROE) and a 15% Return on Invested Capital (ROIC).

Why these two metrics? ROE measures how effectively a company generates profit from shareholders" equity, while ROIC measures how well they deploy all their capital (including debt). A company that hits the 15/15 mark demonstrates a durable "moat"—they have the efficiency to survive trade wars and the pricing power to maintain margins even when tariffs rise. When the S&P 500 feels expensive, these are the only businesses worth holding through the volatility.

Summary: Patience Over Action

The recent earnings season for the "Magnificent 7" was telling. Only Meta saw a sustained rise, largely because they could prove the link between AI capital expenditure and bottom-line advertising returns. For the rest, the market is signaling caution.

Between record-high bond yields, a strengthening dollar, and shifting trade rules, the "unknowns" are currently outweighing the "knowns." Stay patient, keep your "powder dry" (cash on hand), and wait for the price to hit the zone where the math once again makes sense.