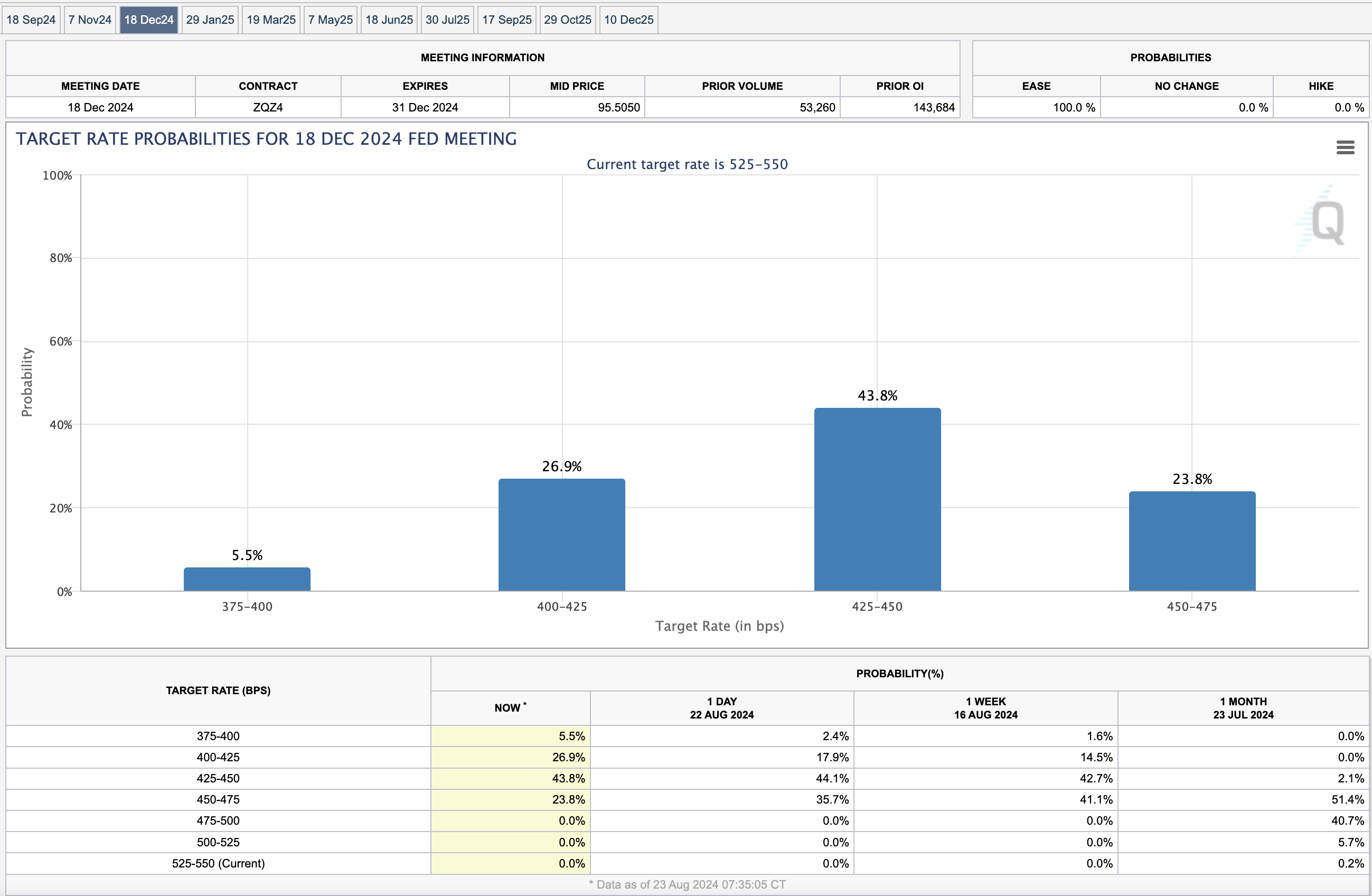

Powell Takes a Victory Lap

Powell Takes a Victory Lap

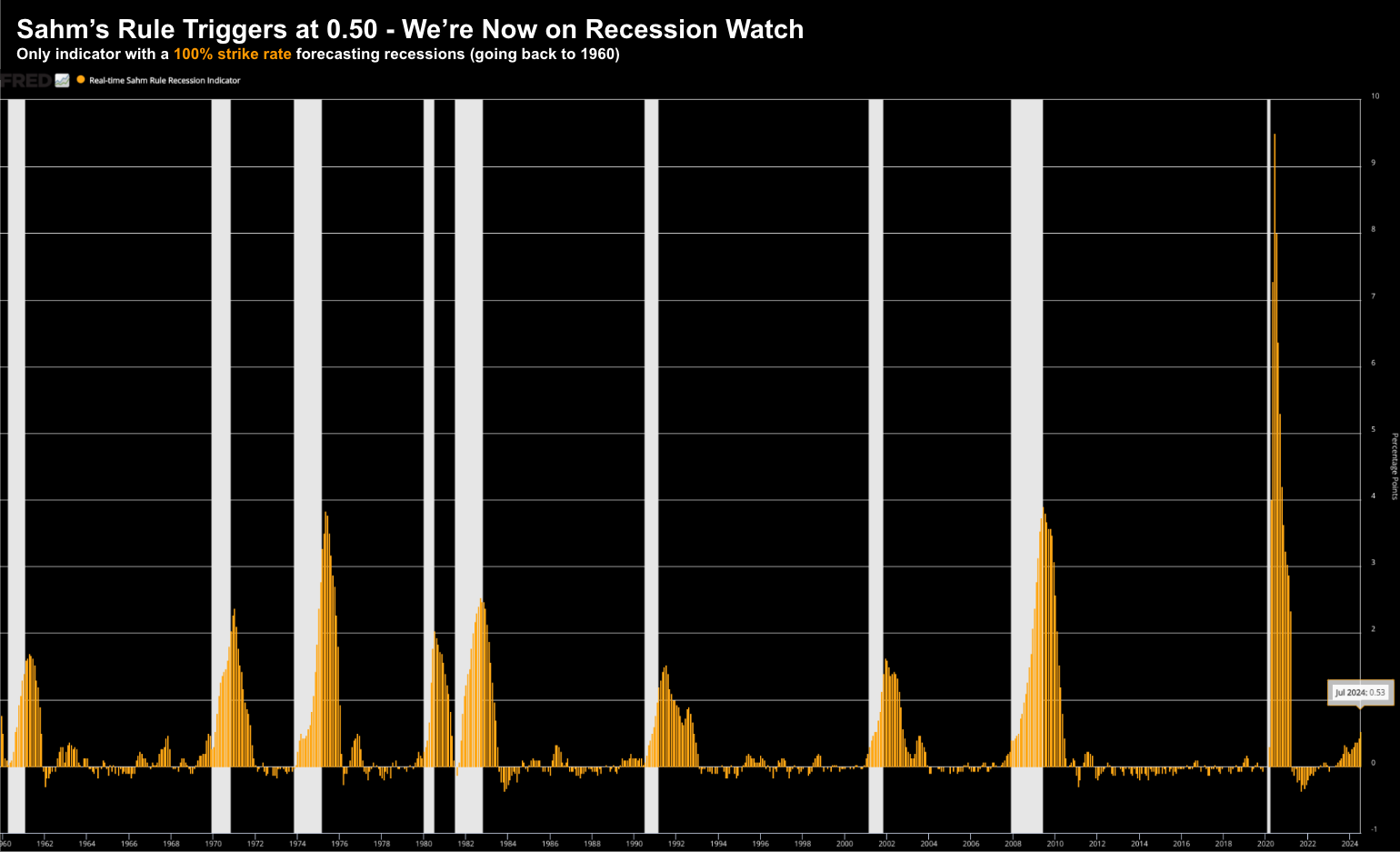

Fed Chair Powell didn't disappoint at Jackson Hole - giving the market what it wanted to hear... rate cuts are coming. All that remains how many and by when? That's not something Powell was ever going to offer (why remove optionality) - but the market is willing to bet we receive at least three cuts by year's end. All eyes now turn to two major economic reports: (i) PCE due Aug 6 and (ii) Aug nonfarm payrolls due Sep 6. For e.g., if Augusts payrolls are similar to June's (where only 114K jobs were added) - we could see the Fed cut rates 50 bps come Sept. What signal will that send to the market?