Bear Market Rally? Or Something More?

Bear Market Rally? Or Something More?

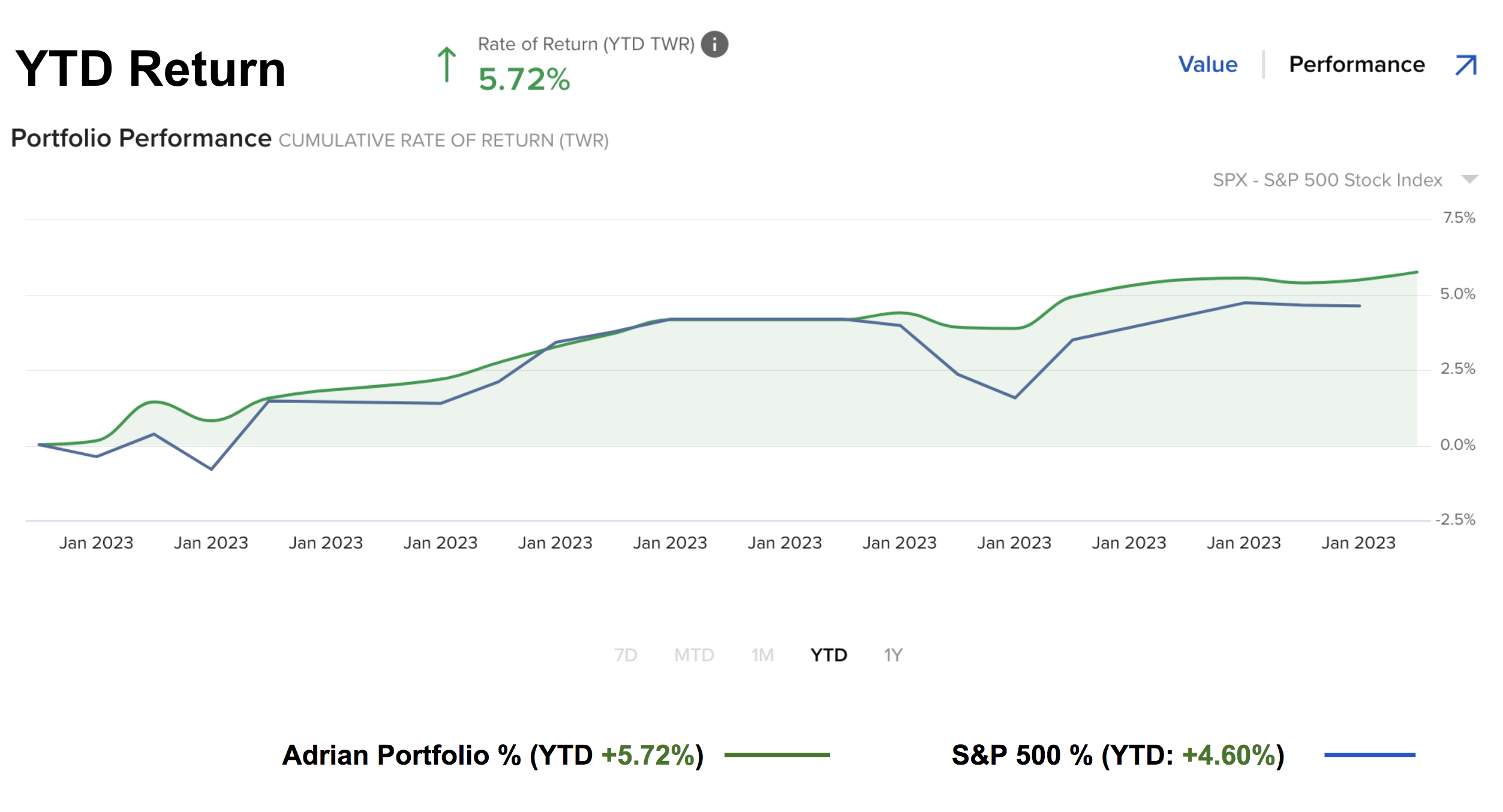

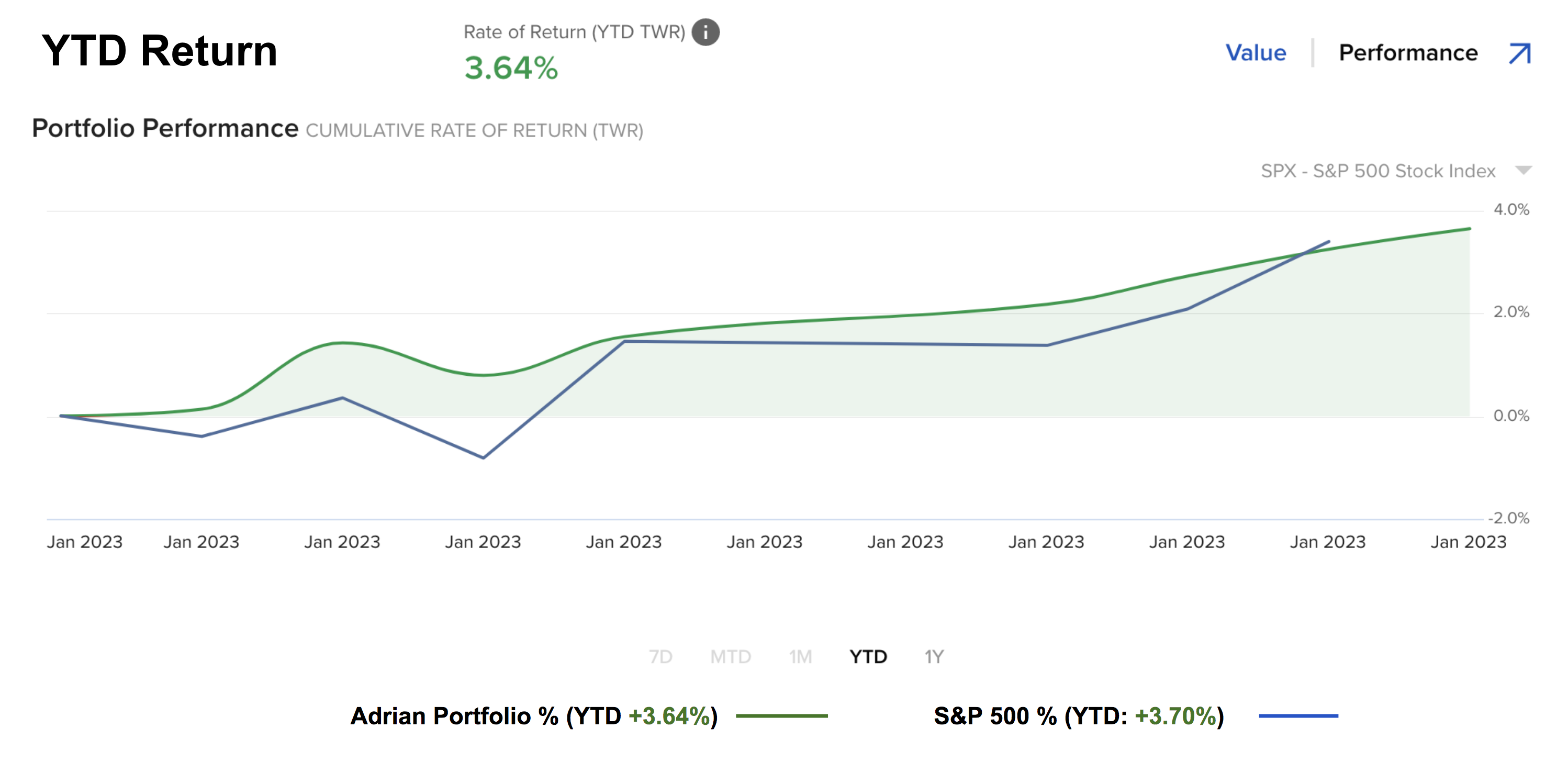

About 100 of the 500 S&P companies have reported Q4 2022 earnings. TL;DR is they are 'average' at best. Most have barely met already lowered expectations. What's more, forward guidance is weak. However, the bulls are betting on inflation continuing to plunge forcing the Fed to cut rates later in the year. I'm not yet prepared to support that thesis... with services inflation still running at 5.2%. There are some signs things are improving.