The Anatomy of a Growth Scare: How Tariffs, Tightening, and Inflation Impact Markets

Words: 1,260; Time: 7 Minutes

- The mechanics of a stalling economy: Why growth could falter in the months ahead.

- Policy friction: How "anti-growth" mandates offset tax cuts and deregulation.

- The ultimate indicator: Why Real PCE quarterly changes will warn us of a slowdown.

We frequently discuss the growing levels of uncertainty facing the market. Whether it involves impending tariffs, shifting monetary policy, or aggressive changes in fiscal spending, investors are finding it increasingly challenging to price the risks.

It is becoming incredibly difficult to forecast what policymakers will do next, and that unpredictability creates a ceiling for asset prices.

Let"s start with the Federal Reserve…

When we see hotter-than-expected inflation prints, the market is forced to rapidly re-price its expectations. Currently, markets are pricing in virtually zero rate cuts for the near future. Some analysts are even suggesting that should inflation remain stubborn, we could see a rate hike. That scenario is absolutely not priced into current equity valuations.

And when it comes to policy out of Washington D.C., the landscape is just as murky. Consider the current rhetoric surrounding tariffs:

- Broad tariffs on steel and aluminum across all countries.

- Targeted baseline tariffs on imported goods from China.

- Looming, paused, or negotiated tariffs on major trade partners like Mexico and Canada.

- The inevitable retaliatory tariffs from global partners defending their own industries.

All, some, or none of these things could permanently take effect. However, business leaders are already sounding the alarm. Ford"s CEO noted that sweeping tariffs would "blow a hole in the industry." Popular restaurant chain Chipotle stated that supply chain tariffs would immediately increase the cost of their meals. During recent earnings calls, approximately 60% of all companies cited the geopolitical trade situation as a material risk, though most admitted it is still too early to quantify the exact damage to their bottom line.

Regular readers will know my stance: broad tariffs act as a consumption tax (see "Zero Sum Game").

The optimistic view is that the threat of tariffs is primarily a negotiating tactic designed to secure better geopolitical deals. For example, using economic leverage to secure better border protocols, force trading partners to purchase more U.S.-made goods, or incentivize foreign corporations to build domestic manufacturing plants to avoid import taxes.

But we can"t be sure, and markets despise uncertainty…

This is precisely why the broader market indices have struggled to maintain momentum. We are currently facing the elevated risk of a growth scare.

The Push and Pull: Why Growth Could Stall

New political administrations are often initially viewed through a pro-growth lens, particularly when they promise to stimulate business. And that narrative is partially true.

For example, the primary pro-growth tailwinds typically include:

- Lowering corporate and individual tax rates.

- Aggressively removing layers of government regulation.

In short, the goal is to remove the "shackles from business"—getting government out of the way so the private sector has the capital and the incentive to invest and expand. Markets generally applaud this approach.

However, we must balance this against policies that are distinctly anti-growth:

- Strictly reducing immigration, which mechanically shrinks the overall labor force and drives up wages.

- Implementing broad tariffs, which drive up input costs for businesses and prices for consumers.

- Executing sweeping cuts to government spending and federal employment.

While current federal debt and deficit levels are mathematically unsustainable, the reality of fixing them is painful. From an investor"s perspective, when the government drastically cuts spending, the economy naturally contracts.

These restrictive policies offset the benefits of deregulation. Based on this lens, it becomes obvious why equities are failing to push into new territory. Investors are realizing a "growth scare" might be the necessary price for structural reform.

The Plumbing: Markets Have Yet to Recognize Tightening

Many factors push the price of equities higher: fiscal policy, tech innovation, earnings growth, and investor sentiment. But ultimately, the deepest driver of asset prices is the availability of money.

Abundant liquidity translates into higher asset valuations. If the taps are flowing—either from central bank easing or deficit government spending—equities will likely rise. However, if those taps are turned off, the market begins to fracture.

Here is the mechanical reality:

Over the last several years, we enjoyed extremely accommodative financial conditions. The government was spending at levels not seen since WWII (with the deficit-to-GDP ratio hitting 7%), and the Fed was broadly signaling a transition to rate cuts. Both are incredibly bullish signals.

However, investors must remember that economic data lags financial conditions by roughly 6 to 9 months. When commentators point to the current data and claim "things are very strong," they are looking through the rear-view mirror.

In reality, financial conditions have tightened considerably. Look at the trajectory of the US 10-year yield—the benchmark that dictates the rate on mortgages, car loans, and corporate debt.

US 10-Year Yield Snapshot

This surge has made borrowing exponentially more expensive for businesses and households alike. It leads directly to a tightening of credit availability and drastically higher debt servicing costs. This is a massive headwind for economic growth that has yet to fully show up in corporate earnings.

It comes down to Econ 101:

When you make something cost more (in this case, capital), you should expect less of it to be used.

With the yield curve heavily flattened for the next three to four years, the bond market is telling us to expect very few rate cuts into 2026 and 2027. Let"s connect the macro dots:

- Tightening financial conditions driven by stubbornly high bond yields;

- Restrictive policies including reduced immigration, increased tariffs, and slashed government spending;

- Resulting in overall demand falling, input prices rising, and macro growth slowing.

Remaining Agile: Watching the Labor Market

An aggressive trade war is only one catalyst for a growth scare. If we look under the hood of the broader economy, there are other cracks forming.

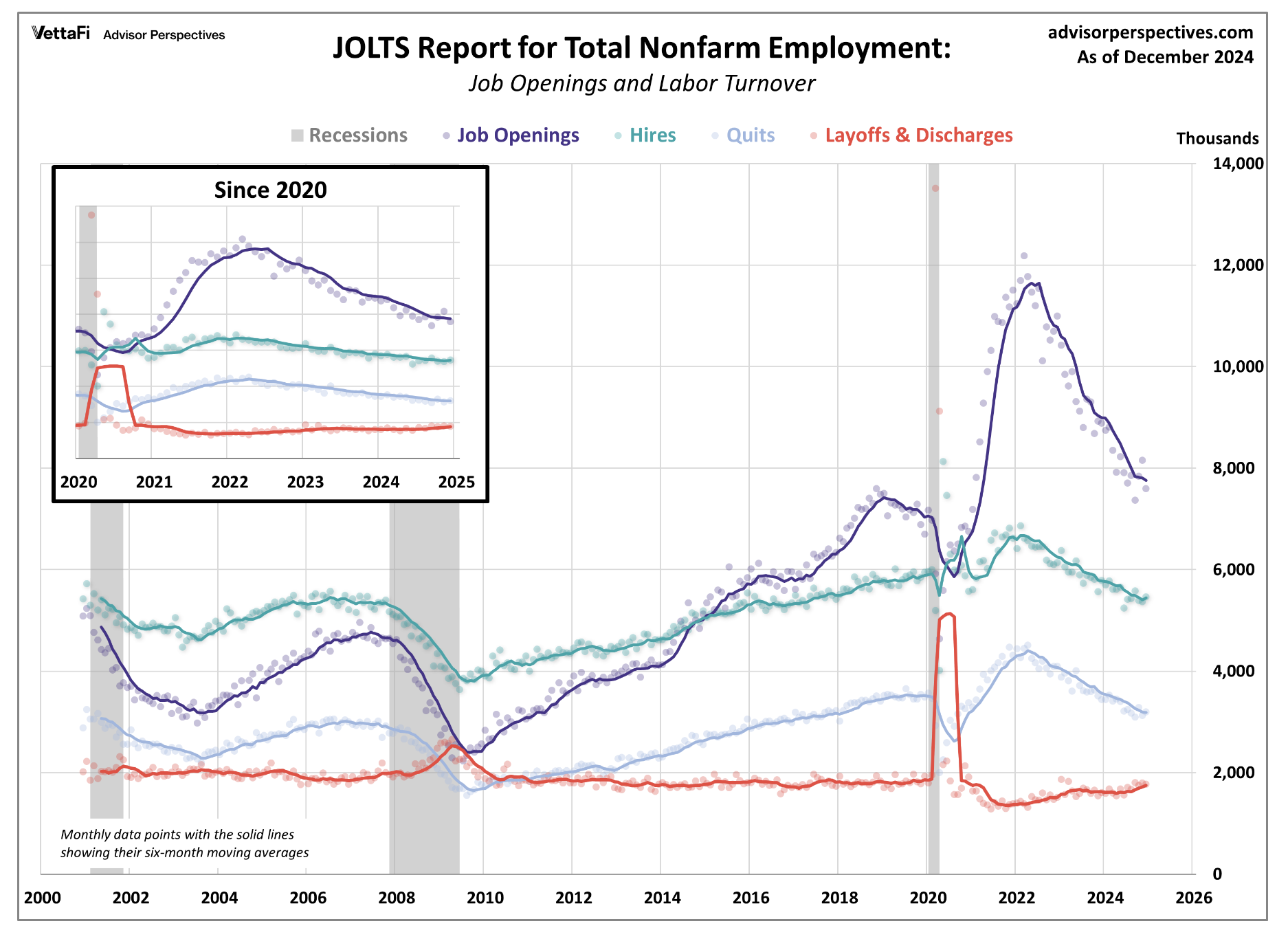

The JOLTS survey has consistently revealed a sluggish hiring rate, indicating a low-velocity labor market. Notice the downward trend of the purple line (job openings) while layoffs (the red line) begin to tick upward.

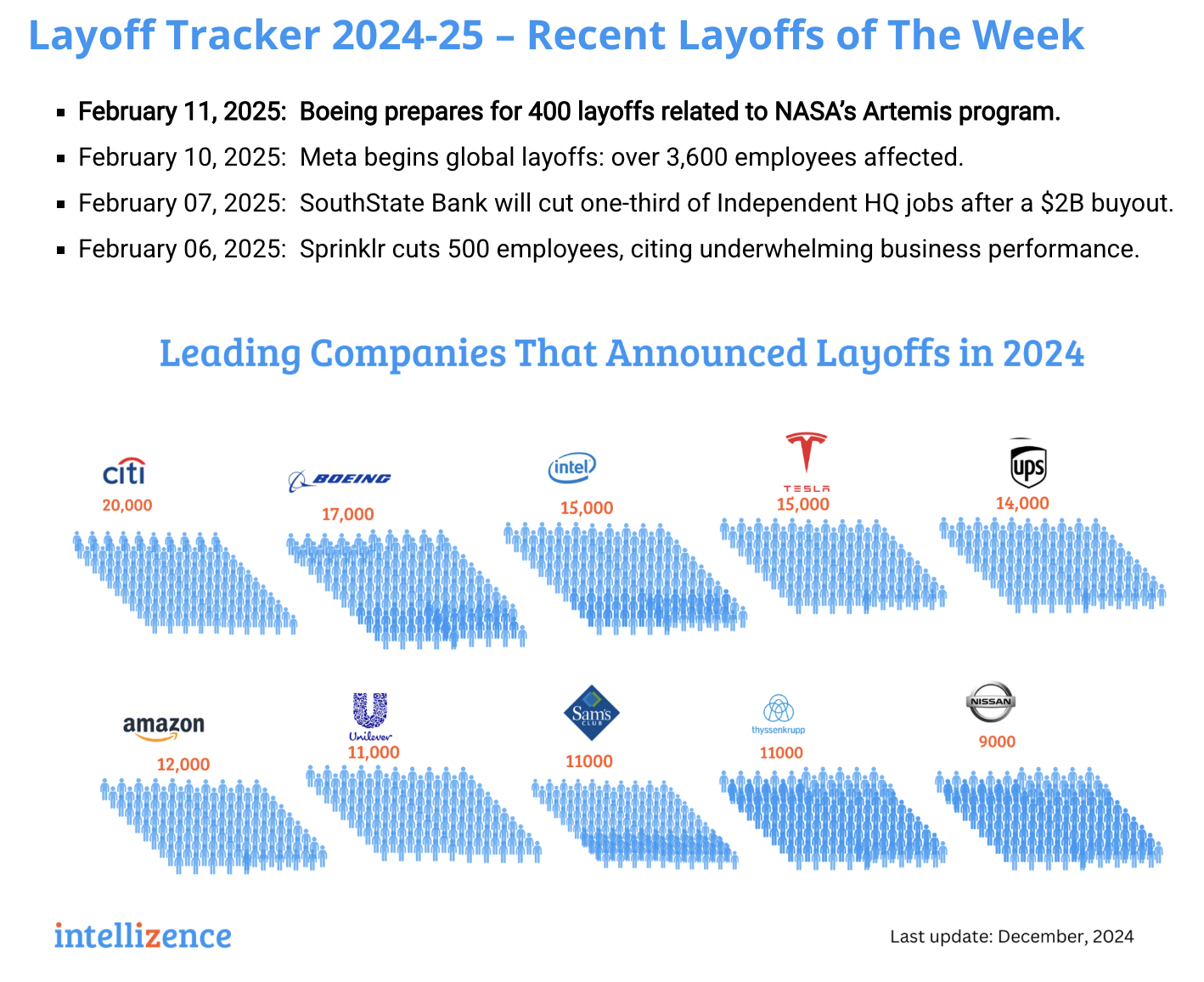

We are witnessing high-profile corporate restructuring accelerate. Recent examples include:

- Chevron announcing layoffs affecting 20% of its global workforce.

- Meta cutting thousands of operational roles.

- Google offering 25,000 voluntary redundancies to staff in its Platform & Devices business.

Here is data compiled by Intellizence detailing the scope of these corporate reductions:

This is the metric to watch.

If interest-rate-constrained consumers—fearful of a cooling job market—begin spending less at the exact moment the government withdraws fiscal liquidity, economic growth will stall.

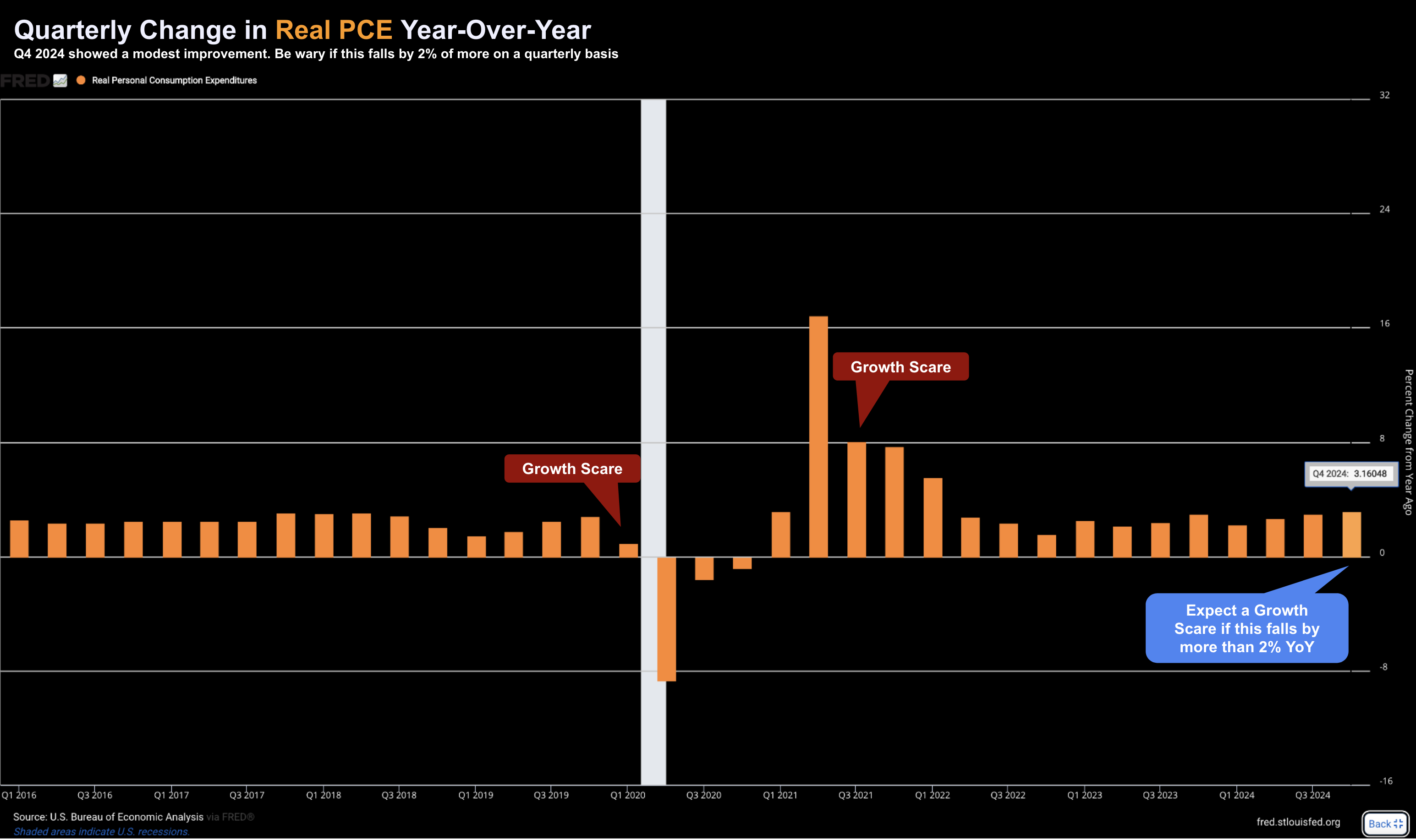

I will be keeping a very close eye on the quarterly year-over-year change in Real PCE (Personal Consumption Expenditures). The consumer is the undeniable engine of the US economy. If we see Real PCE drop more than 2% year-over-year on a quarterly basis, a significant growth scare is all but guaranteed.

Putting it All Together: Defense via the 15/15 Rule

We entered the year with markets priced for perfection, banking on a friendly Fed, massive deregulation, and the limitless promise of AI. Investors were willing to pay exorbitant valuation multiples, essentially crowding onto one side of the boat.

But as momentum stalls and anti-growth policies offset the tailwinds, that uncertainty causes capital to pull back. So, how do we navigate this?

When macro uncertainty rises, the best defense is moving up the quality curve. This is exactly where my 15/15 Rule becomes non-negotiable. To insulate a portfolio from a growth scare, I look exclusively for businesses capable of generating a 15% Return on Equity (ROE) and a 15% Return on Invested Capital (ROIC).

Companies that meet this strict 15/15 threshold possess wide competitive moats. They generate enough internal free cash flow to fund their own growth, meaning they don"t have to borrow at 5% to keep the lights on. They have the pricing power to survive tariffs, tightening credit, and slower consumer spending. In an environment where the "perfect storm" of macro risks is gathering, holding cash and waiting for 15/15 companies to trade at a fair valuation is the ultimate margin of safety.