Show Me the Money!

- Market sentiment shifts from AI hype to demanding cash flow

- Private credit cracks widen as risky lending schemes collapse

- High valuations risk compression as growth stories meet reality

February was not overly kind to stocks.

As I"ve shared in recent posts – software and financial stocks ended the month bruised and battered.

However, other sectors such as energy and staples posted gains.

My last post mentioned I was watching the selling in the financial sector closely (due to its potential impact on the economy).

The selling in financials was particularly sharp Friday – as "fresh cockroaches" emerge.

Names like Goldman Sachs lost 7.5%

This time a little known UK mortgage-finance company – Market Financial Solutions (MFS) – collapsed.

Behind that company where Barclays and Atlas Partners — the structured-credit arm of Apollo Global Management — who arranged more than $2.7 billion of loans.

Jefferies Financial Group and Wells Fargo are also among those with exposure.

The unraveling of MFS further underscores the importance of my previous post; i.e., the loose underwriting in credit markets.

When you have been lending money at this scale ($1.8 Trillion post 2008) – at this velocity – you sacrifice quality.

In short, firms lent money too quickly on terms no prudent banker would accept.

That"s a recipe for disaster.

For example, last year we saw the bankruptcies of US auto parts supplier First Brands Group and sub-prime auto lender Tricolor Holdings.

That"s the thing with cockroaches… rarely is there just one.

"Show Me the Money"

If I could use a word to describe the start of this year – it"s skepticism.

The market is now starting to question things like (not limited to):

- What level of job layoffs will AI cause (see here and here)?

- What is the scale of private credit "cockroaches" in the market? and

- How much will AI replace software?

Up until 2026 – the market was happy buying into all things "AI".

It didn"t matter who the borrowers were; if the deals were circular in nature (more on that below); or even how much cash flow AI would absorb.

All that mattered was you didn"t want to miss out on catching the next "big thing".

This is no different to the PC revolution in the 1980s; and the dot.com fever in the mid 90s. Today we can simply substitute PC or Internet for "AI".

It"s the same movie repeating.

However, now the market is saying "show me the money"

Jerry Maguire was asking the right question…

For example, lets say you are spending "$100B in Capex" – investors are asking:

- What are your earnings going to be?

- What"s your free cash flow?

- What"s your operating margins?

- What"s the return on that incremental $100B (will it exceed the previous $100B?) and

- What"s the business model and how does it differentiate? etc

These are very difficult questions to answer and not intended to be exhaustive.

I don"t think anyone knows.

This was punctuated this week with what we saw from AI company CoreWeave (CRWV)

For those less familiar – it"s a cautionary tale – piecing together various components of the AI bubble.

Blue Owl Capital (see this post), which is co-developing a large AI data center in Pennsylvania (where CoreWeave would be the anchor tenant), failed to line up external lenders for as much as ~$4 billion in financing for that project.

Lenders were reportedly hesitant because CoreWeave has a below-investment-grade credit rating (B+/BB-), making them reluctant to participate.

Following the news of Blue Owl"s funding difficulty, CoreWeave shares tumbled and investor concern grew about how future projects would be funded without broad lender support.

Enter Nvidia (NVDA).

Nvidia has made direct "strategic investments" in CoreWeave — about $2 billion this year — and agreed to purchase large amounts of CoreWeave capacity (and stock), helping underpin financing that might otherwise be hard to get from traditional lenders.

But from mine, I see potential red flags with these types of circular deals (which have become common place – something we also saw during the dot.com bubble):

- Credit, equity, and operating relationships are intertwined.

- Stress in one node can propagate quickly.

- Growth optics can look stronger than underlying free cash flow.

These questions are now showing up in equity and bond markets (evidenced by some of the price action)

That is, the overall sentiment of investors is shifting from a "fear of missing out" to "what is the reality?"

"Trust Me"

In late 2025 on the "Bg2 Pod" podcast with Brad Gerstner — Sam Altman (CEO of OpenAI) a response to a question which troubled me.

In the interview, billionaire hedge fund manager Gerstner pressed Altman on a central concern of investors and analysts:

How can a company with reported revenues of roughly $13B a year commit to spend over $1.4T on compute and data-center infrastructure through the 2030s?

Instead of walking through a clear business model or financial plan, Altman chose to dismiss the premise entirely.

This was his answer: "If you want to sell your shares, I"ll find you a buyer… enough."

Altman does not have an answer to a pertinent question – resulting in him getting defensive.

Gerstner had backed him into a corner.

That wasn"t just a neutral statement — it a non-answer to the core question of how the unit economics of AI make sense.

Today they don"t. Investors are hoping tomorrow they will.

For me, this exchange simply highlighted the asymmetry between massive planned spending and current revenue levels — something almost unique in corporate history.

Instead of outlining a credible multi-year profit model, Altman chose a deflective market-confidence response.

This is why the market (perhaps since around September last year) – is now taking stock of just where things stand.

And in that sense – 2026 will be a "show me the money" year.

Nvidia: Beat & Raise Not Enough

One final data point before I wrap things up…

This week the market was sweating on results from NVDA – arguably the AI poster child – and largest capitalized stock on the S&P 500.

First the blow-out numbers from CNBC:

- 75% revenue growth in its core data center business.

- $1.62 EPS adjusted vs. $1.53 estimated

- $68.13B Revenue vs. $66.21B estimated (up 73% YoY)

- Net income almost doubled to $43 billion YoY

- GAAP Gross Margins were 75% (indication of their sheer pricing power)

Interestingly, 91% of sales ($62.3B) were from its data center unit, which houses its AI chips.

Forward guidance was also better than expected.

NVDA said revenue for the fiscal first quarter will be ~$78 billion vs expectations $72.6 billion.

On the surface, this level of revenue and net income growth – at 75% gross margins – would blow away the street. They are astounding results by any measure.

But not in this climate...

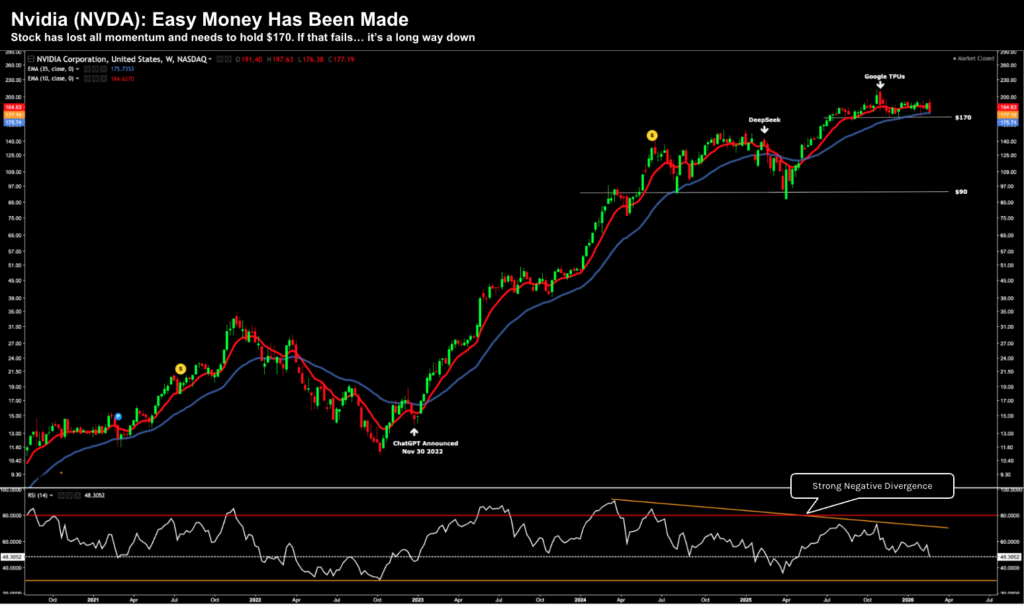

The stock failed to post gains on the news – falling over 5%

Technically the stock has lost all of its momentum.

Note the strong negative divergence in lower window – the weekly Relative Strength Index (RSI).

It has made a series of lower highs whilst the stock made higher highs. Quite often this will result in selling pressure.

In addition, the stock has failed to make any ground since July last year.

As an aside, consumer staples have outperformed NVDA over the past 12 months.

I think the market understands the game only gets harder for NVDA from here.

Yes, they have an exceptionally strong market position with their technology and install base.

But alternatives are coming…

They are not only coming from other chip makers – but also from their customers (e.g., Google, Amazon, Microsoft all now scaling their own chips)

From a fundamental perspective – I don"t think NVDA represents strong value.

Now some analysts will argue from a forward (2027) PE basis, it trades at ~24x (based on expected "27 EPS of $7.60)

However, earnings are a lazy (overly generalized) metric.

- If we use EV/EBIT multiple (which brings the balance sheet to the multiple) – that ratio expands to 33x (not cheap); and

- If we use price to free cash flow (P/FCF) – it"s a rich 44.5x

I will be the first to say this company deserves a premium to the market.

No question.

But how much of a premium?

I think the stock will pause – affording those who are patient to buy this quality stock at a much lower multiple.

Putting it All Together

Despite the recent bruises in software and financials, the broader market still trades above 21x forward earnings.

That"s far from a discount.

This multiple is largely driven by the assumption that AI capital expenditures will seamlessly translate into massive, high-margin profits for those involved.

I remain less convinced. It"s a giant leap of faith.

From mine, the "unit economics" of this transition are still unproven.

When a stock like Nvidia doubles its net income, grows revenue by 73%, and maintains 75% gross margins—yet the stock falls 5%—it tells you one thing: the good news was already priced in.

The market is no longer paying for growth; it is demanding certainty. And right now, certainty is in short supply.

The danger for the average investor today isn"t missing the next rally; it"s getting caught in the "multiple compression" that happens when a "growth story" transitions into a "show me" stock.

Some back of the envelope math:

If you buy a stock at 45x Free Cash Flow (like Nvidia today), you are effectively accepting a ~2.2% earnings yield.

In a world where risk-free Treasury bonds offer 4% or 5%, you are taking on massive equity risk for a lower immediate return.

Why take that risk?

On that basis – I can"t say with confidence that NVDA is an attractive buy – not at ~$200.

And as surface cracks in private credit and the circular financing of AI startups suggest, the future might be more expensive and less profitable than the models predict.

As I"ve said in previous posts – this is not a call to sell everything and hide in cash.

That would also be a mistake.

I remain ~65% long – where I own quality names like Microsoft (MSFT), Amazon (AMZN) (both of which I added to recently) and Google (my largest position)

And if I am lucky enough to see MSFT and AMZN trade ~15% lower from there – I will increase my position.

Bottom line:

If you own high-quality assets with fortress balance sheets, hold them.

I prefer to own companies that generate their own cash, not companies that need to borrow it from "Nvidia" or a "Blue Owl" to survive.

Caution is not pessimism; it is simply the price of admission for the patient investor in 2026.