Why Warren Buffett Bought SiriusXM: A Deep Dive into ROIC, Cash Flow, and Value Trap Risks

Words: 2,150 Time: 9 Minutes

- Is SiriusXM (SIRI) a classic value-trap or a misunderstood cash machine?

- Why Buffett sees limited long-term downside at low valuations; and

- Key quality metrics which suggest it"s potentially undervalued

In previous analyses, I have offered readers a framework to evaluate the intrinsic quality of a stock and determine whether it represents true value.

This approach heavily leverages the methodologies of proven value investors, most notably Warren Buffett. Buffett places significant, almost exclusive, emphasis on two critical pillars when analyzing businesses: Free Cash Flow (FCF) and Return on Invested Capital (ROIC).

He is not governed by fleeting metrics like top-line revenue beats or temporary earnings growth. He demands a sustained return on invested capital, but crucially, he is only willing to pay a "fair price" (or secure a deep discount) to acquire those cash flows.

Here is how these core metrics align with his operational philosophy:

The Power of Free Cash Flow and ROIC

With respect to FCF, Buffett frequently discusses the concept of owner earnings—a metric virtually synonymous with free cash flow. He defines owner earnings as the cash flow available to shareholders after all necessary reinvestments (CapEx) are made to maintain the business"s competitive position.

This aligns perfectly with FCF because it isolates the capital a company generates that can be freely distributed or strategically deployed. A robust FCF profile demonstrates:

- The company"s ability to generate real, unencumbered cash that owners can extract;

- Management"s flexibility for intelligent capital allocation—be it strategic acquisitions, dividends, or share buybacks; and

- Assurance that reported earnings are not just accounting illusions ("paper profits") but translate directly into tangible wealth creation.

In terms of ROIC, while Buffett may not always use the exact academic acronym in his annual letters, his relentless focus on businesses with durable competitive advantages (economic moats) inherently favors companies that exhibit high ROIC.

He pursues businesses capable of generating exceptional returns on the capital they retain and reinvest for three fundamental reasons:

- High ROIC over a sustained period (e.g., a decade) proves the efficient use of shareholder equity.

- Companies boasting strong ROIC almost always possess sustainable competitive advantages, such as absolute pricing power, unassailable brand strength, or structural cost leadership.

- A high and consistent ROIC mathematically ensures the company compounds intrinsic value, actively adding wealth for shareholders over time.

The 94-year-old oracle consistently highlights that exceptional businesses can reinvest capital at high rates of return, compounding their growth internally without relying on external debt or dilutive equity offerings.

To put this in perspective, consider the 10-year average ROIC and ROE for Berkshire"s top holdings:

| 10-Yr Avg ROIC % | 10-Yr Av ROE % | |

| Apple (AAPL) | 39.1% | 85.9% |

| American Express (AXP) | 11.3% | 17.3% |

| Bank of America (BAC) | 10.7% | 8.1% |

| Coca-Cola (KO) | 11.8% | 31.4% |

| Chevron (CVX) | 4.2% | 6.4% |

Note: CVX was significantly impaired by global macroeconomic shutdowns during recent market disruptions—however, its most recent full year showed a normalized ROIC of 17%.

The central takeaway is that these businesses can sustain operations and grow without needing to dilute equity or take on ruinous debt.

This context brings us to Buffett"s seemingly contrarian move: a meaningful addition to his existing SiriusXM (SIRI) position.

A superficial glance might lead investors to label this stock a classic value-trap. The prevailing narrative is that SIRI"s satellite radio model is actively being cannibalized by ubiquitous smartphone streaming applications like Spotify and Apple Music.

And that narrative holds weight…

However, reality is more nuanced. SIRI maintains a commanding 60% market share of the in-car "fixed audio" hardware market, entrenched by deep, long-standing partnerships with major automotive manufacturers.

While premium subscription counts have faced headwinds, the company is actively re-architecting its pathway to market by implementing:

- Granular content bundles (i.e., lower-priced, segmented plans);

- A brand new, strategically targeted ad-supported (free) tier;

- Highly exclusive, proprietary content offerings; and

- Enhanced digital functionality (e.g., the ability to curate and save music to custom playlists).

Analyzing the SIRI Investment Thesis

For those less familiar with the operational model, Sirius XM Holdings Inc. (SIRI) operates primarily as a subscription-fee-based satellite radio provider in North America.

The enterprise broadcasts a massive ecosystem of music, live sports, premium entertainment, comedy, talk shows, news, and vital location-based services (traffic, weather, remote vehicle diagnostics, and security features).

Beyond satellite transmission, they deploy a robust streaming service targeting smartphones, smart home devices, and connected vehicle hardware. Crucially, they control their distribution channel through aggressive, embedded agreements with automakers and national retailers.

Berkshire Hathaway now commands approximately 33.2% of SIRI, as Buffett persistently acquired shares while the broader market pushed the price lower.

This aggressive buying occurred even as SIRI faced operating headwinds, shedding subscribers, top-line revenue, and profit margins, which culminated in a massive "refocusing" initiative late in the year.

While future growth expectations have been rationally re-rated lower by management, the company is doubling down on its "core" automotive customer base, concurrently executing an additional $200M in structural cost cuts.

The macroeconomic and competitive challenges facing Sirius are structural and not insignificant:

- The modern consumer defaults to streaming services (Apple Music, YouTube Premium, Spotify) for frictionless audio consumption.

- Inflationary pressures have made consumers incredibly price-sensitive, triggering audits of monthly recurring subscriptions (making in-car audio plans vulnerable to cancellation).

- Scaling international market penetration has proven historically difficult and capital-intensive.

However, management is not sitting idle. They have engineered a specific, three-pronged operational pivot to counter these threats:

- Category Segmentation: Content is being disaggregated into distinct category blocks. Rather than a monolithic expensive package, offerings include a music-only tier for $8 p/month, news and talk radio for $5 p/month, and premium sports for $8 p/month.

2. The Ad-Supported Pivot: Borrowing a page directly from the Netflix playbook, they are launching a new free tier heavily supported by digital ads. While currently restricted to vehicles featuring specific technological integrations (and notably absent from the mobile app), this will scale linearly as automotive fleet tech upgrades naturally occur.

3. Product Enhancement: The premium tier is being upgraded to an "Interactive Premium" bundle, allowing users to save tracks, build custom playlists, and engage with content dynamically (directly attacking Spotify"s value proposition).

Of these initiatives, the free tier with targeted ads holds the highest probability of structural success. It mirrors the exact monetization mechanism legacy radio has exploited for a century.

Consumers possess an insatiable appetite for "free" content. Furthermore, modern programmatic digital advertising tools allow publishers to secure significantly higher ad yields through hyper-precise demographic targeting.

As evidence, Netflix is rapidly scaling its subscriber base via its ad-supported tier, proving the commercial viability of this pivot.

This strategy is not without risks. As users migrate to cheaper tiers, the Average Revenue Per User (ARPU) will inevitably contract. The thesis relies on volume offsetting that contraction.

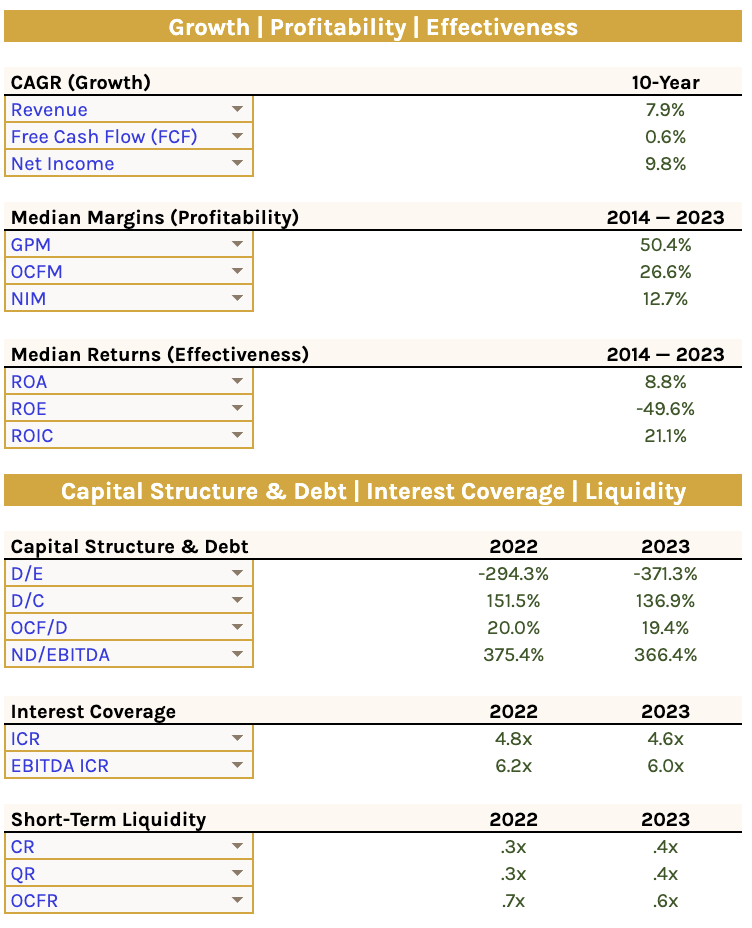

Applying the 15/15 Rule to Quality Metrics

Before analyzing the valuation multiples, we must subject the business to a rigorous quality audit. My preferred framework is the 15/15 Rule, which demands a company consistently output at least a 15% Return on Equity (ROE) and a 15% Return on Invested Capital (ROIC). This strict hurdle separates durable economic compounders from capital-destroying mirages.

When mapping these quality metrics over a decade, utilizing decisional quadrant charts with specific color-coded verdicts provides much more clarity than simple informational charts. It immediately flags whether a business has the operational engine required to justify capital allocation.

Growth, Profitability, and Efficiency Observations:

- The 10-year average Return on Invested Capital (ROIC) easily clears the 15/15 Rule hurdle, sitting over 21%.

- Profitability remains incredibly robust, with a 10-year Net Income Margin (NIM) of 12.7%—comfortably above broader market averages.

- The Operating Cash Flow Margin (OCFM) sits at a stellar 26.6%.

OCFM is a critical barometer; it confirms the true structural strength of a company"s day-to-day operations and validates the reality of its reported earnings. Buffett zeroes in on metrics exactly like ROIC and NIM while largely ignoring headline revenue growth.

When analyzing the cost structure and operational margins, it is also useful to view the business through the lens of the 55/30/25 Model. This model targets ideal corporate efficiency: 55% Gross Margins, 30% SG&A (Selling, General, and Administrative expenses), and 25% EBITDA margins. Companies that operate near these ratios typically have pricing power and disciplined cost controls.

Capital Structure, Debt, and Liquidity Observations:

- Historically (pre-2023), the company carried a troubling Debt to Equity (D/E) ratio of -371.3% (where total liabilities eclipsed assets).

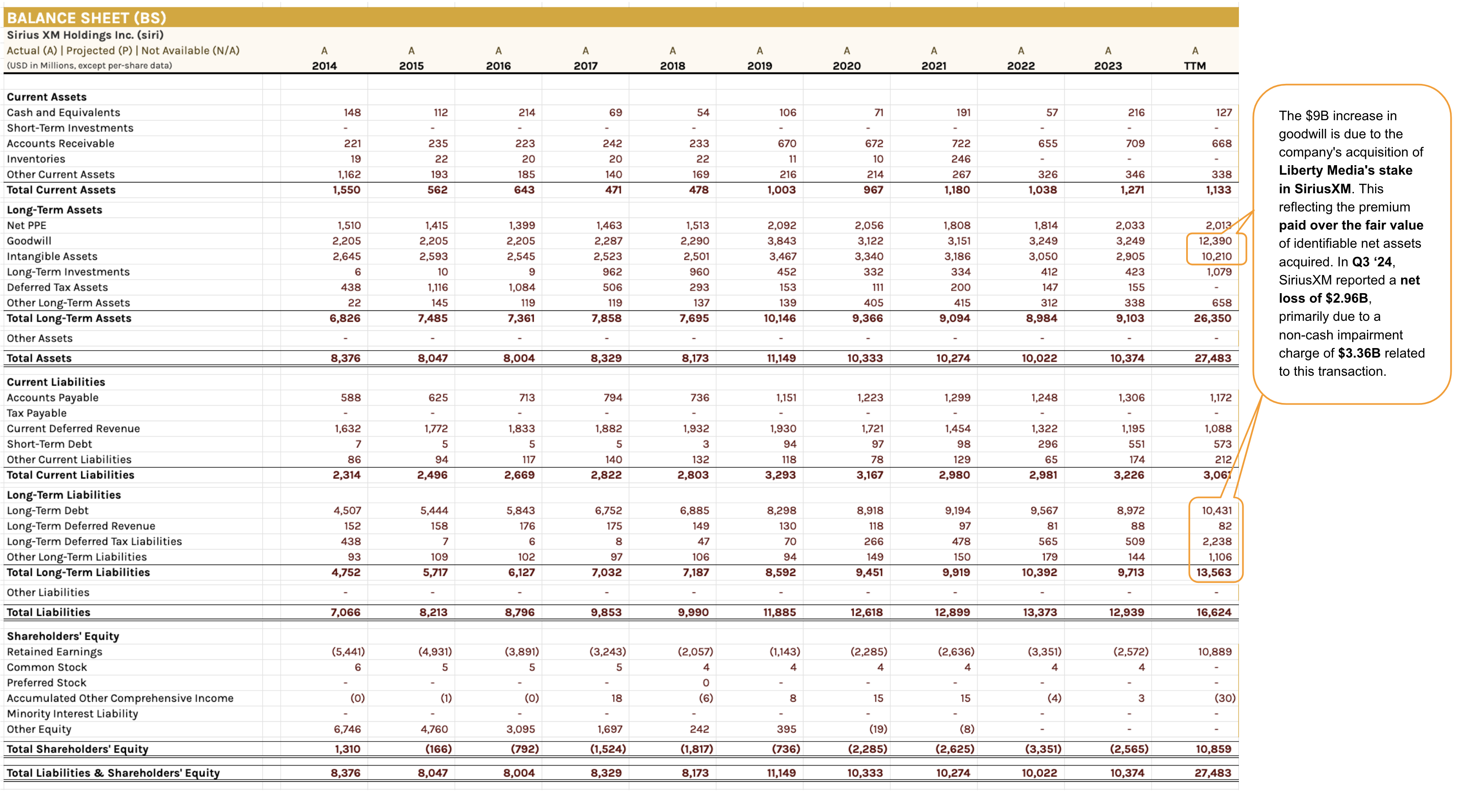

- However, analyzing Trailing Twelve Months (TTM) data reveals a massive $9B increase in goodwill, directly stemming from the strategic acquisition of Liberty Media"s stake.

- Note: Goodwill is an accounting mechanism representing the intangible value acquired, encapsulating brand equity, subscriber lists, and projected operational synergies.

- Recently, SIRI reported a heavy net loss primarily driven by a massive non-cash impairment charge of approximately $3.36B connected to this transaction.

Source: Personal Spreadsheets

- It is vital to recognize that while this impairment crushes reported net income on paper, it does not impair actual cash flow, day-to-day business operations, or corporate liquidity.

- The company maintains a highly defensive EBITDA Interest Coverage Ratio (ICR) of 6.0x—meaning they can service their debt obligations six times over using operating profits.

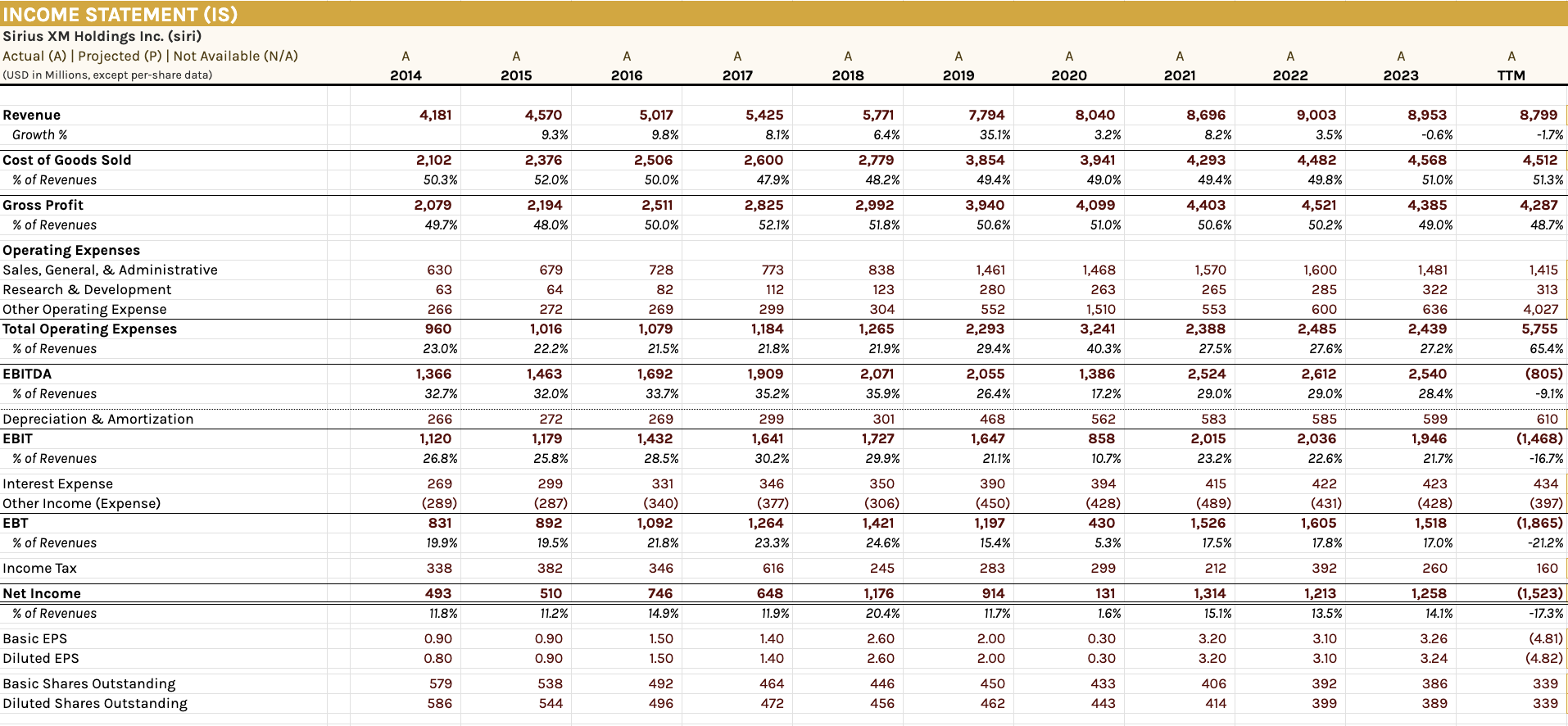

In summary, despite surface-level accounting losses, the past decade proves SIRI possesses elite returns on invested capital, healthy margins, and exceptional free cash flow generation. Revenue will experience turbulence as the ad-tier rolls out, but the cash engine remains intact.

Source: Personal Spreadsheets

The Valuation Argument

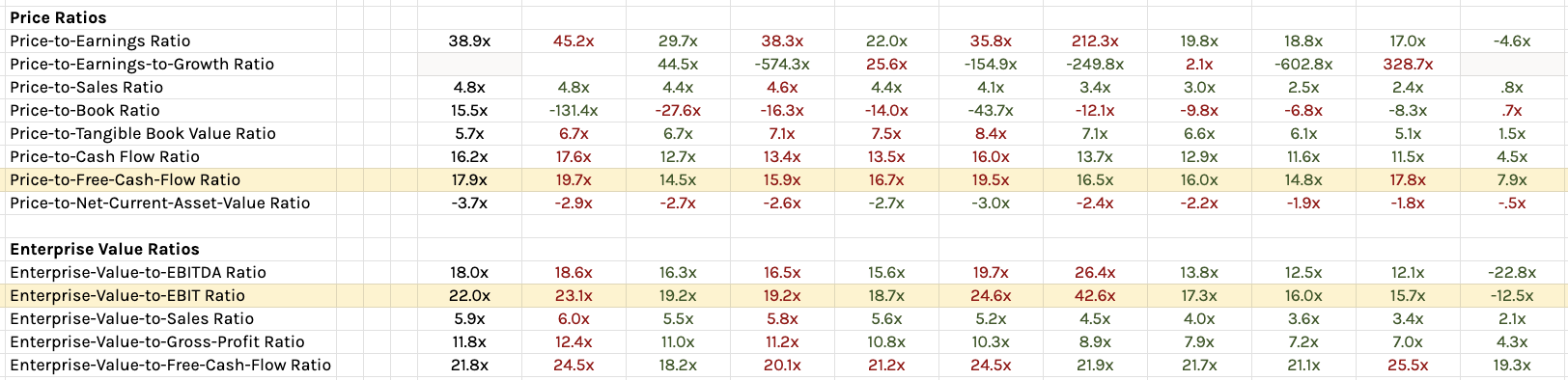

A high-quality business only becomes a great investment at the right price. When analyzing non-cyclical assets with a demonstrable moat, a solid guardrail is targeting an EV/EBIT and Price/FCF multiple between 15x and 20x.

Buffett"s aggressive accumulation is almost certainly driven by SIRI trading far below these historical guardrails.

Looking at previous years, SIRI"s P/FCF hovered between 14.8x and 17.8x, perfectly aligned with the 15x-20x fair-value parameter. EV/EBIT also traded fairly around 15.7x.

Today, the valuation metrics have completely decoupled from fair value:

- P/FCF has collapsed to roughly 7.9x.

- EV/EBIT appears distorted (negative) due entirely to the aforementioned $3.36B non-cash impairment.

If we adjust for the non-cash charge, EBIT normalizes positively, though it remains marginally lower year-over-year due to the anticipated drop in active subscriptions.

Consider the math: At a 7.9x free cash flow multiple, the company is yielding an incredible ~12.7% on its cash generation. Coupled with a historical baseline of 20%+ ROIC and a dominant 60% share of the vehicle hardware market, Buffett likely views the current pricing as severely mismatched with the actual cash reality of the firm.

The success of the investment hinges on whether management can successfully execute the "Netflix pivot" and stabilize ARPU with the introduction of programmatic audio ads. Upcoming quarterly metrics regarding self-pay subscriber retention and ad-tier conversion will dictate the timeline of the turnaround.

Putting it All Together

Buffett relentlessly hunts for enterprises possessing durable, long-term competitive advantages. Controlling 60% of the "fixed" in-car audio real estate represents a formidable moat, the threat of smartphone integration notwithstanding.

To reinforce this moat, SiriusXM maintains contractual strangleholds with automotive manufacturers. Recent agreements, such as Toyota and Lexus bundling 3-year extended subscriptions with new vehicle purchases, ensure that Sirius remains the default audio interface for millions of consumers.

The core thesis of this value play is simple: When you purchase a cash-generating asset at a 7.9x free cash flow multiple (more than 50% below the median market valuation), the company does not need heroics or massive revenue growth to justify the price. They simply need to maintain stability.

Add in an extremely solid dividend yield of ~4.0% (roughly triple the S&P 500 average), and investors are paid handsomely to wait for the market to re-price the asset.

This is precisely why SIRI does not look like a traditional "value trap". Revenue may stagnate in the short term, but their entrenched market position and high ROIC suggest they will forcefully hold the cash flows they have already secured.

Stated simply: The downside risk at these valuation levels appears heavily capped, insulated by the very quality and value metrics outlined above. This asymmetric risk/reward ratio is exactly how Buffett engineers his portfolio.

While SIRI currently represents a very small, calculated bet within Berkshire"s broader holdings, if the management team successfully modernizes its subscription model and unlocks advertising revenue, the upside potential from a 7.9x multiple is tremendous.