Watch Private Credit… Not Software

- Some (retail) investors expect stock-market liquidity from fundamentally illiquid private credit assets.

- Lack of price discovery allows managers to ignore losses until redemptions force liquidations

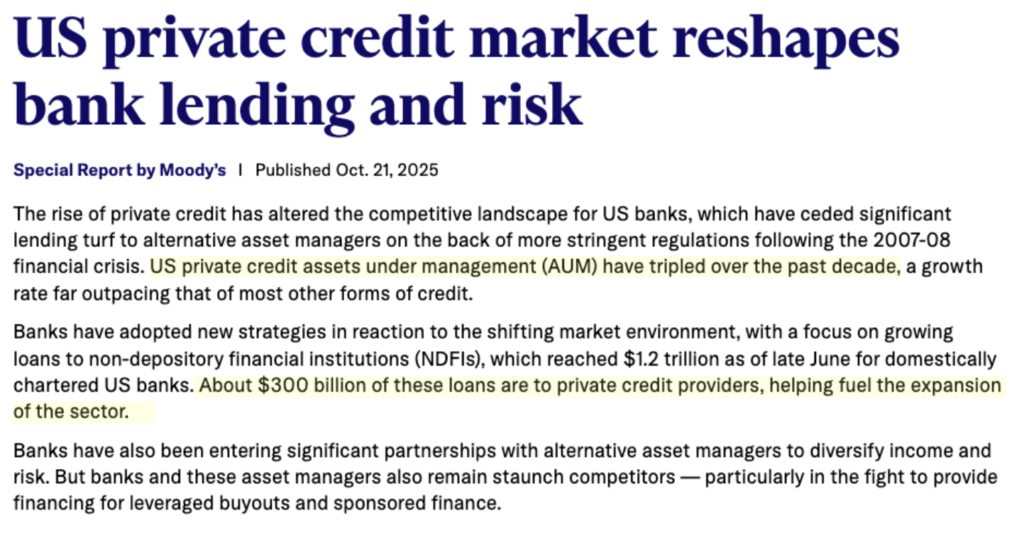

- Up to $300B in bank loans to private funds creates hidden contagion risk

Earlier this week I talked about the startling price adjustment in software stocks.

Highly profitable names like Adobe (ADBE), ServiceNow (NOW) ;and Salesforce(CRM) have lost more than half their value (from their highs).

And I highly doubt we have found the bottom…

For example, Salesforce (CRM) handily beat on the top and bottom lines in their most recent report – but it wasn"t enough to sell the stock lower by another 6%.

At the time of writing, the stock is down from its $367 January 2025 high to trade around $181.

Beyond software, there is another quiet correction working its way through the market.

The difference is this one matters more. I"m talking about the credit market.

Now if software stocks such as ADBE, CRM, NOW etc lose "half" their market value, the economy will do just fine.

Yes, some investors might cry poor – as they regret paying excessive 30x plus multiples for earnings – but the economy"s engine will keep running.

However, if the financial sector starts to restrict lending due to higher than expected defaults, the economy suffers.

Cracks in Private Credit?

One chart I"m watching this year is the financial sector ETF XLF

Over the past few weeks, the popular ETF is ~10% off its January high – trading back below highs of 15 months ago.

While major lenders remain in good shape – there is trouble brewing in the private credit markets.

For years, private credit stepped into the higher-risk lending vacuum left by regulated banks after 2008.

It looked like a win-win: investors got higher rates, and (riskier) companies got flexible cash.

But there is a fundamental difference: price discovery.

In a public market, a loan"s value is judged every day. It"s transparent. However, in private credit, it"s often the fund manager who decides on its value.

And today – those values are being tested.

The "Blue Owl" Stress Test

Over the past 10+ years, the private credit market has surged to approximately $1.8 trillion.

For perspective, the outstanding volume of subprime mortgage-backed securities in 2007 was roughly $1.3 trillion.

While today"s global financial system is larger, the private credit market is now 50% larger than the subprime market was at its peak.

However, the mechanics are very different…

The reason this setup is explosive is something known as the "leverage loop."

The headline risk is not that nonbank lenders make loans to middle-market companies. It is the funding chain behind those loans.

The leverage loop is the mechanism:

Private credit funds extend loans, then borrow from banks against those loans, often on terms with favorable capital treatment.

The same dollar of borrower risk is thus financed by a bank, but in a form the bank can count as lower risk weight. Safer on paper is not safer in reality.

It is leverage layered on leverage.

When assets are marked infrequently and cash flows are floating rate, this works — until it doesn"t.

The engineering metaphor is a truss:

Redistribute load across more beams and you reduce visible strain, right up to the moment a hidden joint fails.

Now in 2007, banks used "shadow" entities to hide subprime loans; when those loans failed, the banks were forced to bring the losses back onto their balance sheets, causing a capital wipeout.

Today, there are some parallels.

According to Moody"s – regulated banks have lent roughly $300 billion directly to private credit funds.

This creates a bridge for "shadow" risk to cross back into the regulated banking system. If the private funds default, those "safe" bank loans become the next domino.

For clarity, the $300B in bank loans are typically senior-secured credit facilities.

On paper, the bank is the first to be paid.

But in a liquidity crunch, seniority is a cold comfort if the underlying assets are marked at 70 cents and there is no exit.

Now it would be a mistake to start thinking this is "Subprime 2.0″.

It"s not.

Banks hold far more capital. Households have more fixed-rate debt and are in good shape.

But the system has rebuilt complexity in a new corridor.

For example, before the 2008 financial crisis, risk was distributed through CDOs and off-balance-sheet conduits.

Today, risk is tranched by contract and distributed through non-banks, then partially pulled back onto bank balance sheets via the leverage loop and credit facilities.

In other words, whilst the mechanism is different – the principle is the same.

Credit risk is conserved. When it is transformed to please capital rules or investors, it tends to concentrate.

In construction terms, we have knocked out load-bearing walls to create an open floor plan.

It looks spacious but it"s less forgiving in an earthquake. The echoes of 2008 are not about assets – they are about architecture.

Mark-to-Myth

In the lead-up to 2008, subprime bonds were "mark-to-model" (not market)

There is just one problem… what"s in the model?

For example, when the 2008 mark-to-model was stress tested – where the ABX Index allowed the market to bet against them – we found that "par value" was a lot lower.

Today, private credit is having its mark-to-model moment due to the lack of public price discovery.

Or as Charlie Munger would call it… "mark-to-model" is more accurately "mark-to-myth"

Activist Boaz Weinstein is now applying it"s own stress test.

By launching tender offers for stakes in Blue Owl-managed vehicles at roughly 70 cents on the dollar, they challenged the "liquidity story" alternative managers have sold to retail investors.

If a fund marks an asset at $1.00 but a sophisticated buyer offers $0.70 and finds willing sellers, the official valuation is a fiction.

In other words, these "semi-liquid" funds promised liquidity that doesn"t exist in the underlying loans.

Now every credit bubble needs a catalyst to pop:

- In 2007, it was falling housing prices that prevented "NINJA" borrowers from refinancing; and

- In 2026, the catalyst looks increasingly like AI Disruption.

For example, UBS analysts recently issued a grim warning:

If AI triggers aggressive disruption among corporate borrowers, default rates in private credit could surge as high as 15%.

Direct lenders who aggressively financed software companies now look over-exposed.

We are already seeing signs of strain, with "interest paid-in-kind" (borrowing more just to pay existing interest) nearing post-pandemic highs.

Part of me can"t help but think its the 1999 tech bubble meeting the 2007 credit bubble.

Today companies borrowed heavily to invest in unproven AI business models.

Now if those investments don"t generate the expected (very large) cash flows within the next 12 to 24 months – the market will question whether they can service the (excessive) debt.

That"s the worry…

Parallels to 2006/07…

Jamie Dimon (CEO of JP Morgan) has been warning about what he sees in private credit markets for some time.

In this article – his comparison to 2008 isn"t hyperbole.

He is warning about private credit filling the "vacuum" of loans to riskier businesses (echoing the Moody"s article I referenced earlier).

In any industry, when there is too much cash chasing too few good ideas, the standards for quality inevitably drop.

Twenty years ago it was "No Income, No Job, or Assets" (NINJA) loans which brought down the financial sector.

More recently – it"s "Covenant-Lite" private loans.

These are deals where the lender has almost no power to step in if the borrower starts failing.

Why would a lender agree to this?

Because if they don"t, the borrower will simply go to the fund across the street.

When the fee-gathering incentive of the fund manager outweighs the "risk-management" duty to the investor – losses are just a function of time.

Putting it All Together

When software giants such as (not limited to) ServiceNow, Salesforce and Adobe lose more than half their value – it captures headlines.

But the real systemic risk isn"t in what we can price — it"s in what we can"t.

As Jamie Dimon warned, the parallels to 2008 aren"t in the assets (mortgages), but in the architecture (e.g., the Leverage Loop).

If we invert this situation, we shouldn"t ask if private credit is "good," but rather: what are the specific joints that could cause the truss to snap?

For example:

- If a fund marks its assets at 100% of value but investors can only exit via a 70% tender offer, what is the real equity value of that fund? and

- When does a bank"s "low-risk" senior loan to a private fund become a high-risk exposure to a failing AI startup?

From here, I will be watching if any private credit funds move to freezing redemptions.

For example, when "semi-liquid" retail funds (like Blue Owl) move from restricting redemptions to freezing them entirely – the pressure will move to the stock market.

But let me clear – this is still very early.

It"s unlikely markets are about to crash anytime soon.

However, if AI disruption eats into the cash flows of the software sector faster than these companies can service their "covenant-lite" debt, the forecast 15% default rate that UBS predicts — will make the sell-off in software appear mild.