Consumption Tax: Why the Market is Mispricing Trade Deals

Words: 1,997 Time: 8 Minutes

- I don"t see how these tariffs end well

- Back of the envelope math on the tax to be paid

- S&P 500 remains overly complacent

Over the past week I was watching how Trump"s trade deals would land ahead of the August 1 (30%) deadline.

From mine, the best case scenario was a blended tariff rate of ~10% (as this was the "great" deal the UK secured).

As it turns out, that blended rate is more likely to be closer to 18%.

But time will tell… with China still in the balance.

For example, with respect to Japan, Trump secured a 15% tariff rate. From CNN:

"I just signed the largest trade deal in history; I think maybe the largest deal in history with Japan,"

Trump said during a reception with Republican members of Congress Tuesday night. "They had their top people here, and we worked on it long and hard. And it"s a great deal for everybody."

The deal will see US importers pay 15% "reciprocal" tariffs on Japanese goods exported to the United States.

But importantly for Japan, the 15% rate will also extend to automobiles and car parts – putting it at an advantage over other major vehicle exporters, which have faced a 25% levy on automotive sector exports since April.

Japan will also invest $550 billion dollars into the United States, Trump said, adding that the US "will receive 90% of the profits.

Over the weekend, Trump announced his 15% deal with the European Union (EU). From the Guardian:

Under the agreement, the US will levy a 15% baseline tariff for most EU exports to the US, limiting a higher tariff. However, the rate is higher than before Trump came to power, and a 50% tariff remains on steel exports – a setback for that industry.

Trump has also said he expects a blanket 15% to 20% global tariff on countries who are yet to secure a deal.

And with respect to China – tariffs continue at a whopping 30%.

But here"s the thing:

Coming into 2025 – the economy worked with a blended 2.7% global tariff rate on US imports.

And despite the market "cheering" the 15% deals with Europe and Japan (where other deals are likely to land in the realm of 15% to 20%) – that is ~12.3% more than what was in place.

Yes, we have some certainty – which is always welcome. Markets like this.

But by any measure – an incremental 12.3% in tariffs (or more) – will be a disaster for the global economy in the long-run.

Let"s unpack why I think there is nothing to cheer… despite the record highs in markets.

~$500B in New Taxes Coming Your Way

It"s hard for me to understand why the market is so happy about the terms of these new deals.

Let"s start with the new tax Trump is making US consumers (and companies) pay.

Last year the US collected about $88B in tariff revenues at a blended global rate of 2.7% on total imports of ~$3.3 Trillion.

If we assume the new tariff rate will increase to around 18% (as a blended rate) – that comes to a figure of almost $600B

$3.3 Trillion x 18% is $594B

Put another way – there could be up to ~$500B in new "consumption taxes" that need to be paid on these imported goods.

But….

We should also assume the volume of goods imported will fall.

Econ 101 tells what when you increase the price of something – then expect less of it.

If we assume import volumes drop 10% (a conservative figure over the next 12 months – but more accurate over a longer period) – the dollar impact is closer to $450B (vs $500B if the volume didn"t fall year over year)

The only question is who is going to pay the new $450B consumption tax?

This is something I explored here…

The other vector we need to think more about is how much inflation will come as a result of the ~18% tariff?

We know that some goods will rise in price… but how much?

It"s my expectation that in ~9 to 12 months – we will see Consumer Price Inflation move back above 4.00%

Again, we only need to look at the sharp increase in PPI which tells us that inflation is on its way.

But for now, the inflation impact is not showing up largely due to most companies drawing down on existing inventories.

However, the price of goods is slowly starting to increase…

It"s my view that every 1% increase in the tariff rate is worth about 10 basis points of inflation.

For example, let"s say we land at 18% blended tariff rate up from 2.7% (much of which will be a function of how things land with China)

That"s about a 15.3% increase in tariffs.

15.2% x 0.1% (10 basis points) = 1.53% increase in the inflation rate.

Today CPI is around 2.40%

If we then add a further 1.53% over the next 12 months – that brings us to 3.93% CPI.

So here"s a question:

Do you think the Fed will be comfortable cutting rates with CPI closer to 4.0% (vs their target of 2.0%)

Handcuffs on the Fed

This brings me to what matters most for the market:

- Interest rates (and monetary policy); and

- Availability of liquidity.

As we know, the Fed has a dual mandate: (i) price stability; and (ii) full employment.

With respect to the latter, the data we get from the labor market will be critical.

And this week we get another look at JOLTS (job openings) and non-farm payrolls.

It"s my view that job growth will continue to slow over the next 12 months as tariffs start take their toll (e.g., maybe as low as just 50K per month)

However, given we have to balance this with the large drop in immigration and increased deportations – unemployment is likely to stabilize around 4.3% (as the denominator effectively shrinks)

If that"s true – then there is no compelling need for the Fed to intervene with aggressive rate cuts.

For example, if they were to see this climb above 4.50% – you could argue the case for a cut.

But in terms of price stability – inflation is likely to reaccelerate as I outlined. And this has the Fed"s hands tied (as Powell has stressed in recent addresses)

That said, the market believes the Fed will cut at least twice (maybe up to four times) this year.

I"m less convinced…

But if that"s the case – it can only mean that economic growth is slowing despite higher inflation (i.e. stagflation)

That is a negative for markets.

However, let me be clear….

On any news of a Fed rate cut – equities will like it initially – as financial conditions remain quite loose – where liquidity is widely available.

That"s a recipe for higher stock prices.

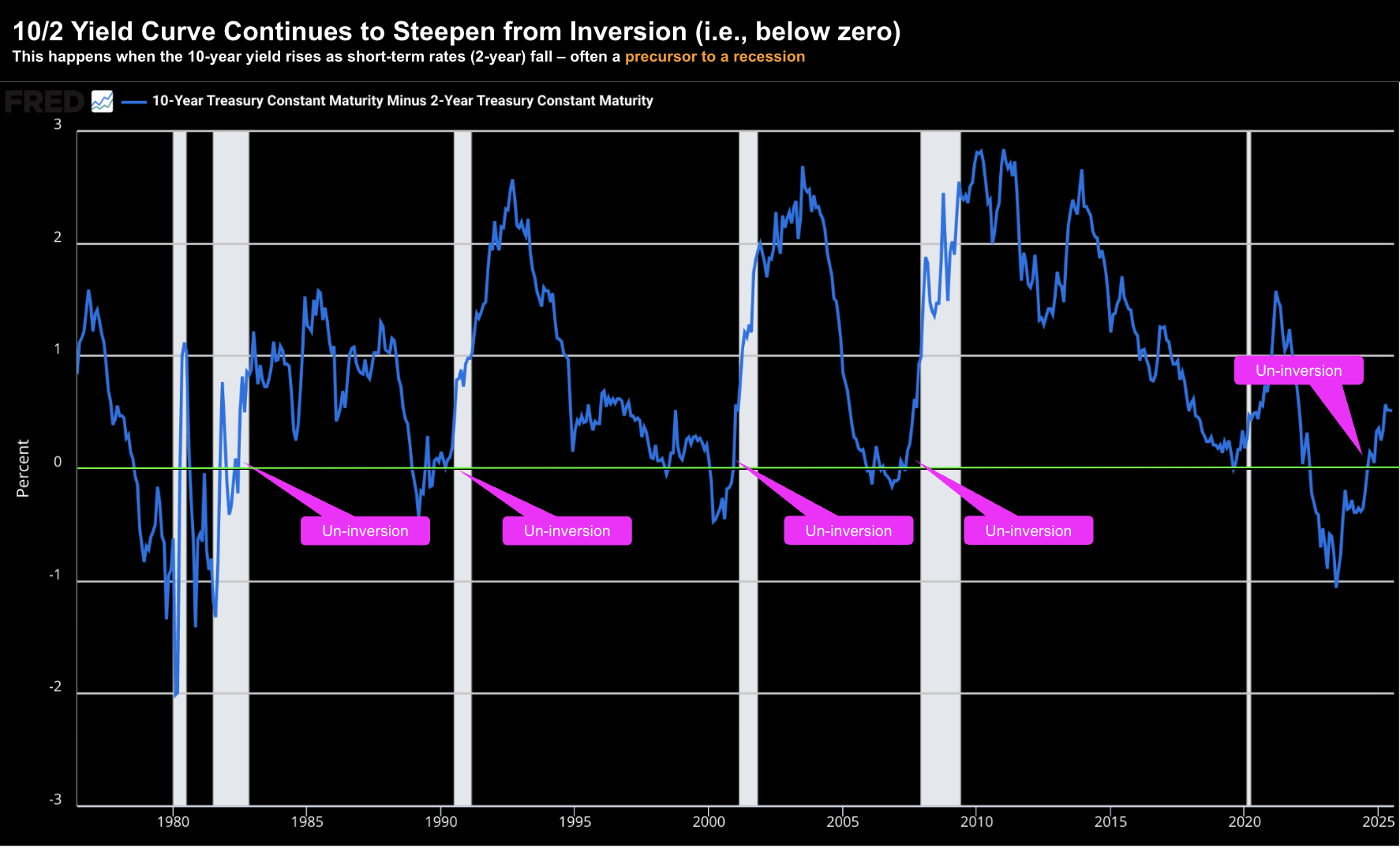

However, from the bond market"s perspective, running a 6% deficit with inflation going up is not a good story.

This will see the long-end of the curve rise (as the Fed manipulates the short-end)

And if this proves to be the case, that could see the yield curve steepen further… often a strong precursor to a recession (as this 50 year chart shows):

I often say it"s not the yield curve inverting which is the issue. Stock markets will generally continue to rise with a deeply inverted curve.

It"s the re-steeping and un-inversion of the curve which is troubling.

More often than not – it indicates a recession is not too far away. However, precise timing is very difficult to predict.

As an aside, with the 10-year yield likely to rise and the government running a debt balance of $36 Trillion – every 1% increase in the 10-year is ~$360B in interest charges (nb: expect the government to try and raise money at the shorter-end).

Therefore, I think the Fed will need to be very diligent in controlling inflation.

Trump"s tariffs will not be helpful with this objective.

And as much as the President wants lower rates (despite the obvious risks) – Powell needs to stay resolute on achieving the Fed"s dual mandate (and its independence).

S&P 500: Are You OK?

Last week I watched the 2024 documentary "Freediver" – Alexey Molchanov"s daring attempt to set multiple freediving world records in 2023.

It"s a sport I don"t fully understand (why do it?) – but the documentary is worth a look.

Alexy can free dive ~136 meters without any breathing apparatus or flippers. He holds his breath for around 4 minutes and 30 seconds to achieve this (he can do ~150m when enabled with flippers).

But holding your breath is only half of it… it"s also the incredible pressure he puts on his (vital) organs.

Regardless, for Alexy to complete a world record, simply free diving to 150m and then resurfacing alive is not enough.

For example, to achieve a pass, he needs to first remove his nose plug; give a signal with his fingers of "ok""; and then verbally say "I"m okay" to get a pass. And it must be in this sequence.

If he messes up the sequence on resurfacing (e.g., he says "I"m ok" first without signaling) – the dive would be recorded as a fail.

In one attempt – he achieved a new record depth of around ~150m – but got the "I"m OK" sequence wrong when he surfaced. The world record was considered a fail. Heartbreak.

Which brings me to the market….

From mine, the Index not only needs to make a new high – like our free diver – it needs to signal "I"m ok" to get a pass.

For me, that signal is 4% above the previous high of 6147 (i.e., a level of 6400) and held for a few weeks.

At that point, I would say we are likely to break out to the upside.

July 28 2025

At the time of writing, the S&P 500 is pushing the level of 6400

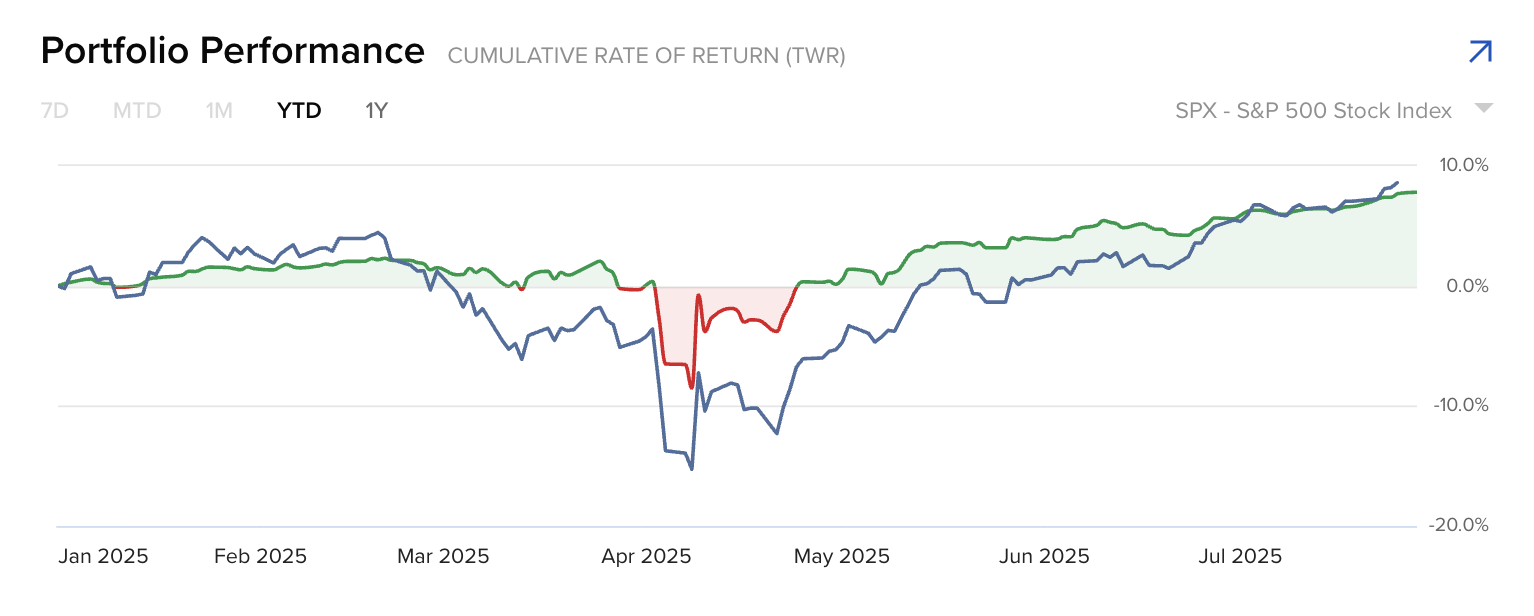

To add further context – in the 17 weeks since the ~4800 April lows – it"s rallied some 32%.

This has the market up ~8.5% year-to-date.

Hopefully you maintained some long exposure to quality names – perhaps capitalizing during the April lows.

For example, the so-called Mag-7 is responsible for more than 50% of the total S&P 500 gains.

Below is my own fund"s performance (in green) year-to-date – matching that of the S&P 500 (blue)

July 28 2025

That said, at this point I"m very wary.

Valuations are exceptionally rich – despite the earnings story holding up.

This week we will hear from the likes of AMZN, AAPL, MSFT, META and a host of others.

It"s a big week in terms of how corporate America is managing the tariffs.

Expectations are high… however any disappointment could see the market correct to the tune of 10% or more.

Putting It All Together

The market is happy cheering the "better than feared" trade deals with the likes of Europe and Japan.

Yes, 15% is better than 30%. Sure.

But 30% would be an embargo – not a tariff.

15% will not be good for global trade or growth.

In my view it will slow economic growth; decrease overall consumption; and result in less job creation (due to weaker demand).

Here"s a post (from Dec 2024) I penned on why tariffs is terrible idea.

Trump"s tariffs will be at least ~12% more than what we had at the beginning of the year.

This consumption tax will need to be paid by someone… just a question of who.

Those with pricing power (such as Apple) will likely pass on most of the cost increase to consumers. And those who don"t will need to absorb the impact to net margins. Either way someone is paying.

For now, the market believes 15% tariffs are good news – pushing prices to record highs.

I doubt this will be the case in 12 months.

Make sure you take a few chips (not all) off the table here – don"t give back all these fabulous (fast) gains.