The AI Red Queen Race: Why Massive Capex and Market Cycles Signal a Rotation to Value

The AI Red Queen Race: Why Massive Capex and Market Cycles Signal a Rotation to Value

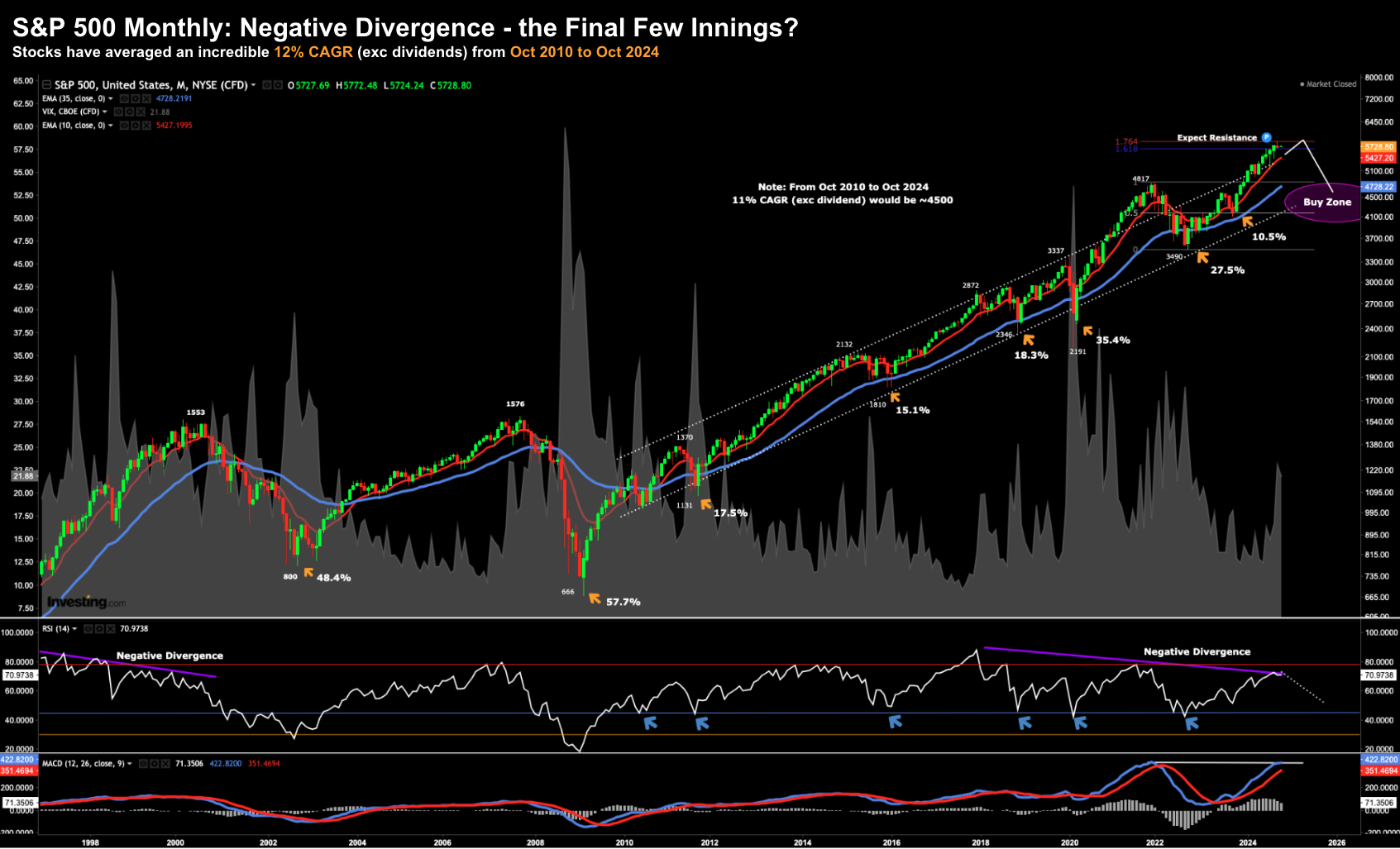

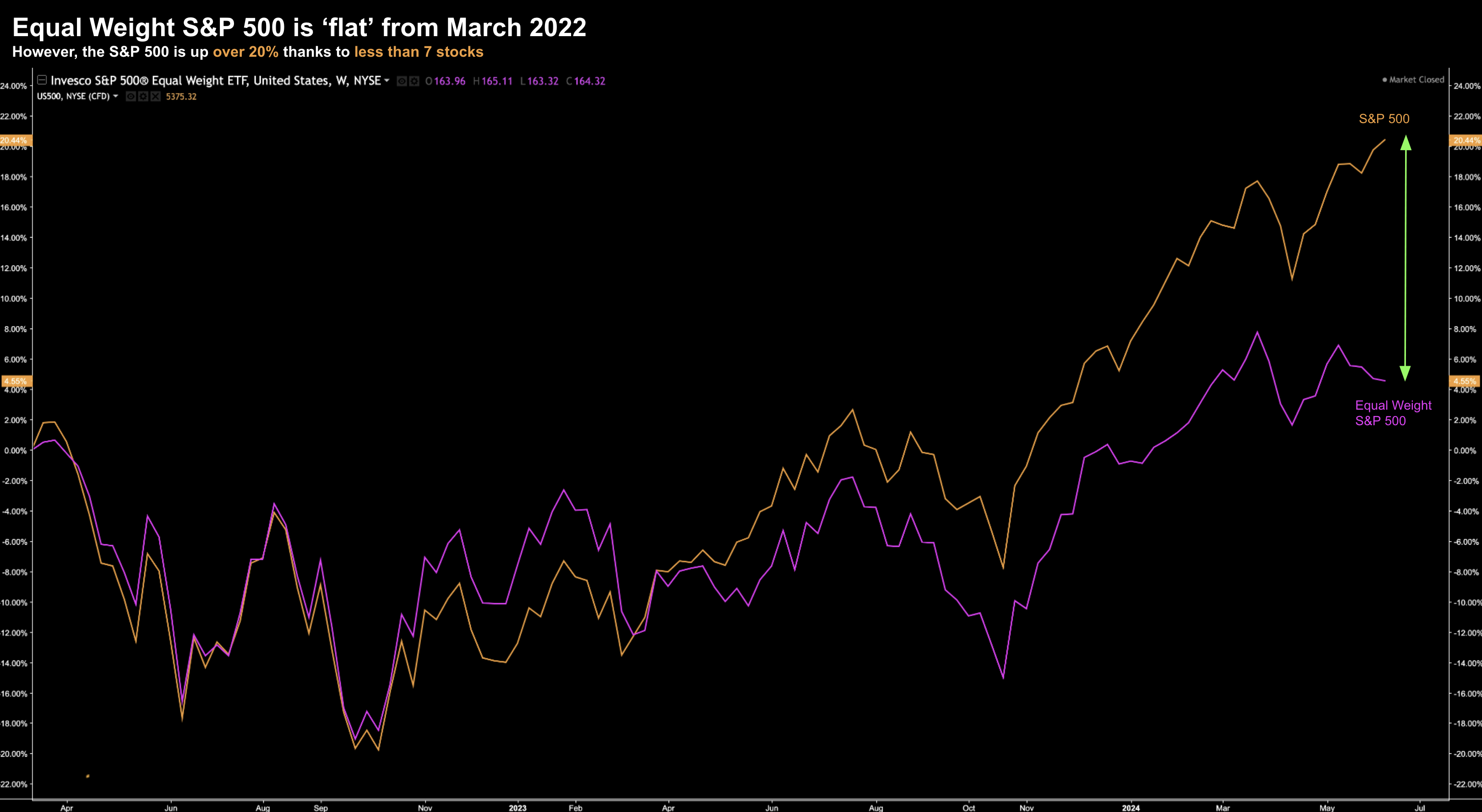

From an index perspective, it has been a lackluster start to the year. At the time of writing, markets have made very little ground over the first 6 weeks. The good news – it”s still early. However, given the incredible…