The Bond Vigilante Vote: Why 5% Yields and a $4 Trillion Deficit Could Break the S&P 500

The Bond Vigilante Vote: Why 5% Yields and a $4 Trillion Deficit Could Break the S&P 500

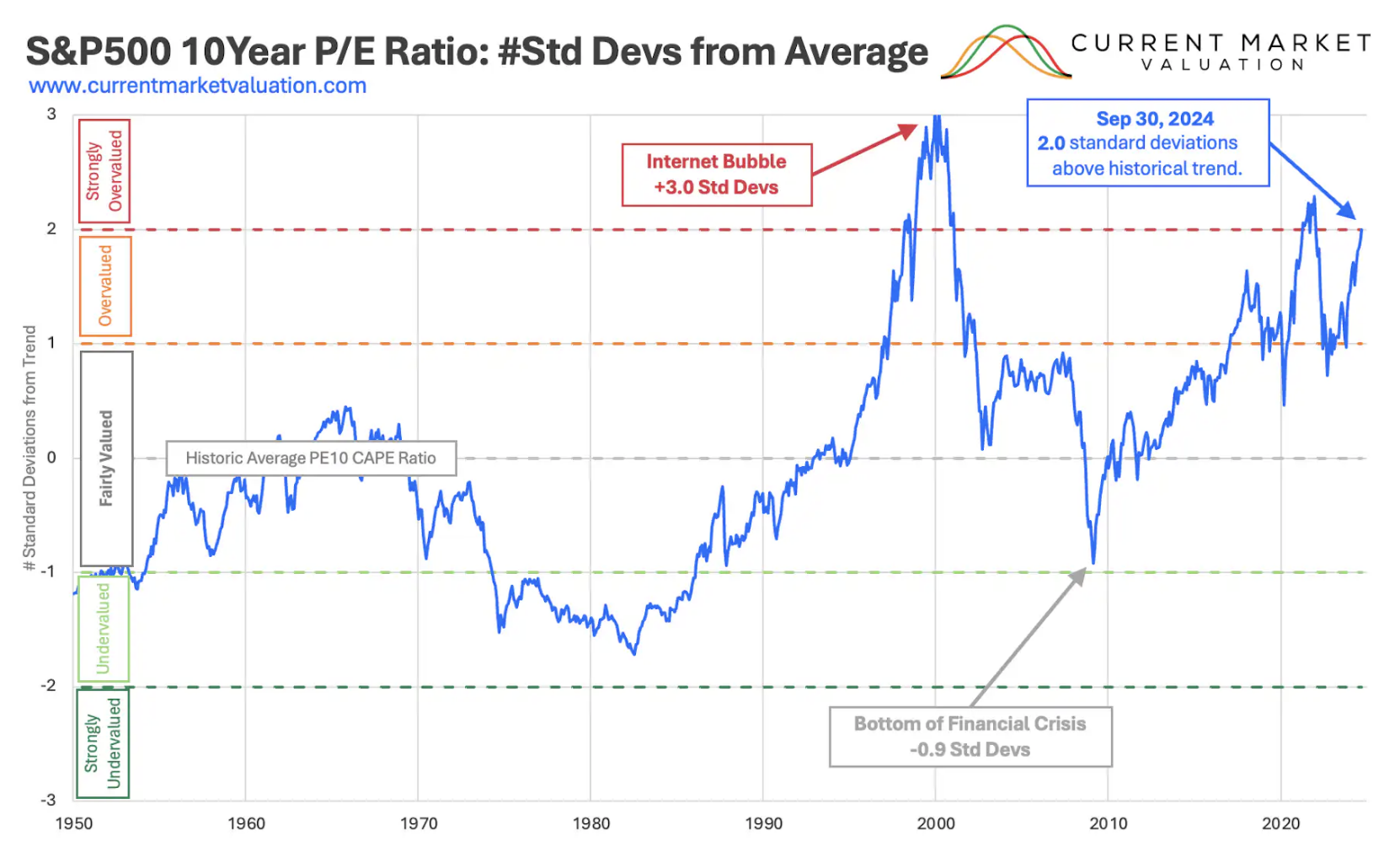

Markets paused to take a breath this week following a six-week ~22% surge. The S&P 500 surrendered a routine ~2.80% - after touching a 12-week high of 5,968. With the market trading at 22x fwd earnings (a premium in any environment) - investors are arguably more mindful of (a) ongoing tariff risks- with new threats from Trump on Europe and Apple; and (b) the thread of rising bond yields - and any potentially widening of the deficit.