Red Sweep Turbocharges the Market

Red Sweep Turbocharges the Market

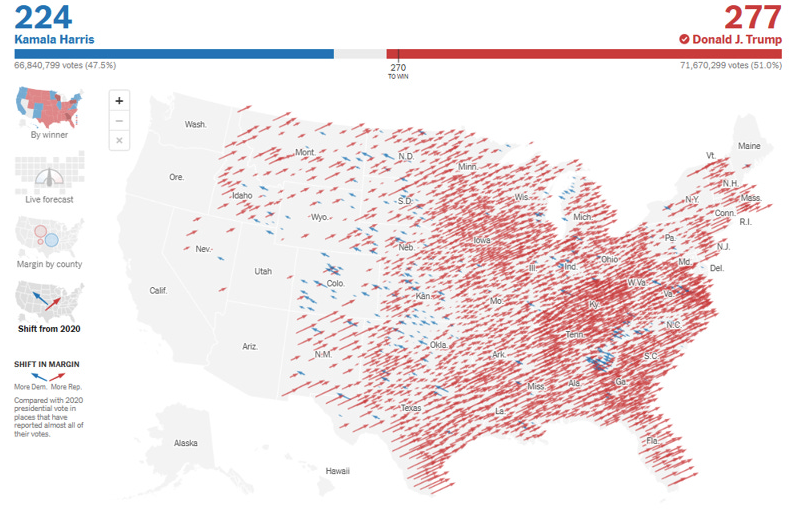

Trump's decisive win last week has seen significant shifts in market sentiment. Markets are optimistic that Trump's tax cuts and deregulation will turbocharge growth. And they might. But what implications will Trump's policies mean for the US dollar, long-term bond yields and foreign trade? As investors, you need to evaluate both what is seen vs unseen. There will be both opportunities and challenges... however they will be very sector specific.