Here’s What We Still Need to See

Here’s What We Still Need to See

There are three primary things we still need to see before we can confidently claim we are close to a market bottom in 2022... the first is a pivot from the Fed.

Here’s What We Still Need to SeeThere are three primary things we still need to see before we can confidently claim we are close to a market bottom in 2022... the first is a pivot from the Fed.

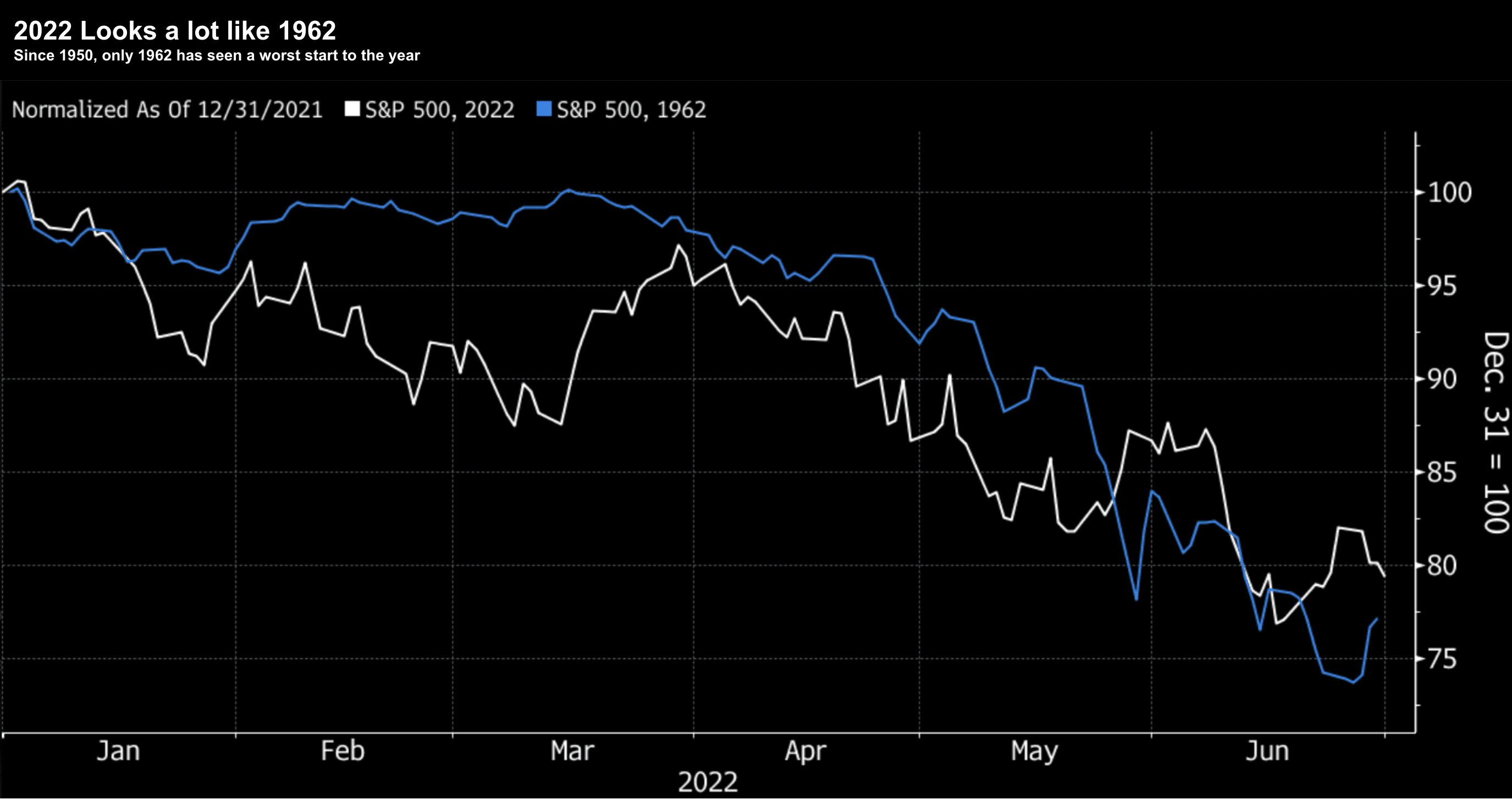

Worst 6-Months to Start a Year Since 1970

Worst 6-Months to Start a Year Since 1970It's becoming increasingly likely we will see a recession next year (maybe before). And there's one thing that every recession has in common post 1950 -- aggressive Fed tightening into a slowing economy.

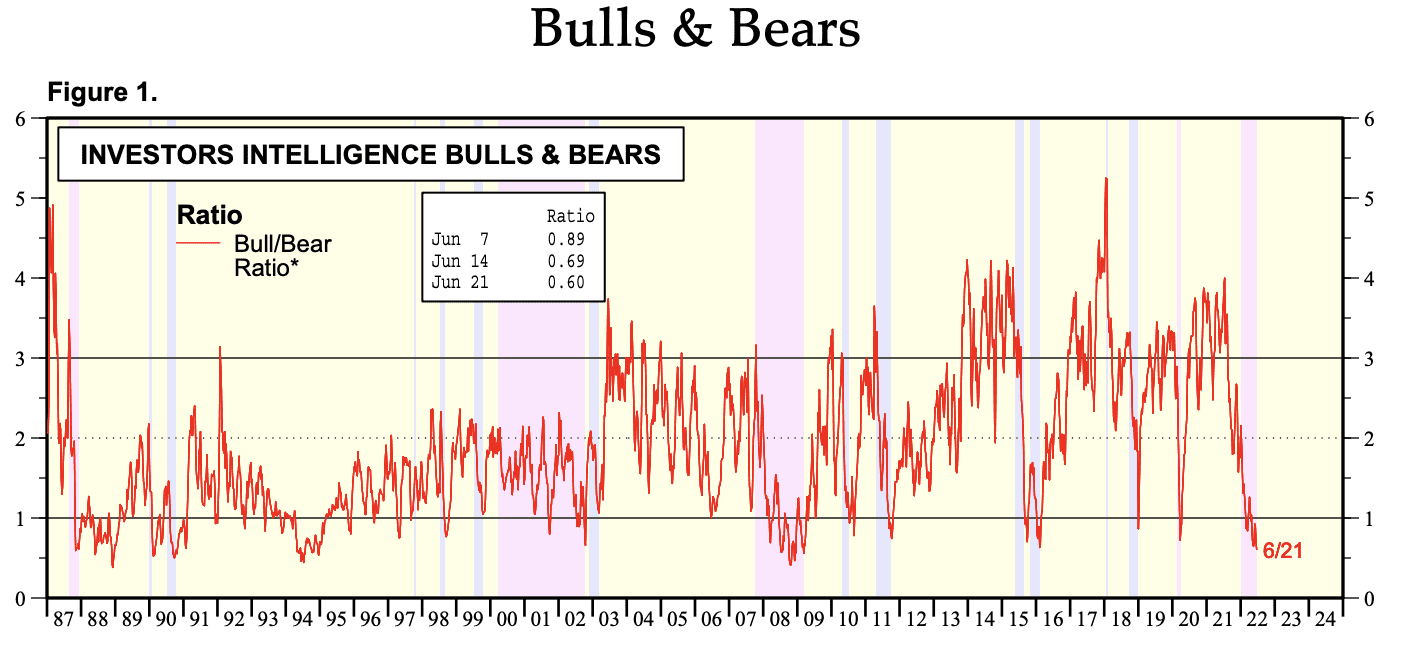

Why Markets Crash; and Why It Spells Opportunity

Why Markets Crash; and Why It Spells OpportunityWhy do markets crash? And how do you identify the likelihood of downside risk before it happens? And when it happens - how do you know when to get back in?

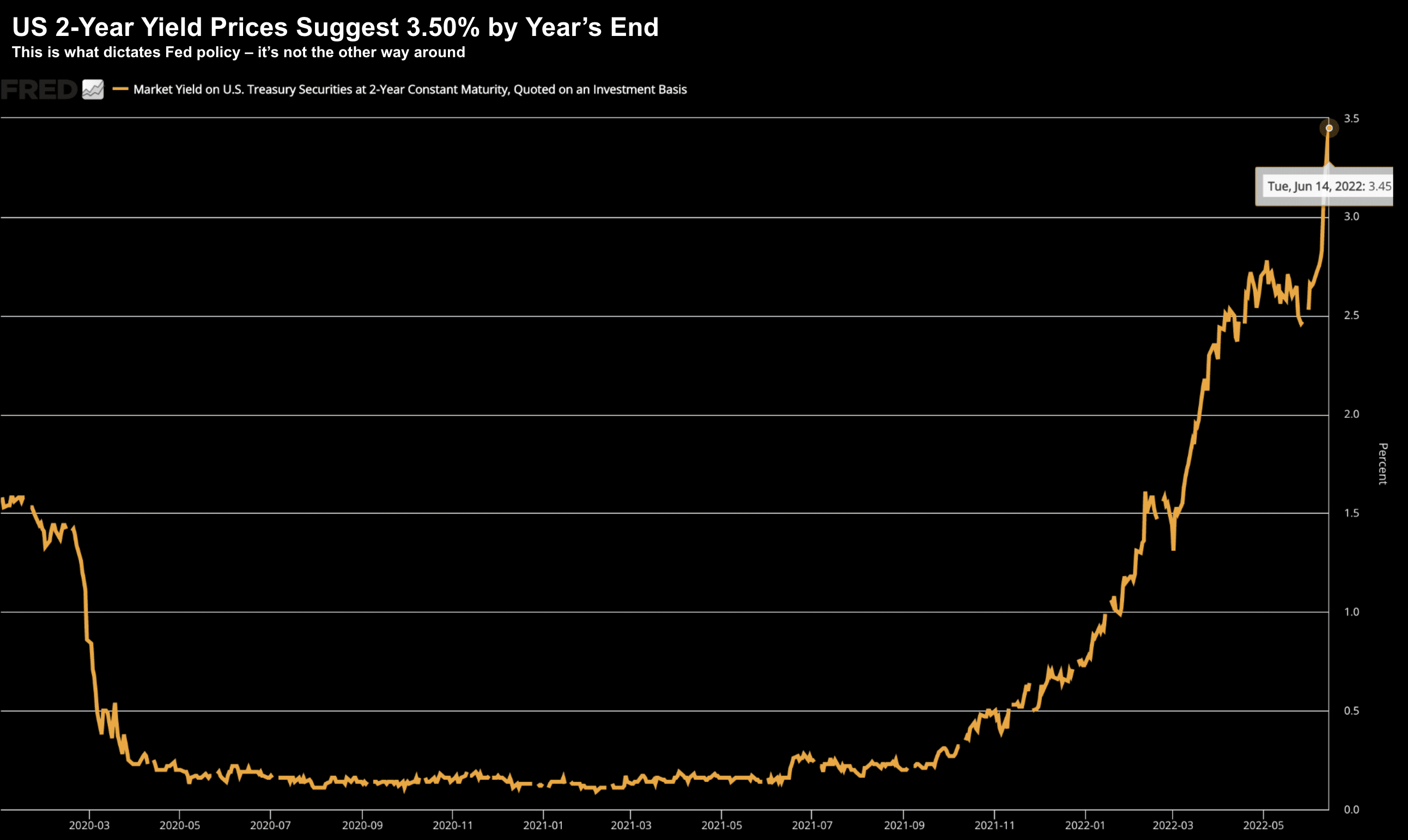

Fed Hints at ~3.50% by Year’s End

Fed Hints at ~3.50% by Year’s EndFor the first time since '94 - the Fed raised rates by 75 basis points. You can lock in 75 bps for July. However, they will need to do a lot more to tame unwanted inflation.

The Bear Roars… Markets Price in 75 bps Hike

The Bear Roars… Markets Price in 75 bps HikeWhen it comes to the market - there are (a) times to make money; and (b) times not to lose money. Now is the time for the latter... the past decade was the time for the former.

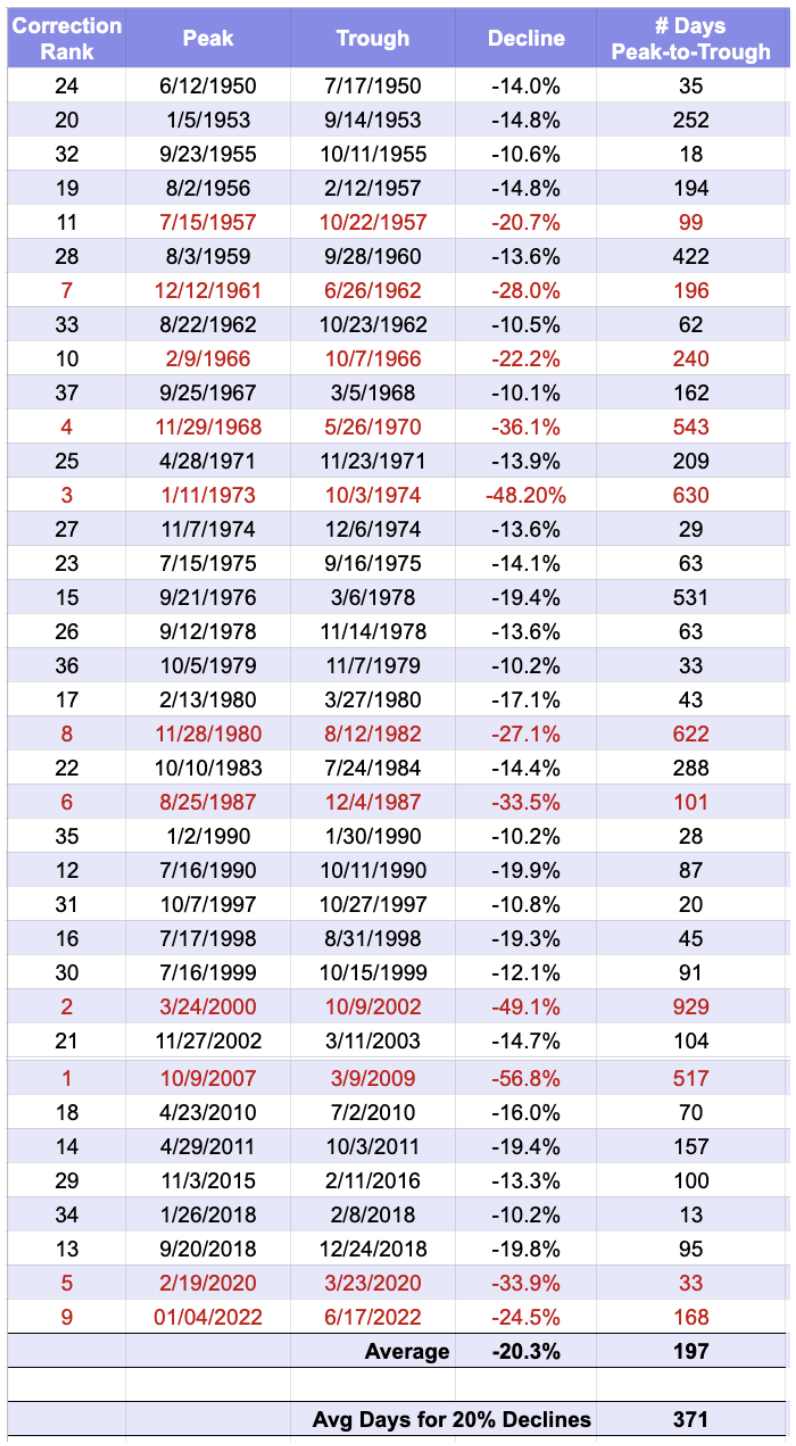

We Haven’t Seen the Lows for 2022

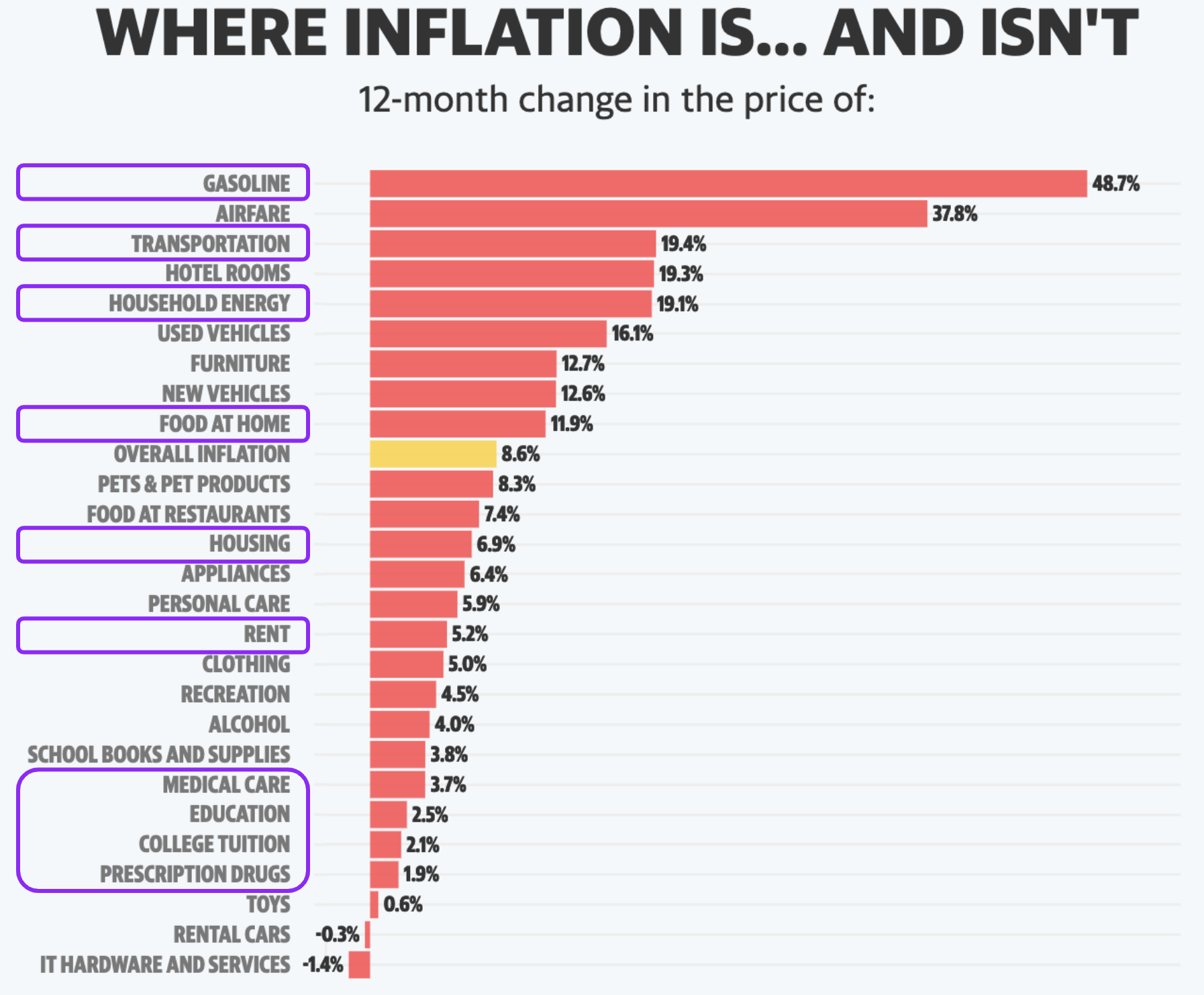

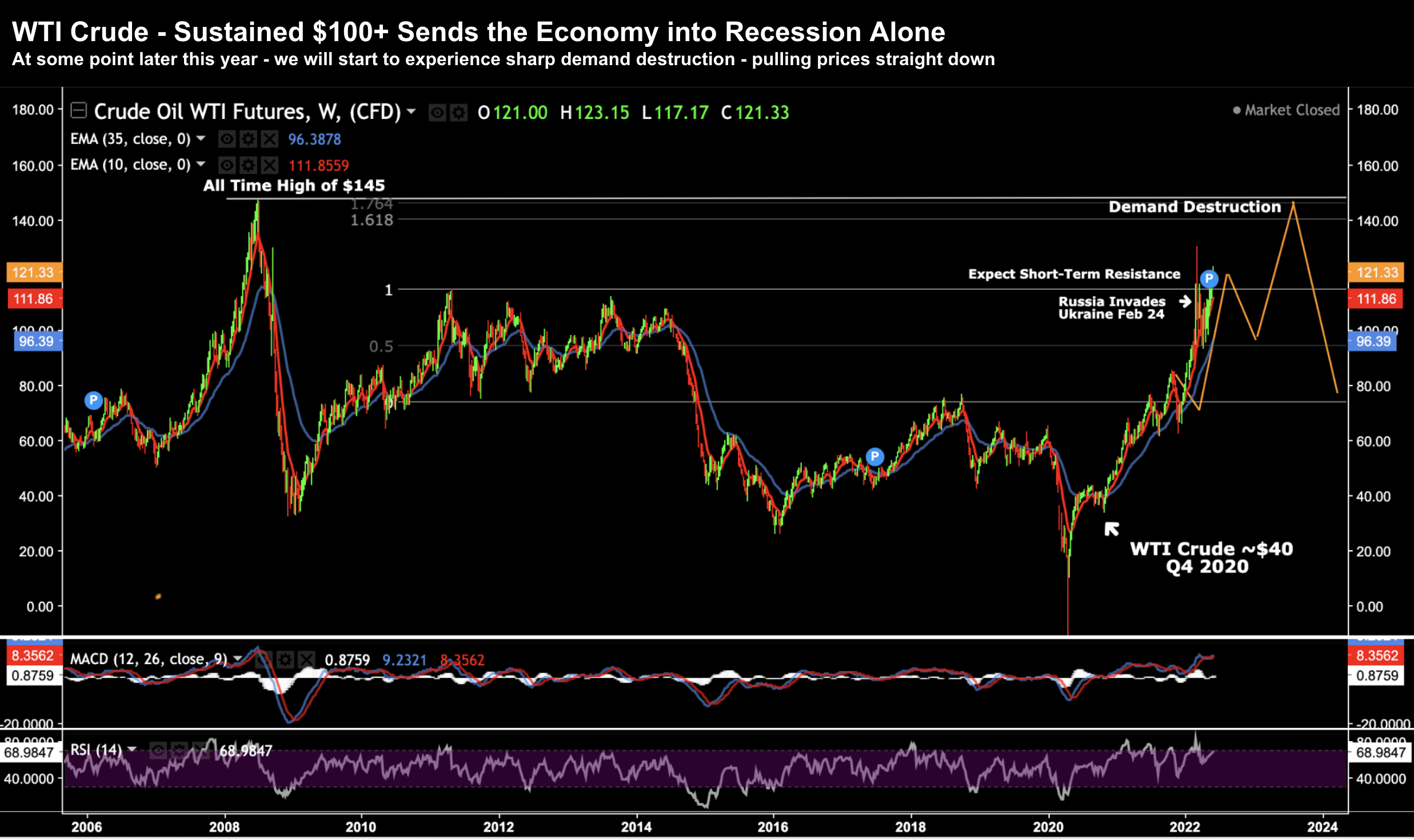

We Haven’t Seen the Lows for 2022Consumer Price Inflation (CPI) continues to run at a 41-year high 8.6%. It's not hard to explain - look no further than monetary and fiscal policy. From mine, the Fed has no choice but to remain very aggressive - where a 75 basis point raise is not off the table. This is not conducive for higher stock market prices in the near-term

Don’t Be Fooled…

Don’t Be Fooled…CPI for May is expected to come in at a red-hot 8.2%. Anything north of 8% will not change the Fed's aggressive stance. In short, inflation is not likely to go away soon... look no further than energy and food prices. Here's why the Fed will hike straight into a recession.

A Cautious Market – MSFT & TSLA Warn

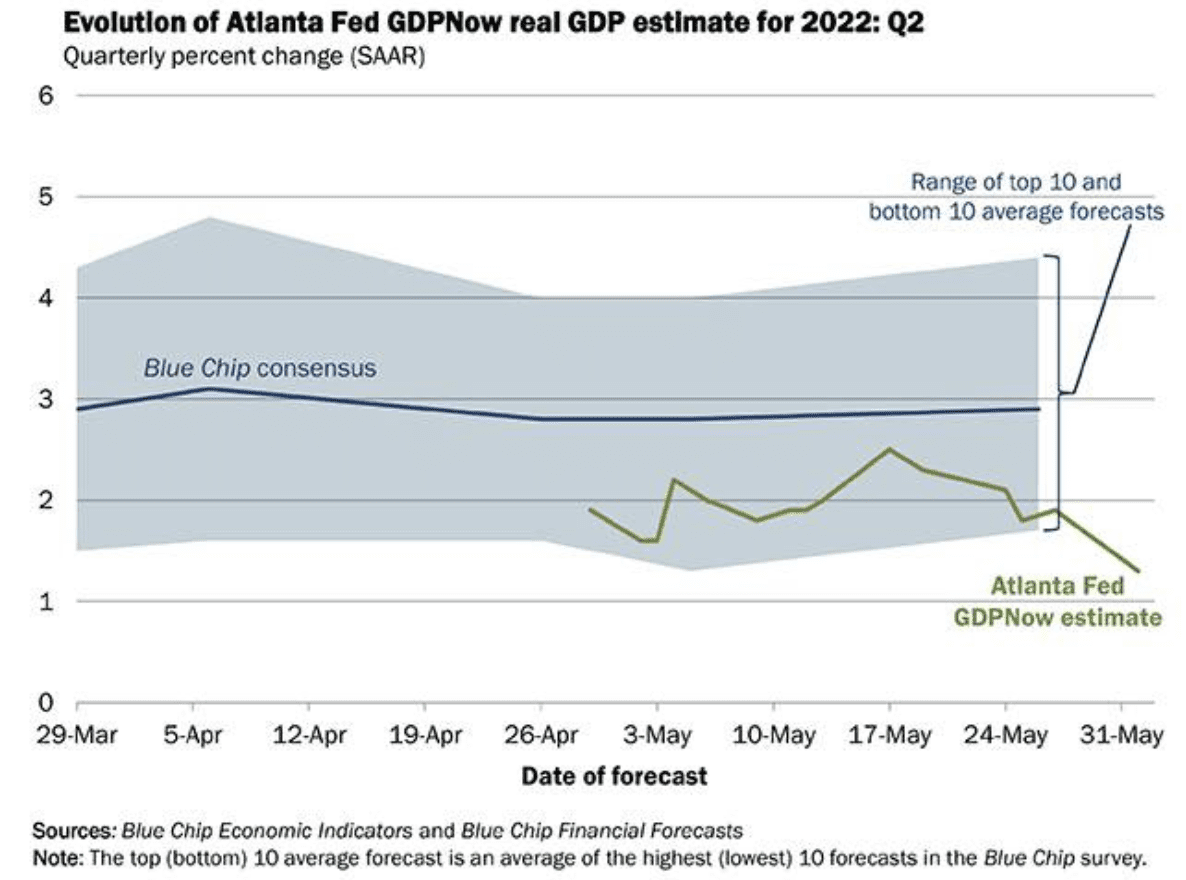

A Cautious Market – MSFT & TSLA WarnLeading CEO's are warning of storm clouds ahead. However, recent economic data suggests near-term recession fears are over-blown. Are the Fed hiking too far too fast?

Time to Lengthen Your Time Horizons

Time to Lengthen Your Time HorizonsJamie Dimon - CEO of JPMorgan Chase -told the market to brace for an economic hurricane. There's weight to his comment - however it will be a great long-term buying opportunity if correct.

The Risk/Reward for Equities

The Risk/Reward for EquitiesWhat's the risk/reward equation for equities? My view - the downside risks still outweigh the upside opposite a host of reasons. Let's explore...