Inflation Analysis: Identifying Peaks and Policy Lags

Inflation Analysis: Identifying Peaks and Policy Lags

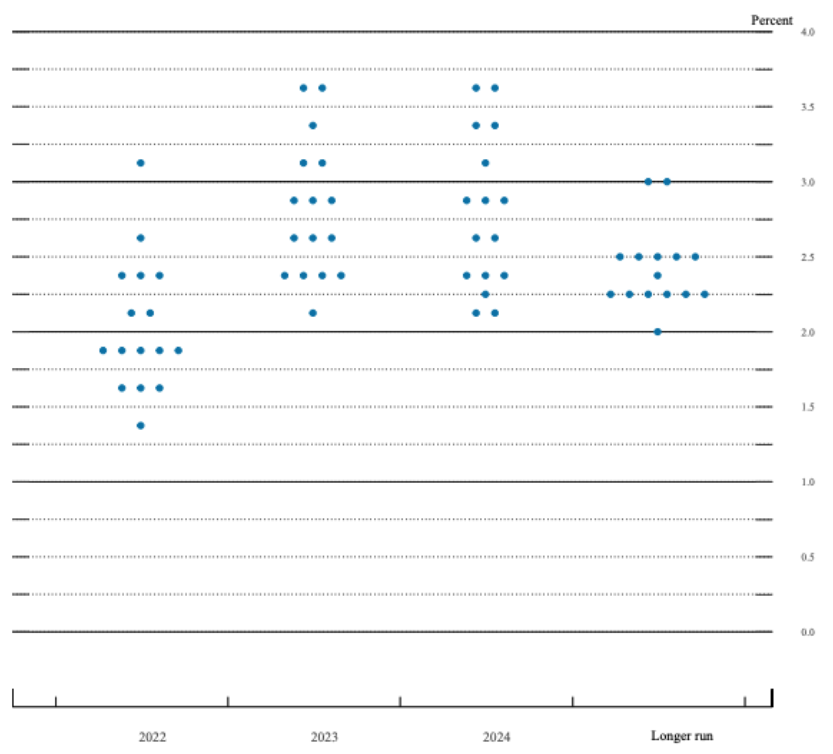

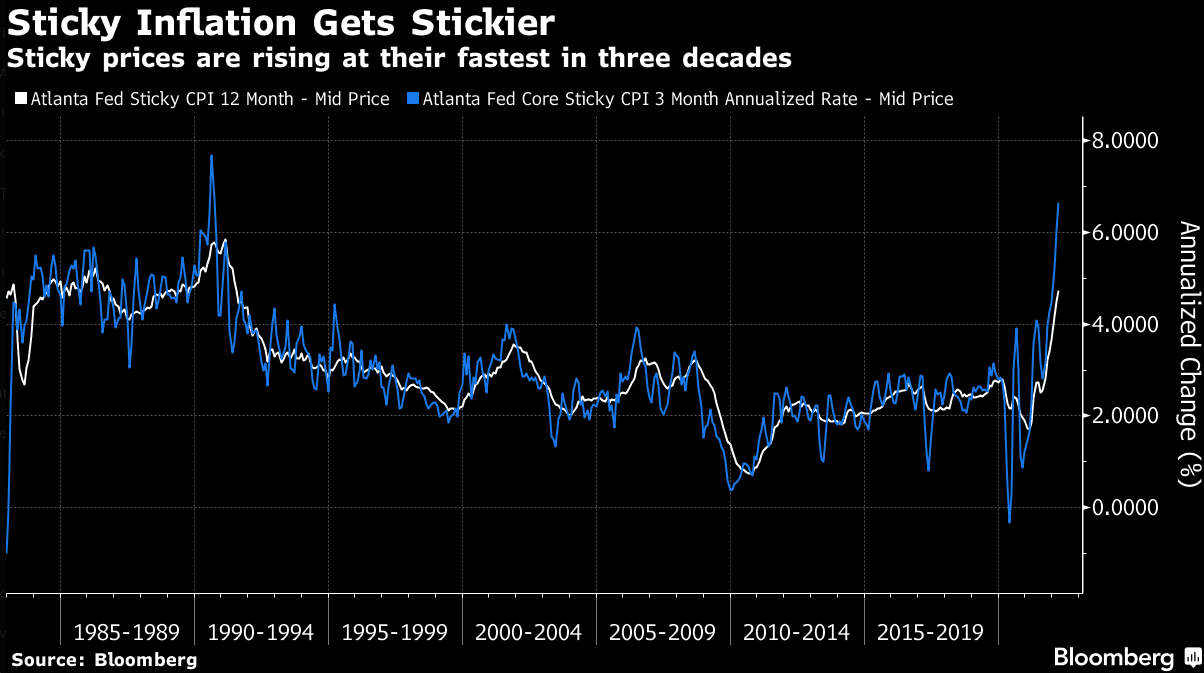

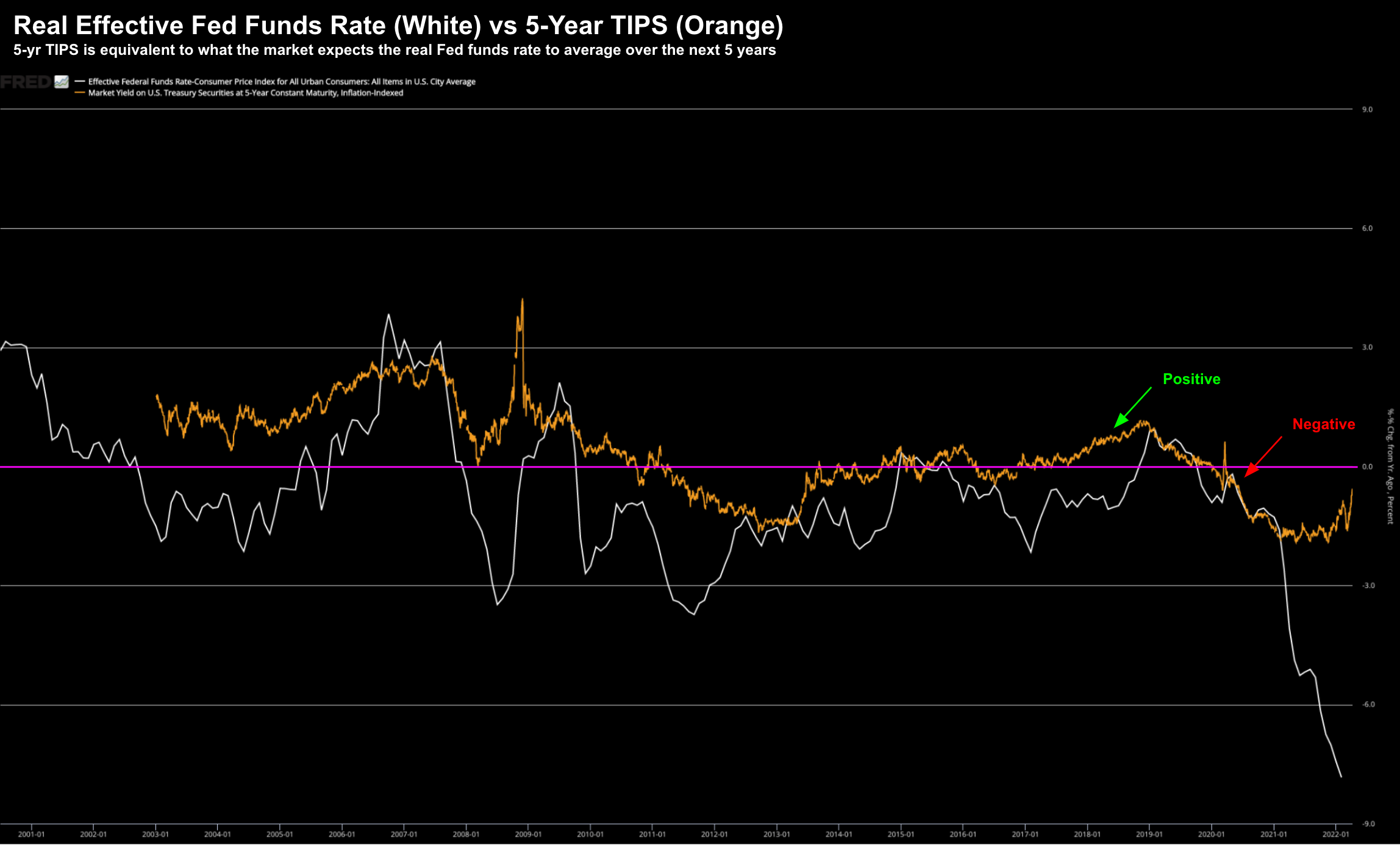

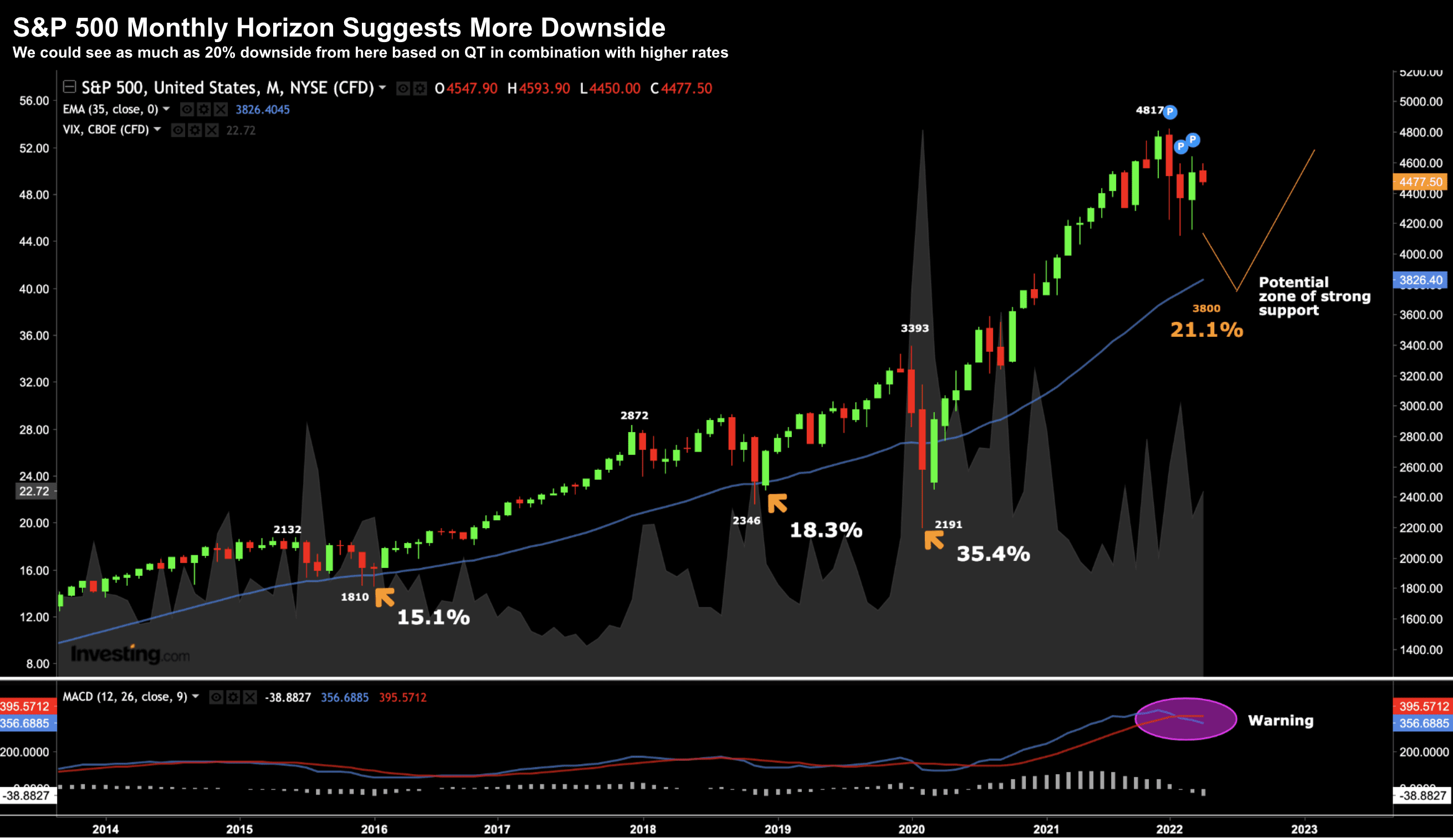

Is inflation peaking? If we knew the answer to that question - markets would be in a very different place.

The problem is - we cannot know for sure. However, there are positive developments...