Powell’s Ready to Cut… And Not Just Once

Powell’s Ready to Cut… And Not Just Once

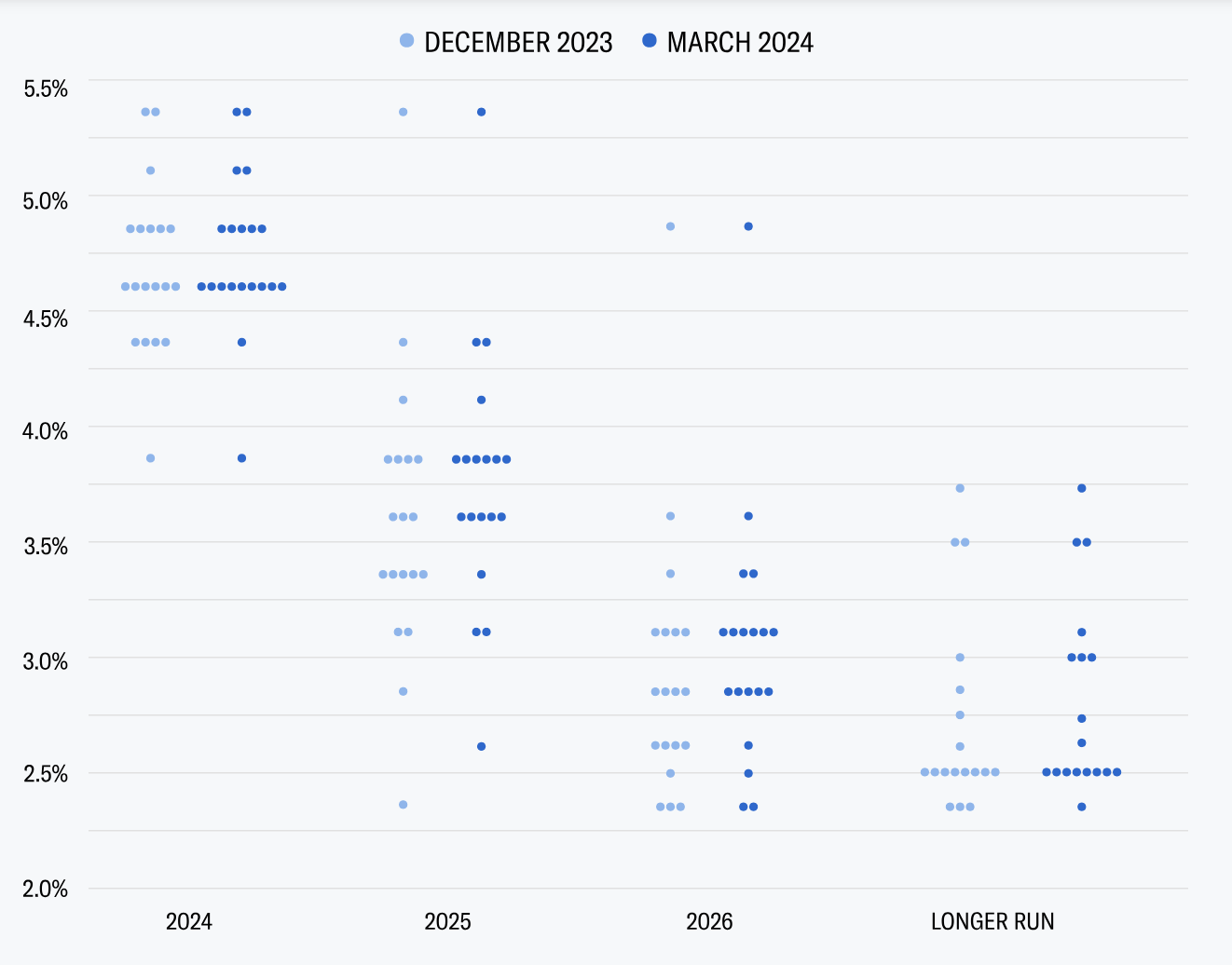

Today Fed Chair Powell delivered precisely what the market wanted to hear... help is on the way. As a perpetual (closet) dove - Powell did his best to stay balanced however the cat is now out of the bag. Rate cuts are coming. And there will be more than one. Consistent with other meetings - Powell said rate cuts are an option if economic data continues on its current path. In other words, it was the (same) scripted "data dependent" Fed.

However, there were some important nuances.