Cautious… But Invested

Cautious… But Invested

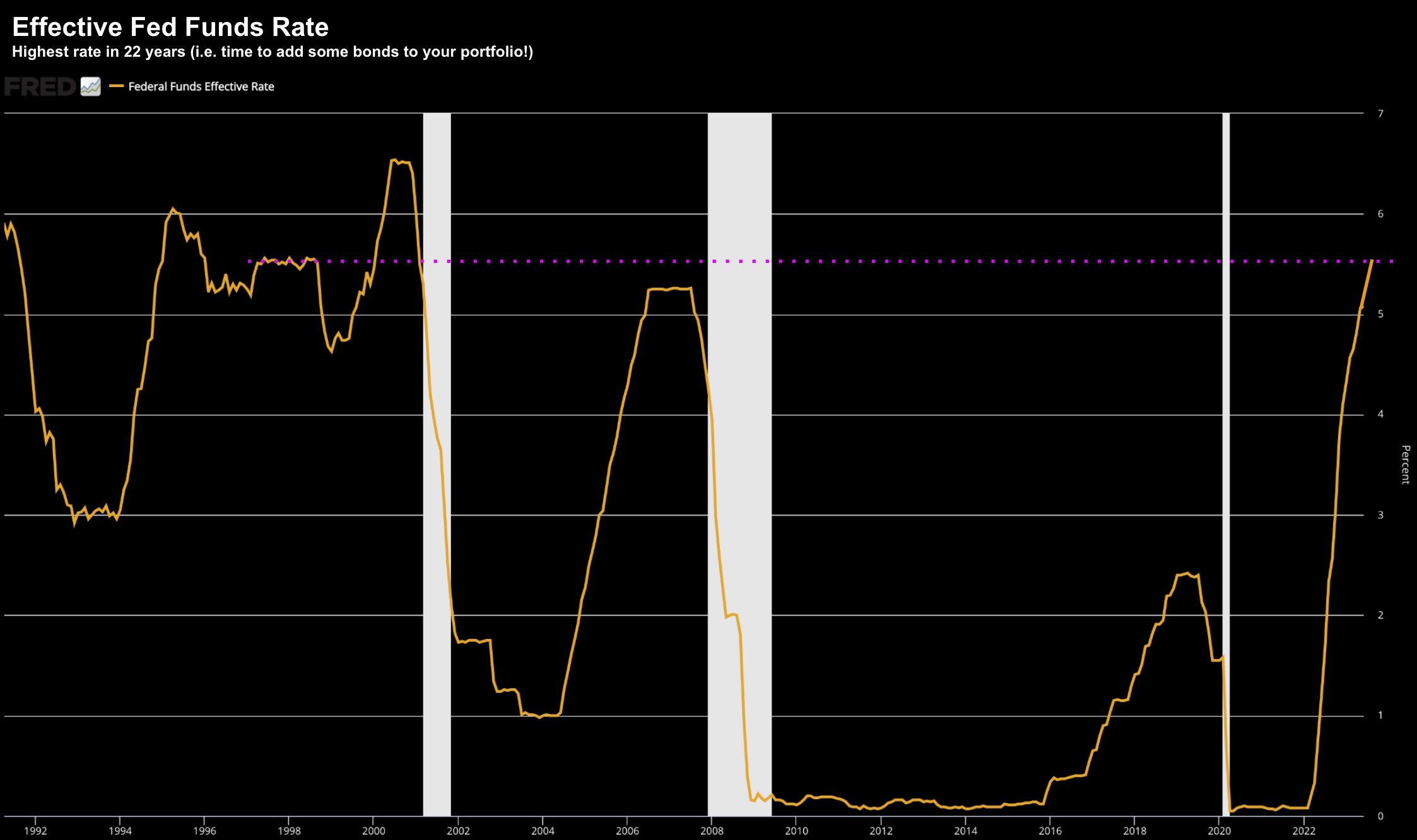

It's a brave person who is short the market. Probabilities suggest we are headed higher in the near-term. For example, previous episodes of Fed pausing suggests stocks typically gain. My sentiment today is best described as 'cautious... but invested'. To that end, one should always be invested to some extent. And whilst it's always unwise to be completely remiss of the risks -- it would be an even greater mistake not to have some exposure to higher quality risk assets and fixed income (at current yields)