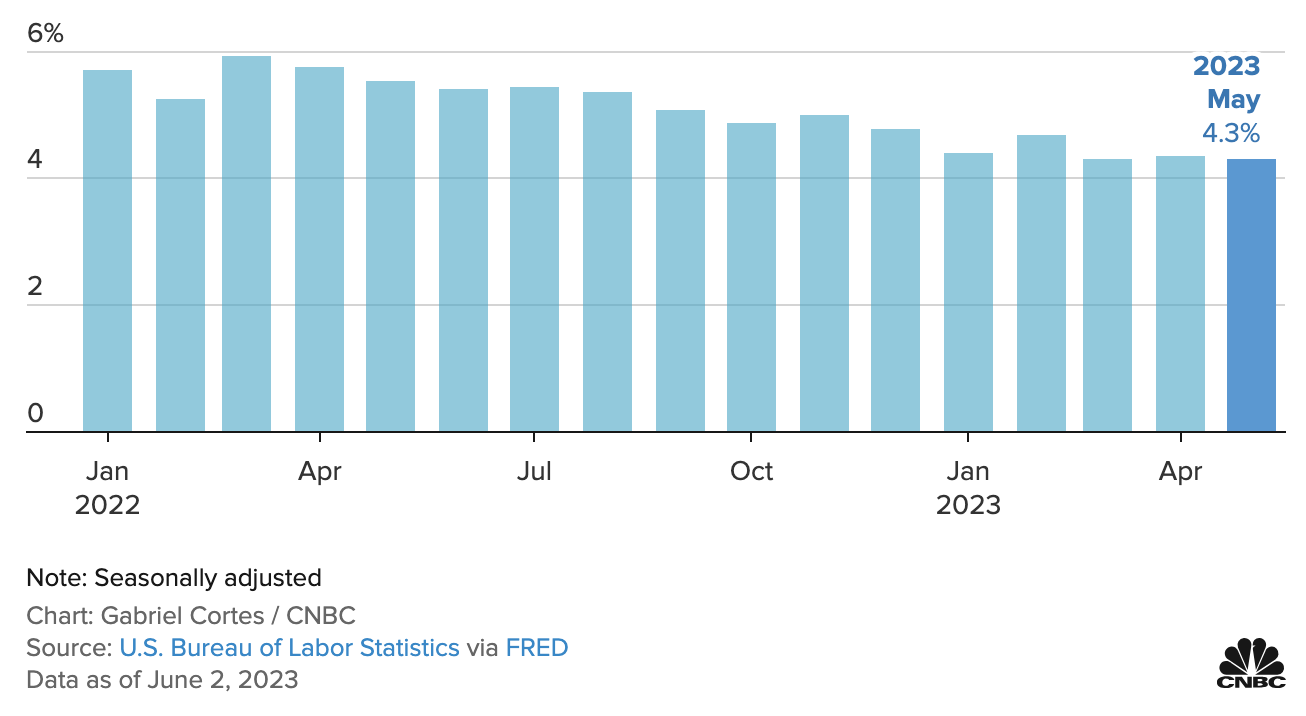

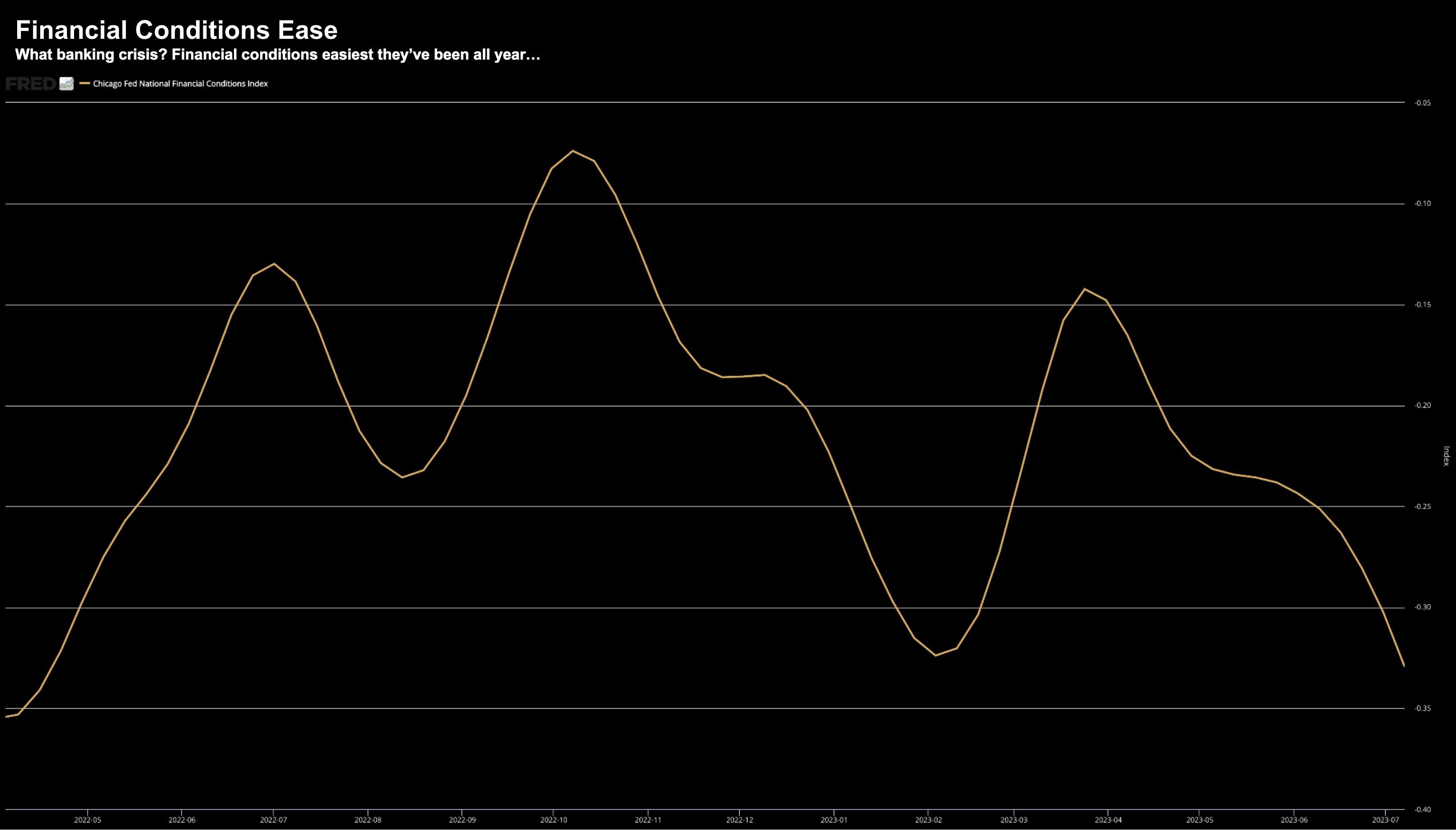

What Banking Crisis?

What Banking Crisis?

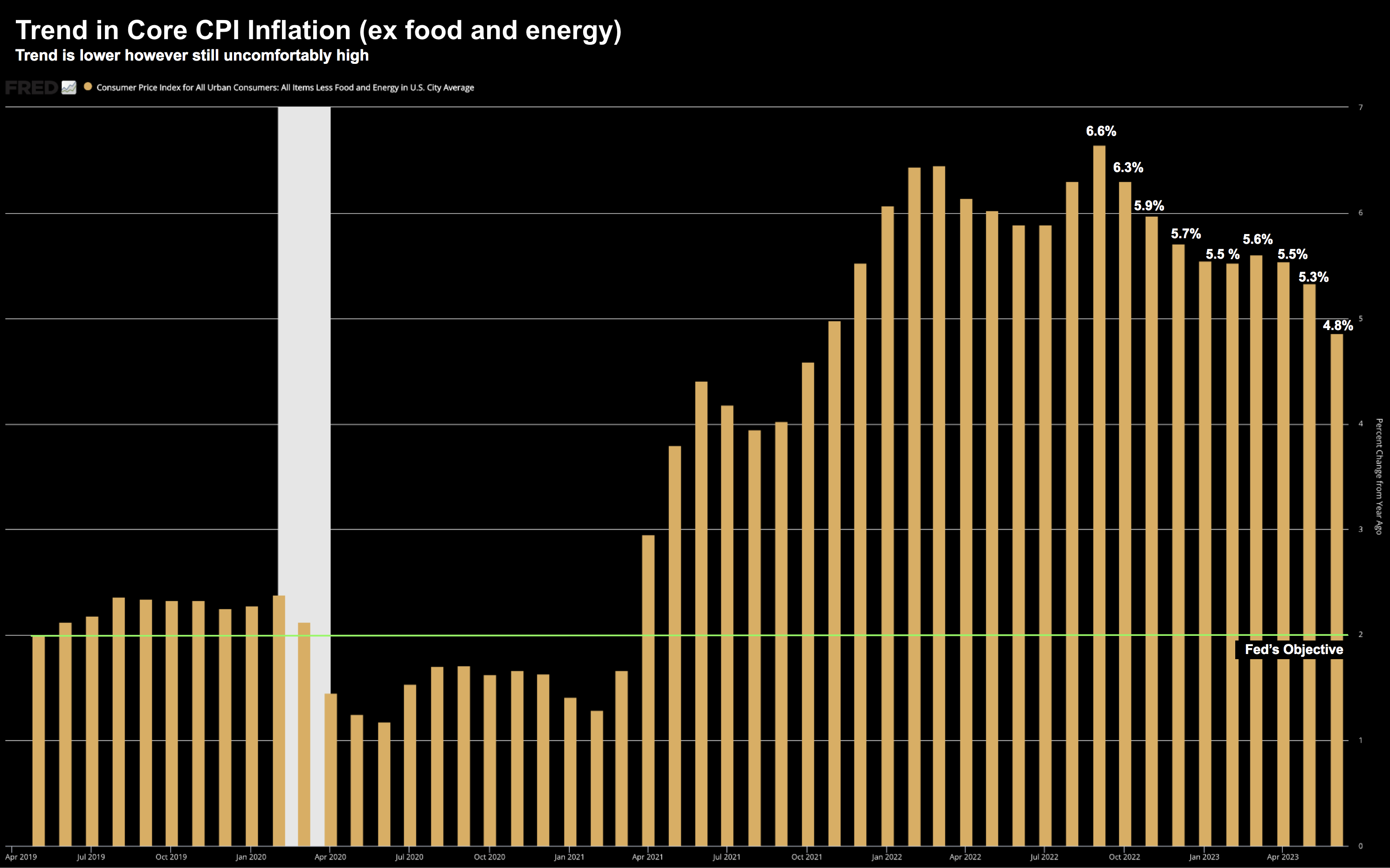

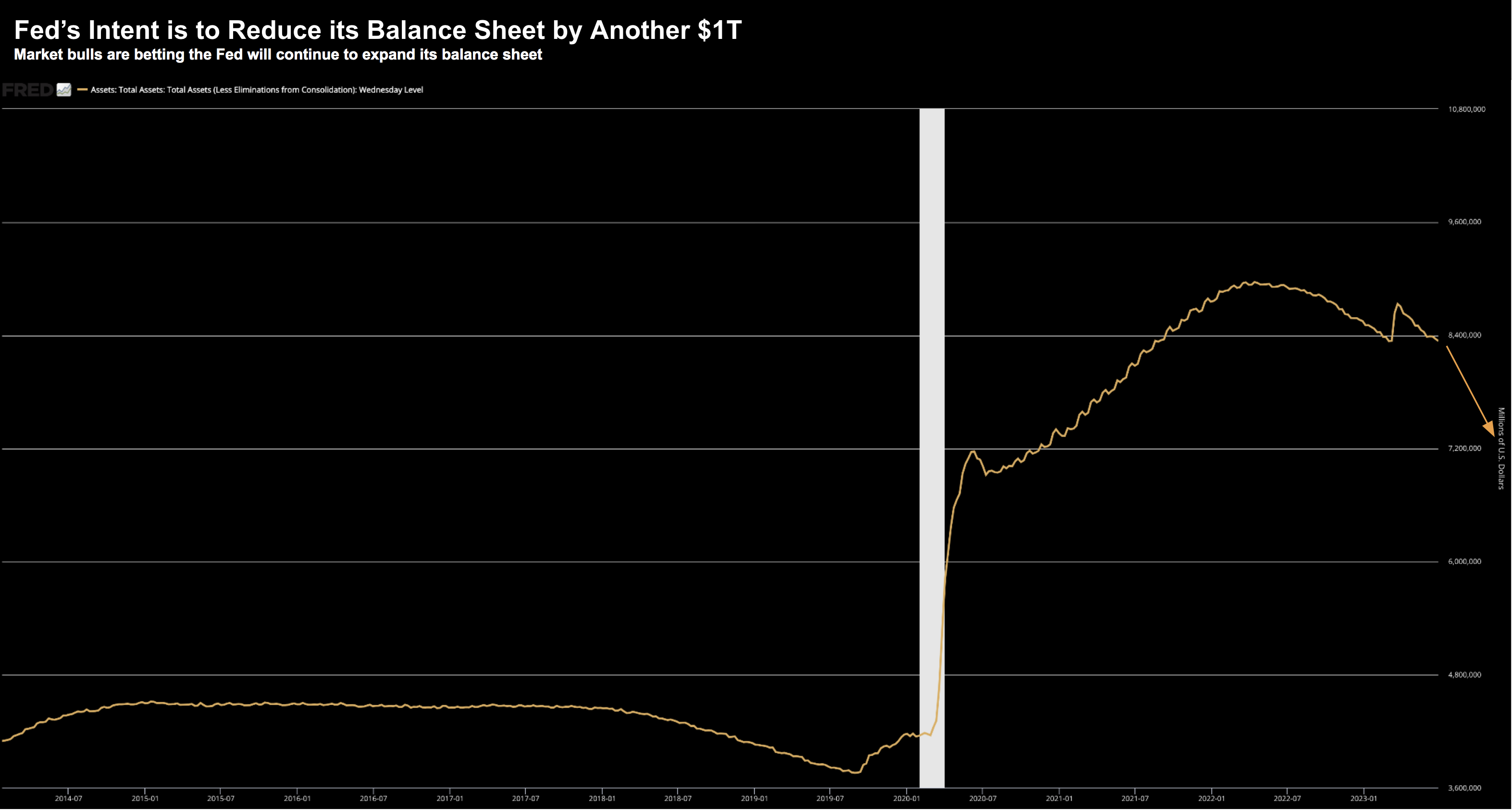

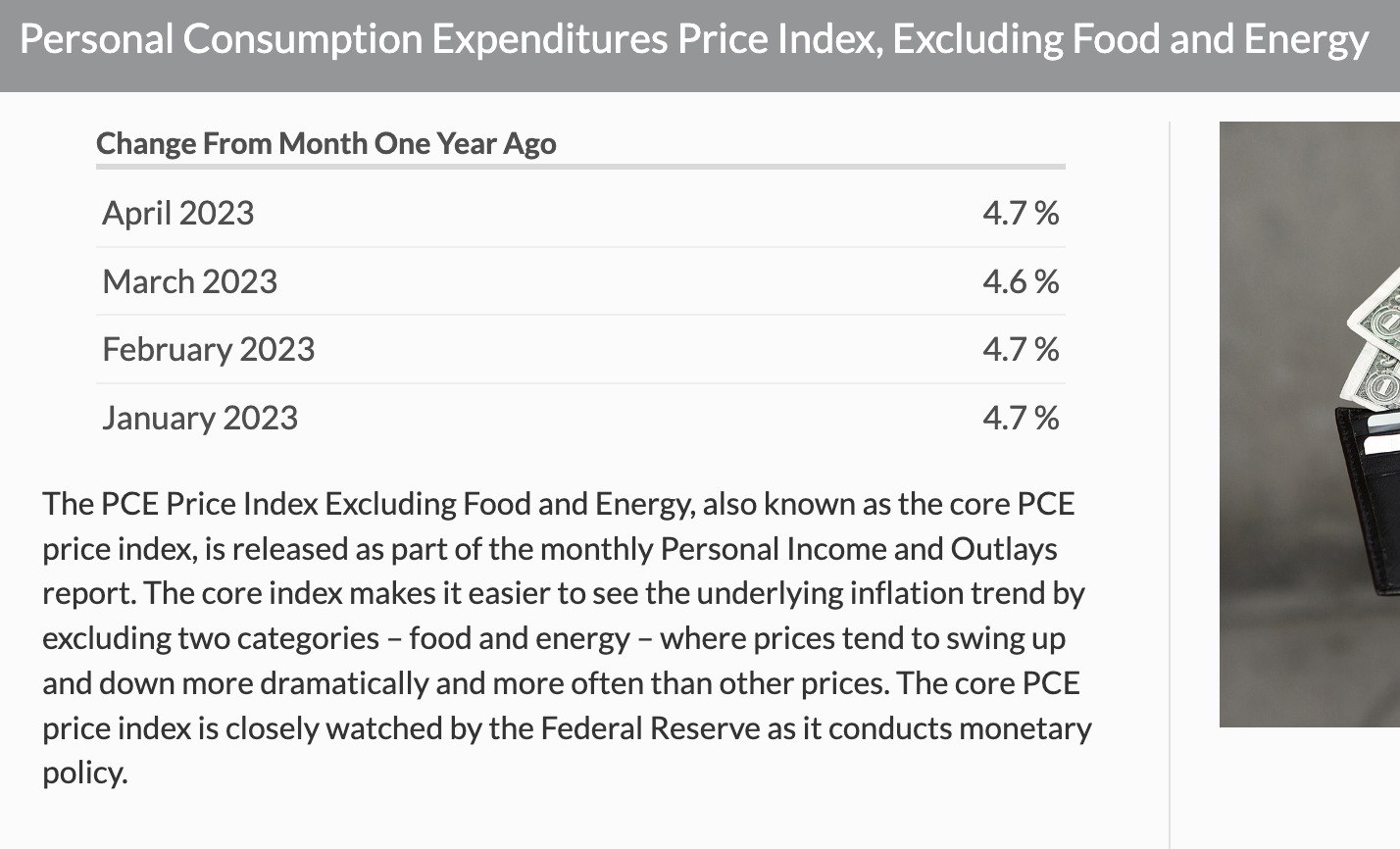

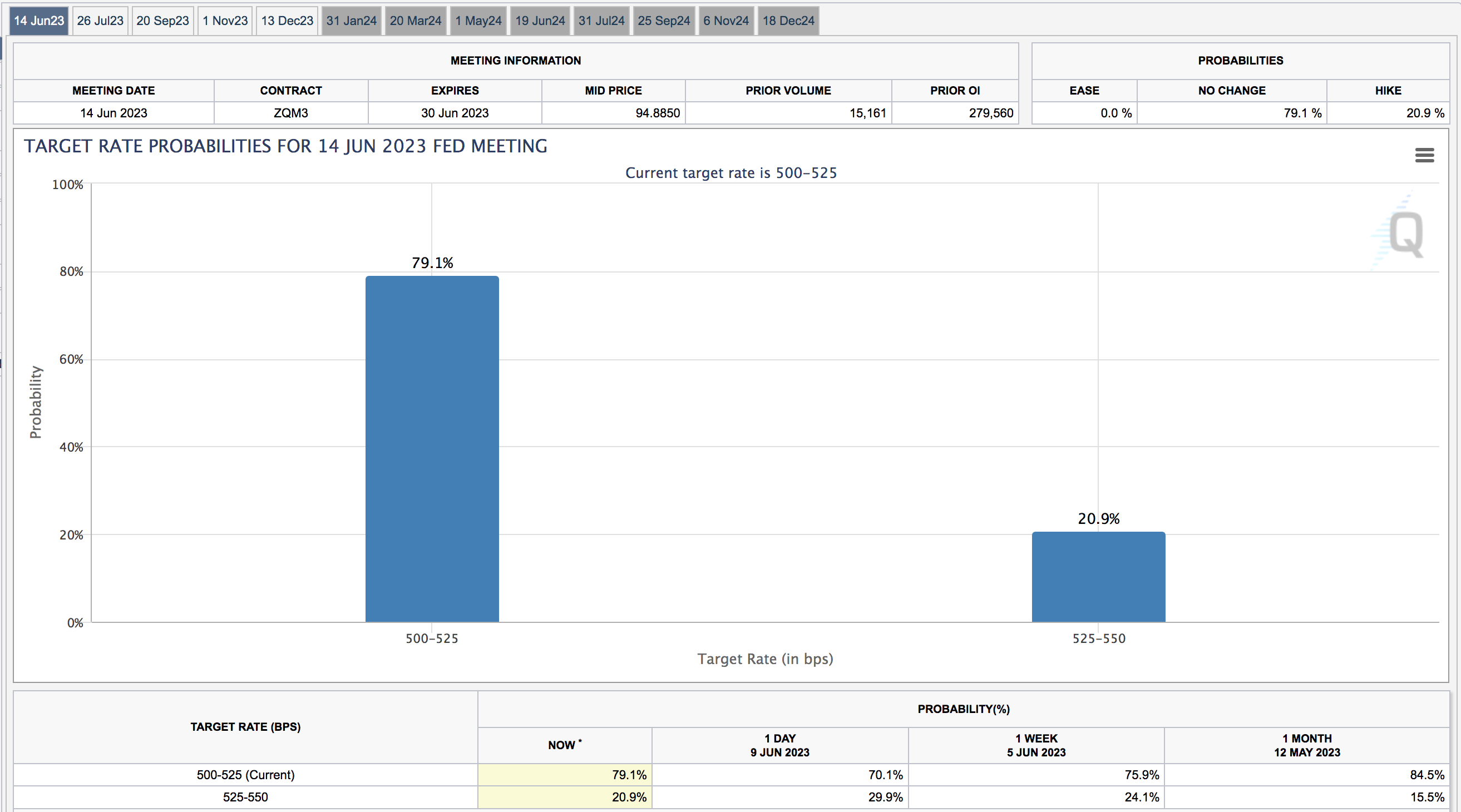

Are things actually looking up? If your measure is the equity market... you would say absolutely. Stocks continue to charge higher on the back of lower inflation and optimism the Fed is closer to the end of its hiking cycle. What's not to like? However, there's something else giving markets a boost. Easy money! Financial conditions are as easy as they've been all year. For example, it was only 4 months ago and we had a mini banking crisis... where funding was a lot tighter. That's now a distant memory.