The Fed Must ‘Choose their Poison’

The Fed Must ‘Choose their Poison’

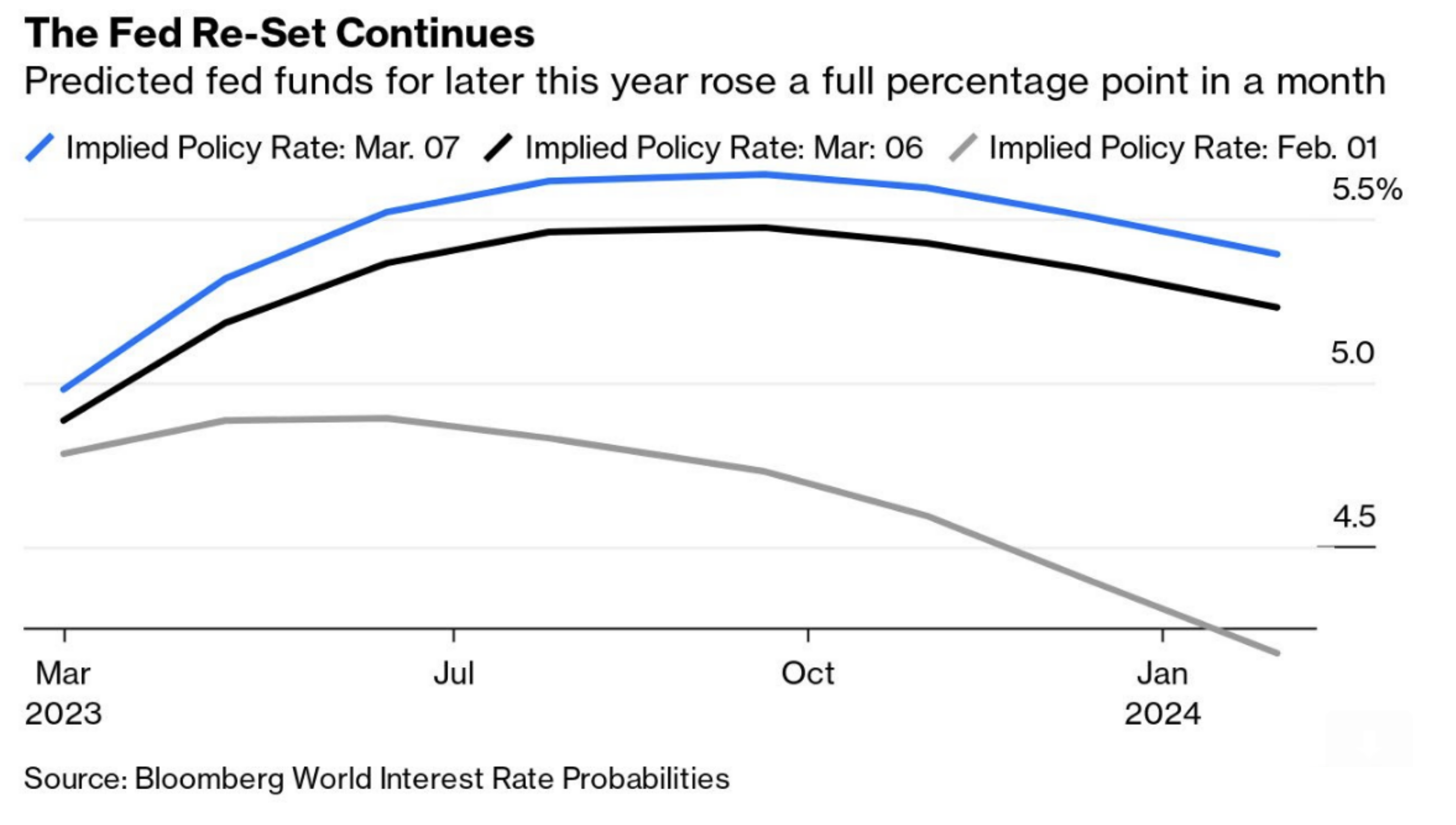

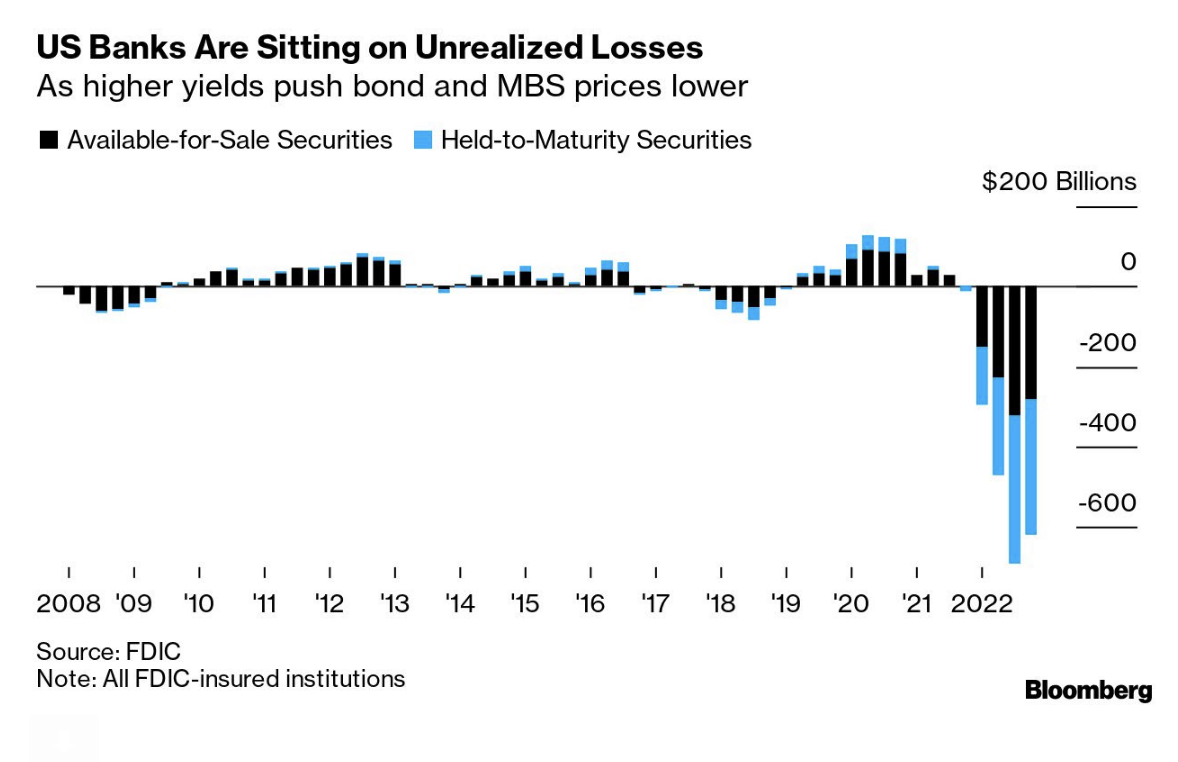

The collapse of SVB and tightening financial conditions has put the Fed in a very difficult spot. For example, prior to the collapse they had a green light to raise at least 25 bps. Not now. Tightening rates could cause further pressure in the banking sector. However, if they choose not to - what signal does that send. There are no easy choices...