The Ellis Framework: Why Real PCE is the “Seeing Around Corners” Metric for Market Cycles

The Ellis Framework: Why Real PCE is the “Seeing Around Corners” Metric for Market Cycles

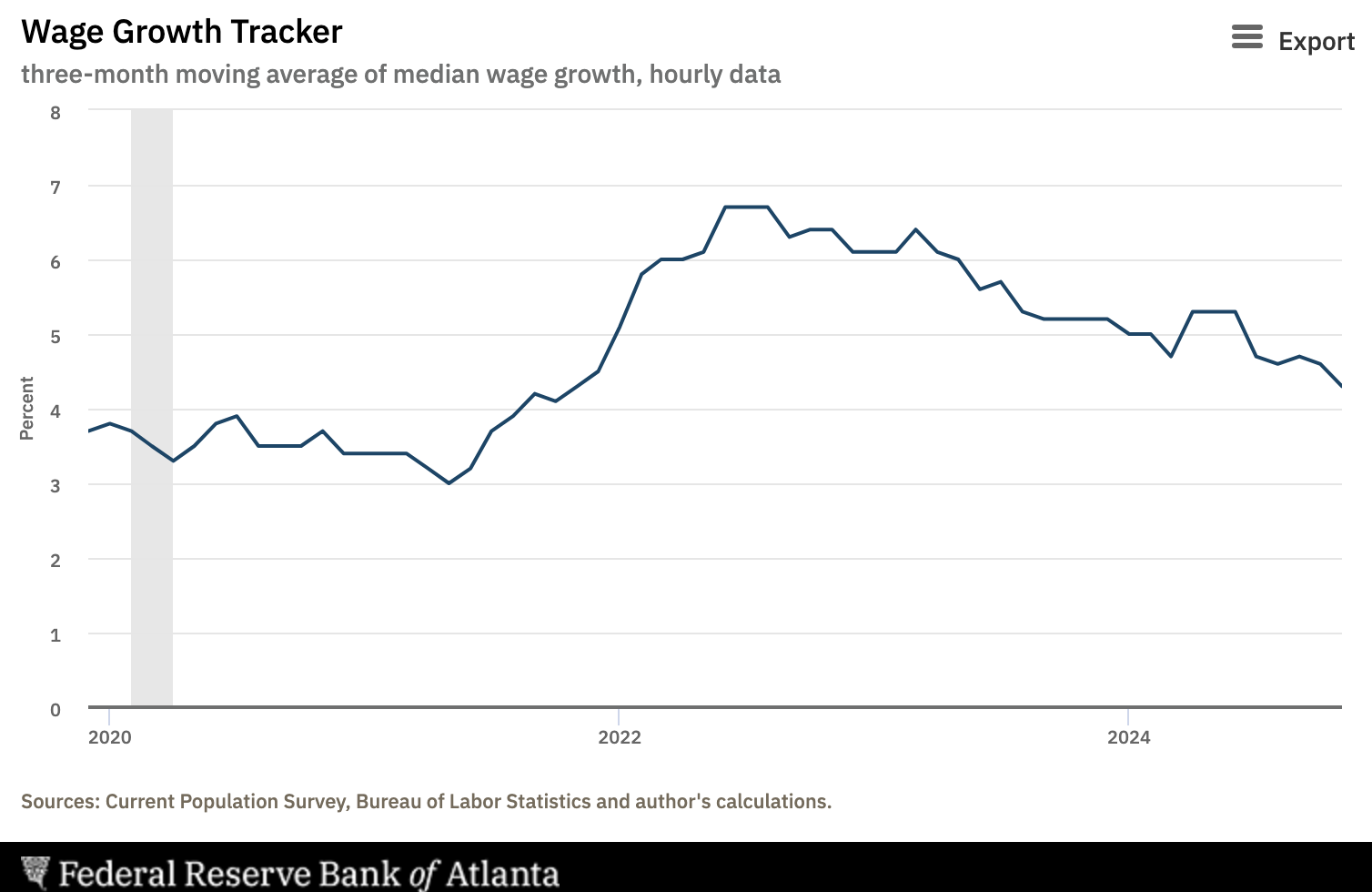

Headline indicators suggest economic resilience, but underlying data reveals structural cracks. While personal consumption remains high, it is increasingly fueled by government transfers rather than private wages. With real spending outpacing income and pending home sales plunging 9.3%, Real PCE serves as a critical leading indicator of an approaching market downturn