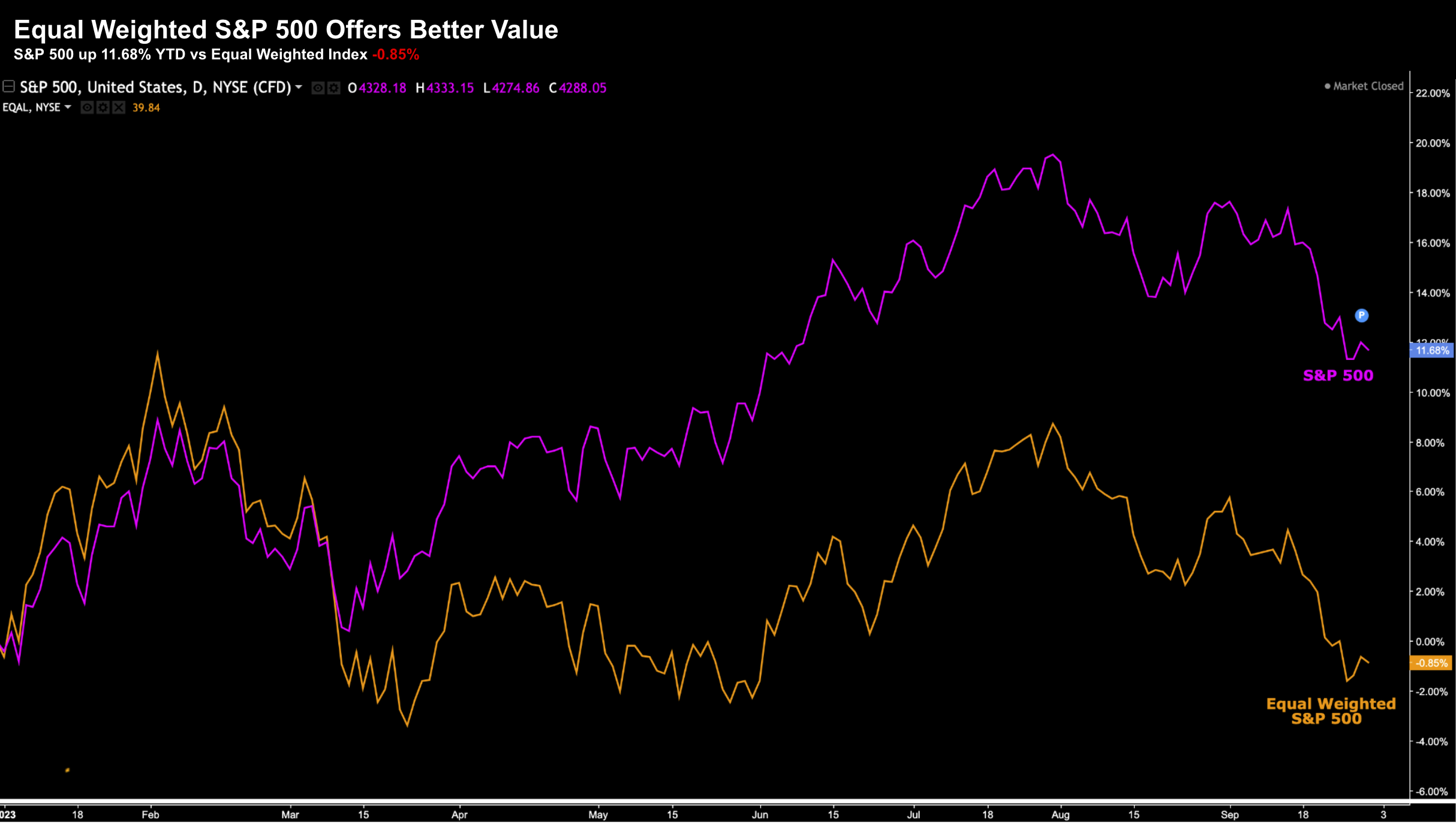

Fed Warns, Stocks Shrug

Fed Warns, Stocks Shrug

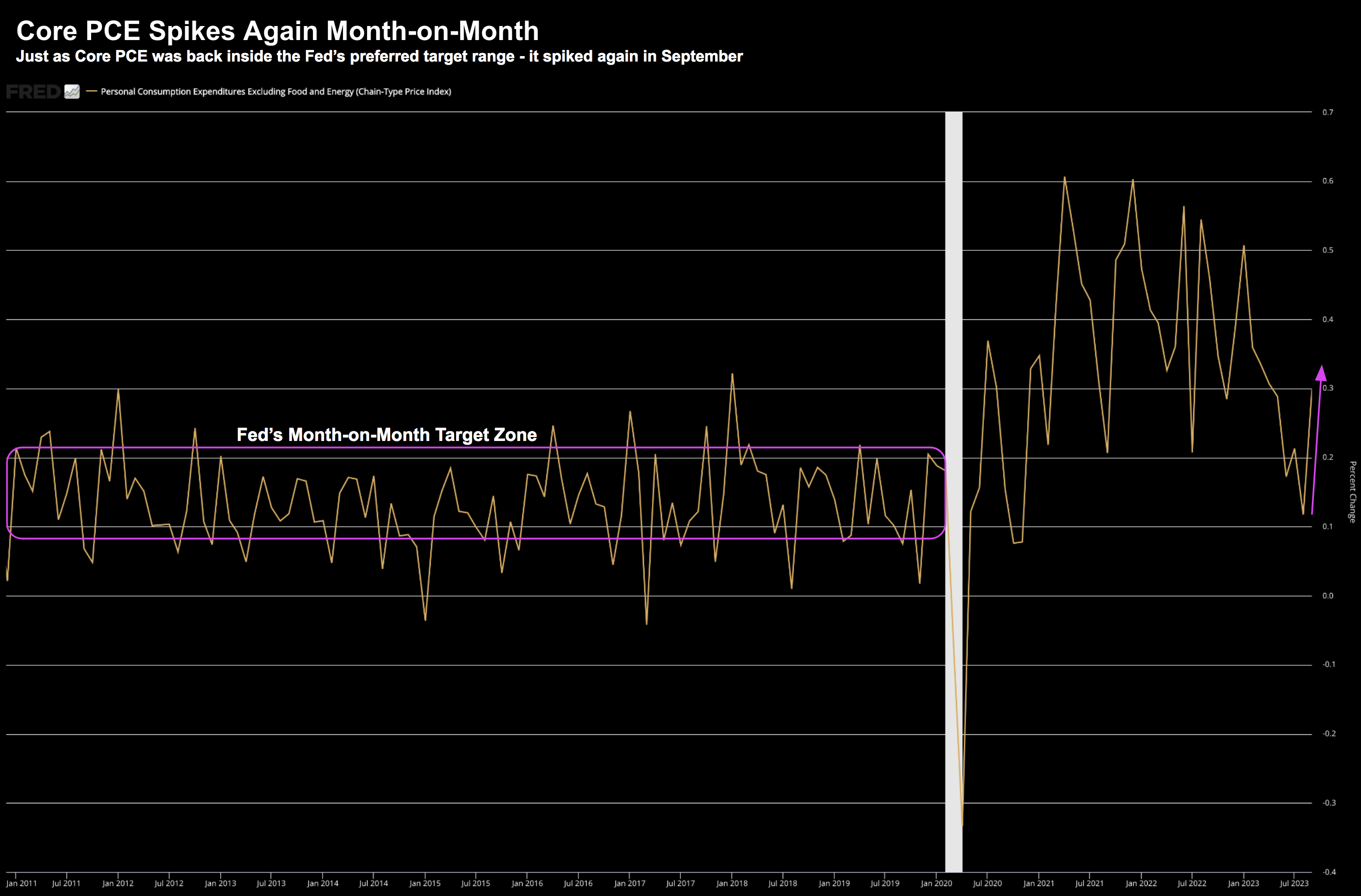

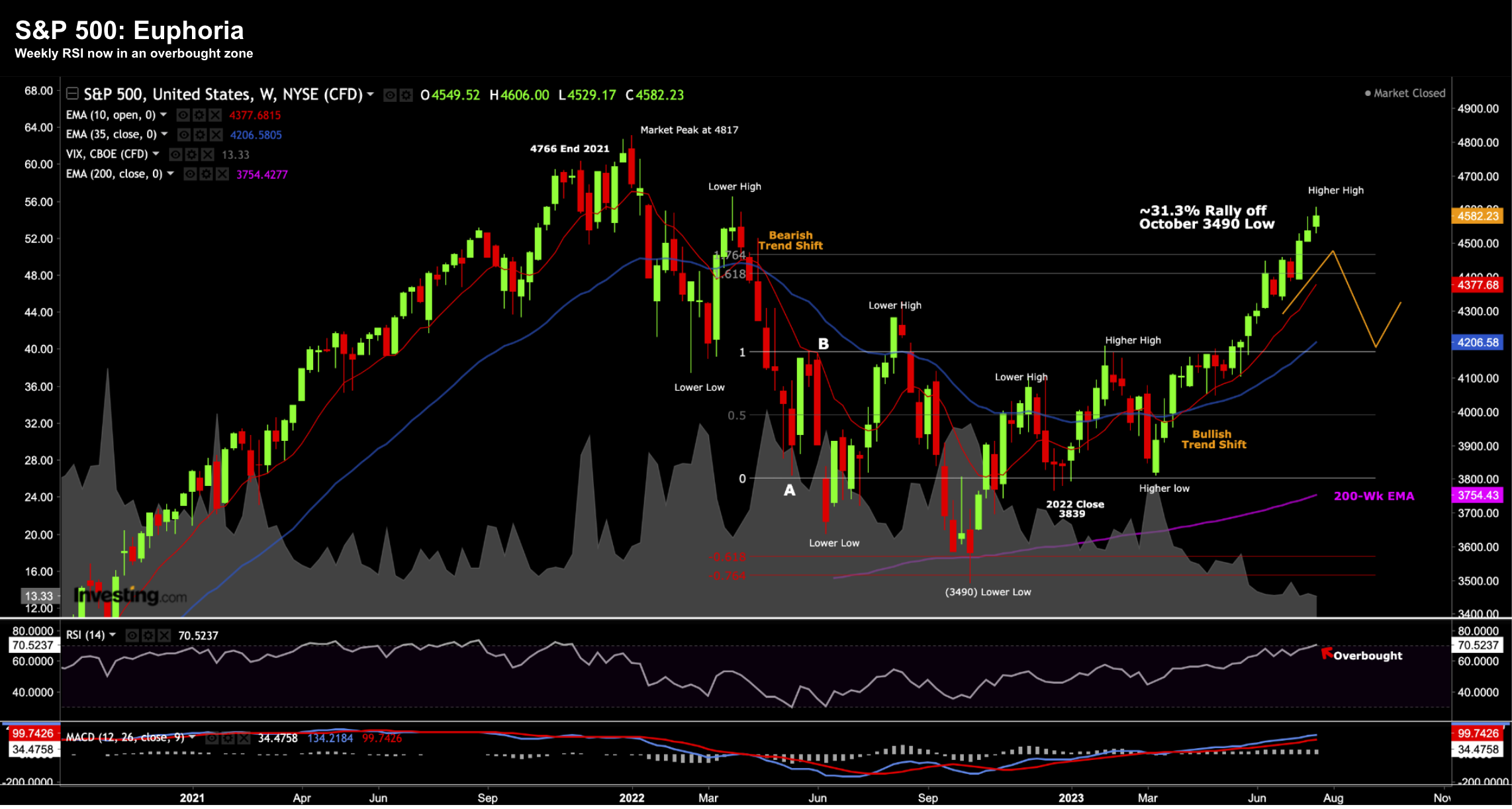

"We still have a long way to go" - that was the not-so subtle warning from Jay Powell this week. After what many felt was a slightly less hawkish Fed Chair last week - sparking an equity rally - Powell attempted to adjust his tone at an IMF event. Was he successful? That's hard to say - as equities seemed to shrug off any warning from the Fed - surging ahead to be up 15% year-to-date. Here's my question: are investors being too sanguine about what's still unknown?