Credit Cycles and Market Psychology: Navigating the Impact of Interest Rates on Long-Term Value

Words: 1,185 Time: 7 Minutes

- Understanding why markets remain tethered to monetary policy

- The challenge of "sticky" inflation in the service sector

- How to value quality when "animal spirits" drive prices higher

If you ever needed a reminder of how closely the modern market is tethered to monetary policy, you need only look at how quickly sentiment shifts based on a single data point. When investors perceive even a slight cooling in inflation, the reaction is often swift and aggressive.

Typically, we see stocks surge on the back of two primary catalysts:

- Consumer price inflation (CPI) data coming in even marginally better than expectations; and

- The resulting prospect that central banks, particularly the Federal Reserve, have more room to ease interest rates.

When the scent of "cheaper money" hits the air, it triggers what we call "animal spirits"—that human tendency toward action and speculation driven by emotion rather than cold calculation. Bond yields drop, stock prices jump, and suddenly the crowd is moving in a singular, optimistic direction.

However, it is often a mistake to jump to immediate conclusions based on a single report. Inflation is rarely a linear path downward. While headline figures might offer temporary relief, the underlying data often contains unresolved questions that require a more disciplined look. For instance, while some sectors see price relief, the "supercore" measure of inflation—which focuses on services while excluding shelter—can remain stubbornly high. This creates a disconnect between what the market wants to happen and what the reality of the data suggests to a cautious central banker.

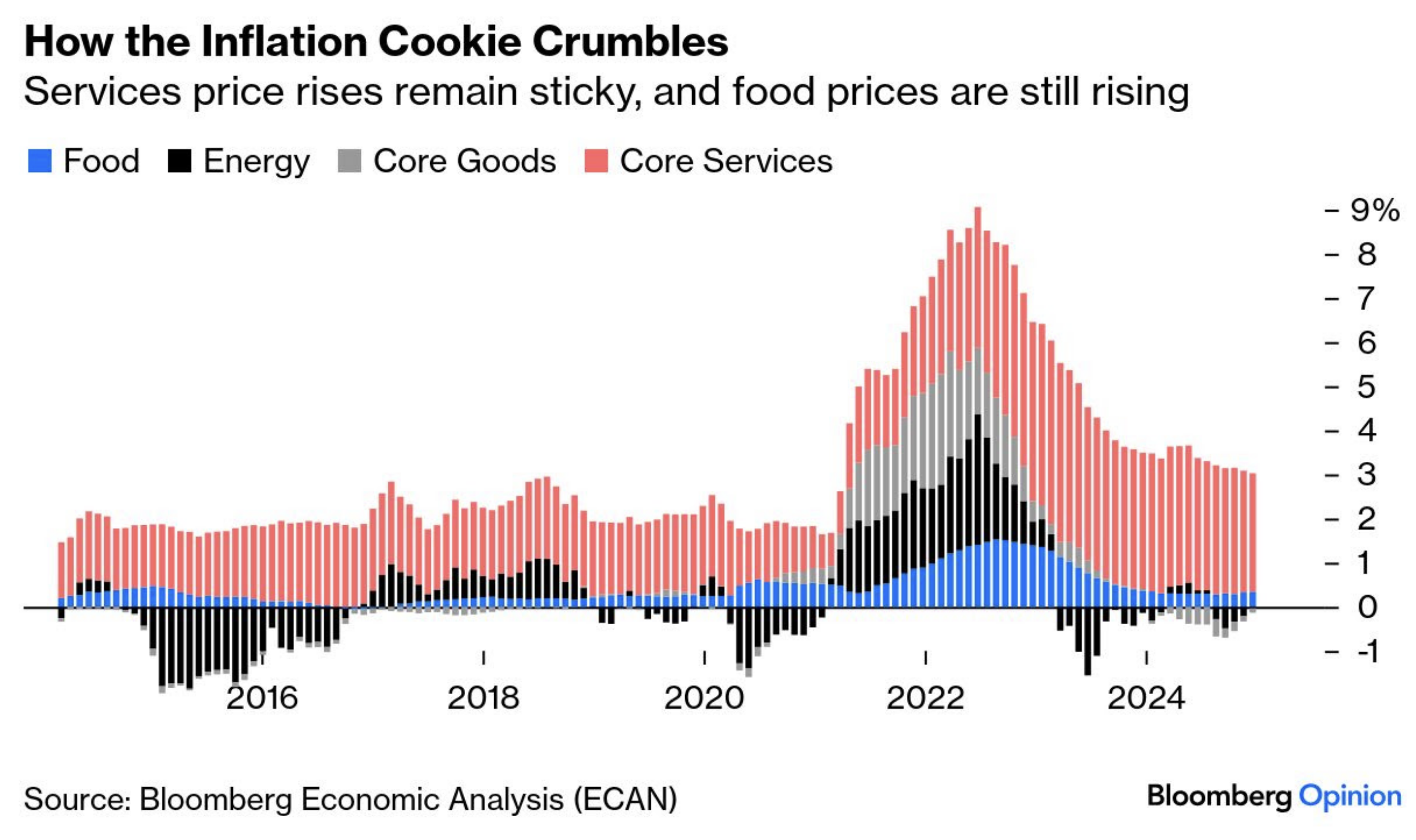

The Persistence of "Sticky" Services

To understand the long-term health of the economy, we have to look past the headline numbers and into the components that drive the cost of living. Often, the data shows a divergence between goods and services. While energy and goods prices might stabilize or even fall, the service sector frequently remains "sticky."

Consider the typical breakdown of modern inflation:

- Headline CPI: The broad measure of price increases across the whole economy.

- Core CPI: Inflation that strips out volatile food and energy costs to find the underlying trend.

- Shelter Prices: A massive component of the index that often lags behind real-time market changes.

When these figures show a slight slowdown, equities are quick to celebrate. We see long-term yields drop and indices like the S&P 500 pile on significant gains. But is this move justified by the fundamentals, or is it a result of the "incentive-caused bias" where traders see exactly what they want to see to justify buying more?

Instead of focusing on when the next rate cut arrives, we should reframe the question: which businesses in a portfolio are most vulnerable if the "cheap money" era doesn"t return as quickly as the crowd expects?

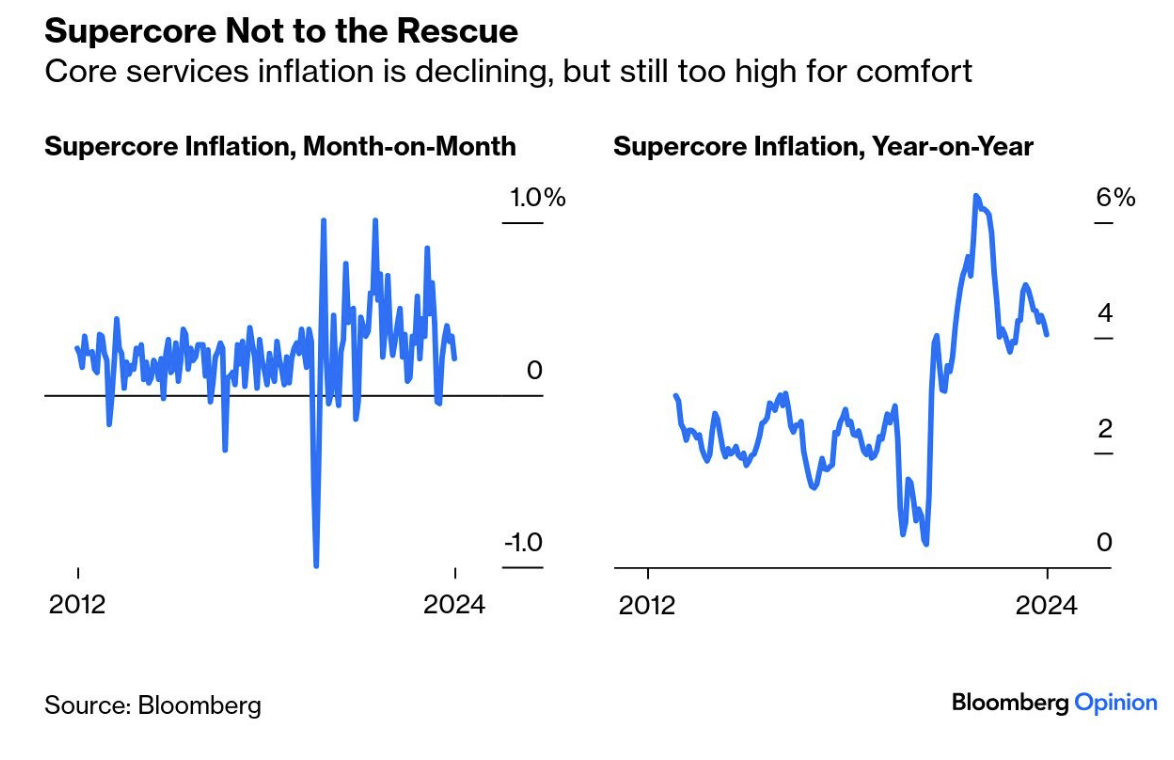

The most persistent challenge for the Fed remains services. For over a year, we have seen a pattern where inflation is driven primarily by two sources: Core Services (including shelter) and Food. Meanwhile, goods prices have remained relatively stable.

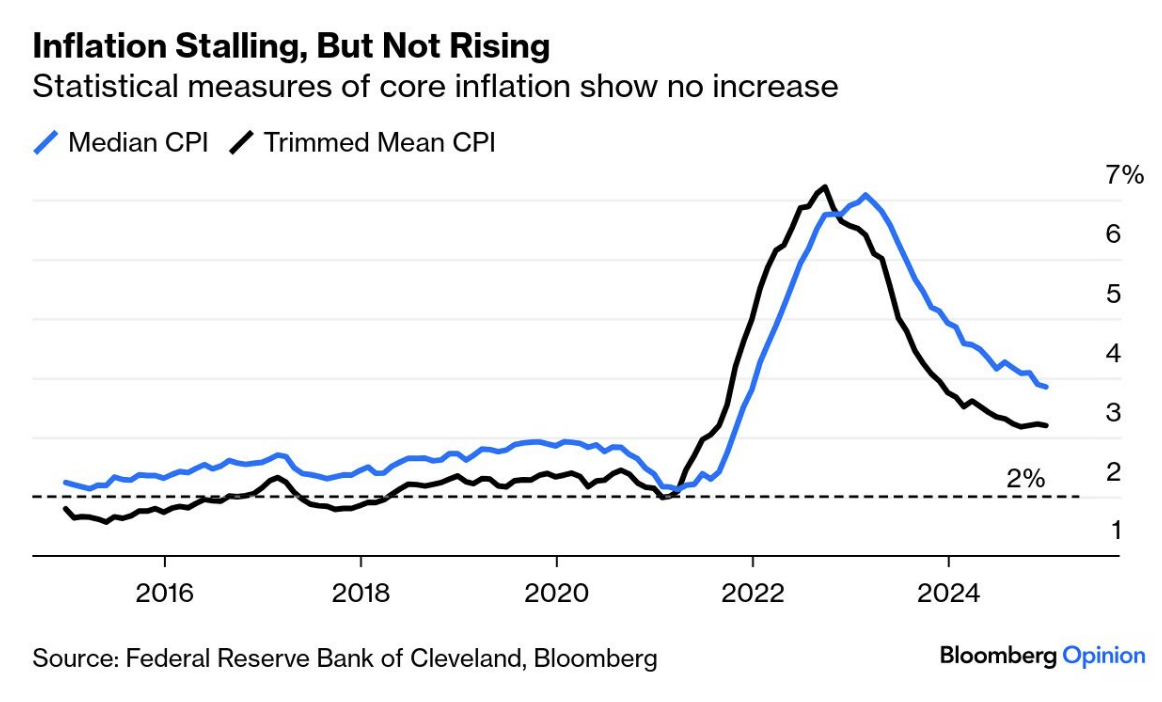

More refined statistical measures, like "trimmed mean" inflation, often show a more gradual decline than the headlines suggest. This indicates that while the fire is being managed, it is far from extinguished. Here"s another way to think about the problem: if inflation in the service sector remains a structural fixture rather than a temporary hurdle, how does that erode the long-term margins of the companies you own?

When the "supercore" rate remains high, we have to look at the primary driver: wages. While a slowdown in wage inflation for lower-income workers might ease some inflationary pressure, it also raises questions about the strength of the consumer moving forward.

Wage Growth and Quality Investing

The labor market is a double-edged sword. Strong wages fuel consumption but keep inflation high. If the labor market stays tight, central banks have less incentive to cut rates. The market, however, behaves like a patient waiting for a specific prescription; it is hypersensitive to any news suggesting the "medication" of lower rates is coming soon.

This "risk-on" attitude often causes consumer discretionary stocks to outperform defensive staples. But for the long-term investor, this is where discipline matters most. We must focus on the principle of strong returns on capital and consistency over time rather than chasing the latest pivot in sentiment.

Valuing the S&P 500: Hopes vs. Reality

When optimism rises, we often see the market erase months of previous caution in just a few days. But the technical lens often tells a more sober story. Even in a strong rally, we find overhead resistance and "negative divergence"—where price keeps rising but momentum indicators like the RSI begin to fade. This is often a sign of a market that is "exhausted" and over-extended.

The real hurdle is always earnings and, more importantly, forward guidance. While many expect high earnings growth from the "Magnificent 7" or large-cap tech, the market will eventually demand to see a measurable return on the massive capital expenditures being poured into new technologies like AI.

This brings us to the importance of the 15/15 Rule. This is a fundamental filter I use to find high-quality, durable businesses. It requires a company to maintain a Return on Equity (ROE) of at least 15% and a Return on Invested Capital (ROIC) of at least 15%. Why 15%? Because it serves as a litmus test for a business that is not just growing, but compounding its internal capital efficiently. If a company can"t generate strong incremental returns on the money it reinvests, it is eventually going to hit a wall—regardless of what the Fed does with interest rates.

Take a company like Apple. It is an incredibly high-quality business, but everything has its price. Investors should reframe the issue this way: what specific set of circumstances would have to occur for a multiple of 30x earnings to be considered a bargain in five years, and how likely is that reality? When the price exceeds the fundamental value, even the highest quality company can become a poor investment. For me, selling a position like Apple at $254 wasn"t a comment on the business quality, but a refusal to pay for a multiple I couldn"t justify. A "fair" price might be closer to 22x earnings, but even then, "fair" isn"t a bargain; it"s just reasonable.

Putting it All Together

The market"s reaction to shifting economic data is often overdone. While short-term relief is welcome, it rarely resolves the broader uncertainties. No one can forecast the central bank"s next move with absolute certainty, yet the crowd will always attempt to front-run the next "pivot."

We are currently seeing strong earnings growth across many sectors, which is why prices have remained resilient. But we must ask ourselves: does a strong growth rate justify paying historical premiums when yields are still significantly higher than they were a few years ago?

Ultimately, a robust framework is what allows an investor to survive these cycles. Luck can deliver a good outcome from a poor decision, but luck is not a strategy. What matters is the consistent application of a disciplined approach—focusing on quality, strong incremental returns on capital, and refusing to follow the crowd over the cliff of overvaluation. Momentum is a powerful force, and expensive markets can always get more expensive. But when the tide shifts, you want to be holding businesses that don"t rely on "animal spirits" to sustain their value.