Anatomy of a Supply Shock: Using Data Frameworks to Filter Market Noise

- Frameworks to assess the impact of the war

- Lessons from the previous oil spikes

- Finding resilient capital in a stagflationary world

In the world of macro investing, we often see years where less happens in the energy markets than what we have witnessed in just the opening days of a geopolitical crisis.

These moments tend to act as a "truth serum" for the markets—exposing exactly who is swimming naked when the tide of cheap energy goes out.

Recent spasms in the Middle East, characterized by leadership transitions and sudden military escalations, provide valuable lessons in market psychology.

For example, we saw crude prices surge toward $120—a rise sharper and more sudden than the opening days of the Ukraine invasion—only to retreat below $90 within hours.

This volatility settles nothing regarding the conflict, but it tells us everything about the current state of trader nerves.

When sentiment is in the driver"s seat, the crowd is prone to recency bias.

For example, some investors (and consumers) are of the belief that because oil jumped 10% today, it is likely to jump 10% tomorrow.

Case in point:

I"ve seen news coverage of people lining up at fuel stations to not only top up the tank – but filling up as many spare gasoline cans as they can.

That"s recency bias.

For investors – instead of getting caught in the news cycle – the question to ask is whether $100+ oil is a signal of:

- a permanent structural shift in the global economy; or

- is the market"s inability to sustain that price actually the "tell" regarding weakening global demand?

Data Over Drama

Geography has once again asserted itself as a primary driver of returns.

While U.S. indexes have remained surprisingly calm (barely down 1-2% since the war started) — Asian and European exchanges—physically closer to the conflict and heavily dependent on energy imports—sustained severe losses.

The U.S. is currently acting as a relative safe haven, but an intelligent investor must look deeper than the surface.

Consider the "smart money" in the futures market.

While the headlines scream "$120 oil" (in turn, panicking the consumer) – the 6th-month futures for Brent crude are pricing oil significantly lower, near $80.

Now if the mathematical reality of the futures curve is leaning toward a resolution, why are so many investors liquidating their highest-quality assets based on a spot price that the professionals expect to be temporary?

The answer – recency bias.

History (and the data) suggests that "cooler heads" will eventually prevail.

When the social proof of a panicking crowd is at its loudest, the disciplined investor trusts the data over the drama.

Identifying a True Bear Market

Two frameworks, in particular, help us determine if a geopolitical shock will morph into a structural economic disaster.

With respect to the first model – Societe Generale"s Manish Kabra suggests that only two variables matter:

- Shock Duration; and second

- Federal Reserve"s Reaction Function.

Most oil spikes peak within three months; the danger only arises if the shock outlasts that window.

By way of example, below is a 20-year S&P 500 chart vs the change in crude prices (in orange):

There have only been 3 occasions over 20 years that sustained higher price saw equities decline by 20% or more.

Only one of these coincided with a recession (2008)

Taking this further, Henry Allen of Deutsche Bank provides a three-part checklist that must be met for a risk-off bear market to follow an oil shock:

- A Sustained Spike: An oil price increase of +50-100% that is sustained over several months, not just weeks.

- A Hawkish Policy Response: The shock forces central banks into a sharp, hawkish pivot to fight inflation—even at the expense of economic growth.

- Broader Macro Damage: The shock is severe enough to tip an already-slowing economy into an outright recession.

In terms of a potential hawkish pivot – the market has priced in one to two rate cuts this year.

If those cuts are taken away because the Fed is more worried about the "inflation" side of the stagflation equation, it implies significant downside for equities.

Which prompts a question:

If the "AI stimulus" that has powered markets is a story of future productivity, but energy inflation is a story of current survival, which narrative will the Federal Reserve prioritize when they meet next?

Supply Choke and its Impact

Inflation is defined as excess cash chasing too few goods.

Today – the continuous supply of goods (e.g., energy and fertilizer) is under threat as a result of the conflict (and its duration)

For example, data from Factset and Oxford Economics demonstrates that trade through the Strait of Hormuz can dry up almost overnight.

This waterway is not just an oil route for 20% of global demand (mostly China and Europe); it is a global artery for nitrogen-based fertilizersthat underpin the world food supply.

If the flow of fertilizer remains impeded, the inflationary impact will eventually collide with the U.S. consumer in a way that goes far beyond the gas pump.

I could be wrong – but I doubt that"s something the President wants during an Election Year?

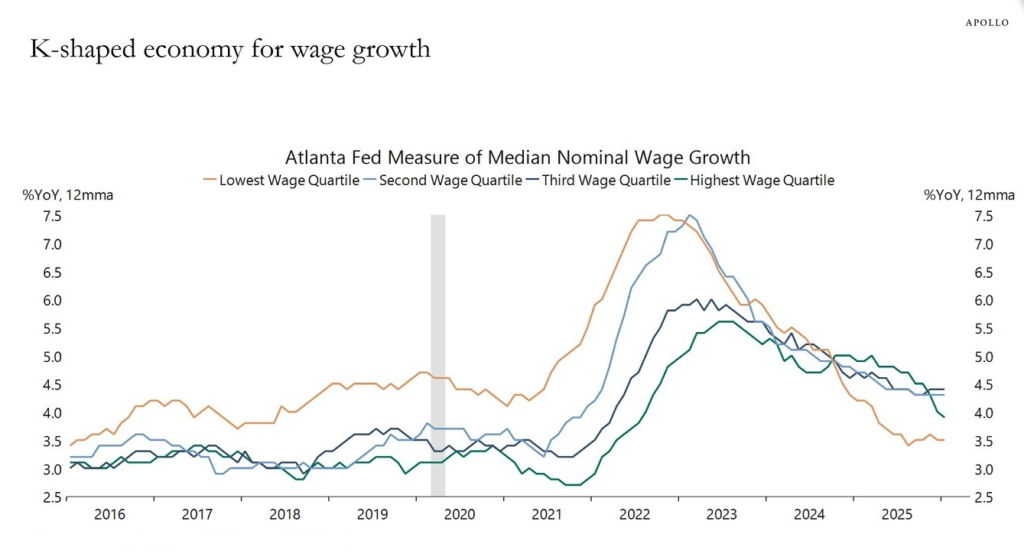

Further to previous posts – we"re already seeing "cracks" in lower-income delinquency data—credit card and auto loan defaults are rising.

Now if the lower "K" is already operating without a large margin of safety (as wage growth slows) – can the "wealth effect" of a rising stock market really compensate for a structural rise in the cost of energy and food?

And that"s a question for the Fed….

Putting it All Together

Monday"s extraordinary gyrations in oil settled nothing, beyond showing that there is still a significant amount of residual optimism in the market.

Day-to-day movements of "2%" in either direction may make for good headlines – but it"s just noise for those who focus on a business" long-term fundamentals (e.g., balance sheet, cash flow, margins, return on invested capital etc).

For the long-term investor, the process remains the same: instead of asking how much you can make if things go right, focus relentlessly on what could cause you to fail.

Coming back to the frameworks I shared earlier:

- Monitor the duration of the shock. If it goes several months – this will be problematic.

- Watch the Fed"s reaction; the market is not pricing in a hawkish pivot; and most importantly

- Ensure the bulk of your investment capital is parked in high quality business that don"t require (i) artificially low interest rates to prosper; or (ii) oil prices below "$60" to be profitable.

By being consistently not stupid, we allow the compounding of quality assets to do the heavy lifting.

When the tide eventually shifts, you want to be the one who was prepared, not the one who was caught panicking over higher energy costs.