It’s Not If “Long & Variable Lags” Hit… It’s When

It’s Not If “Long & Variable Lags” Hit… It’s When

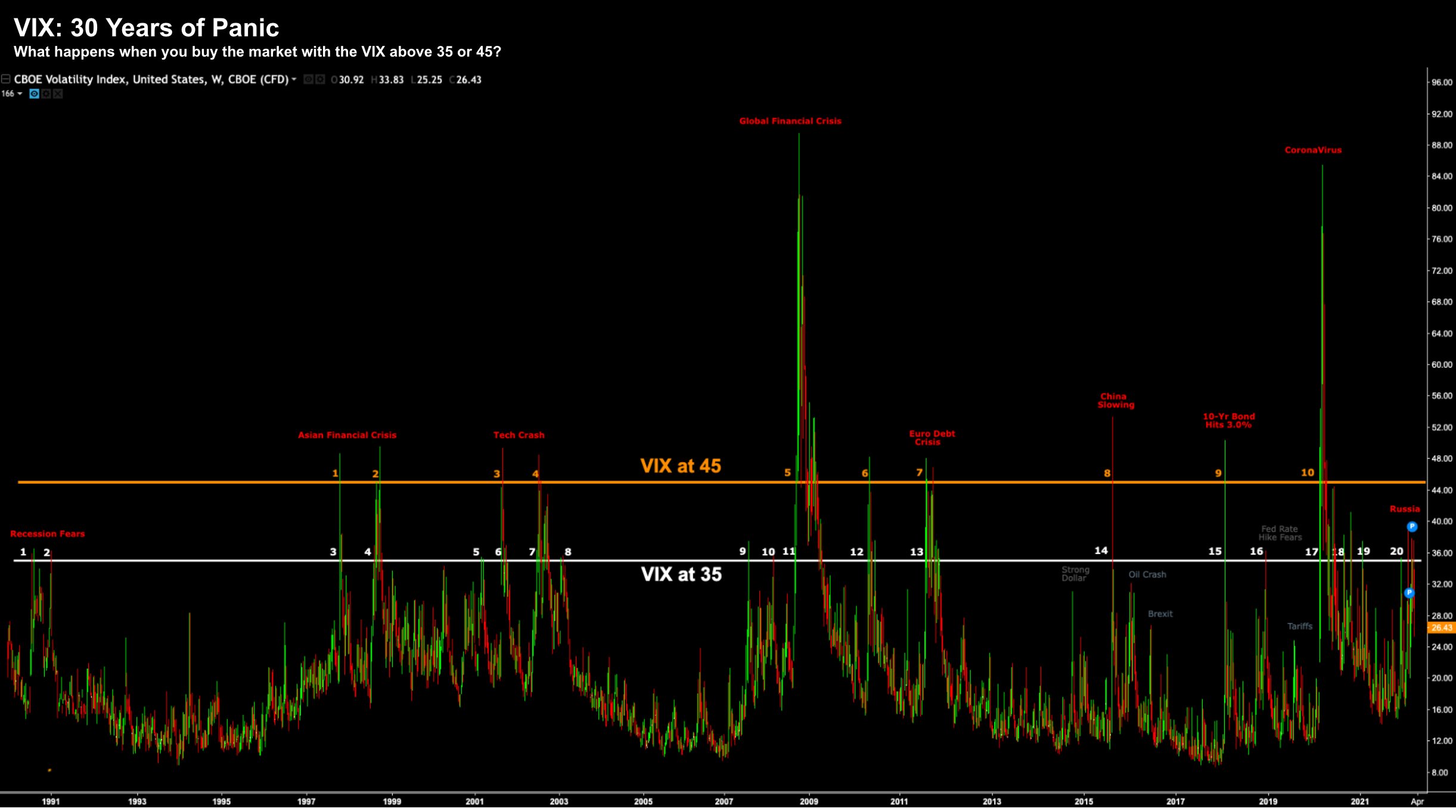

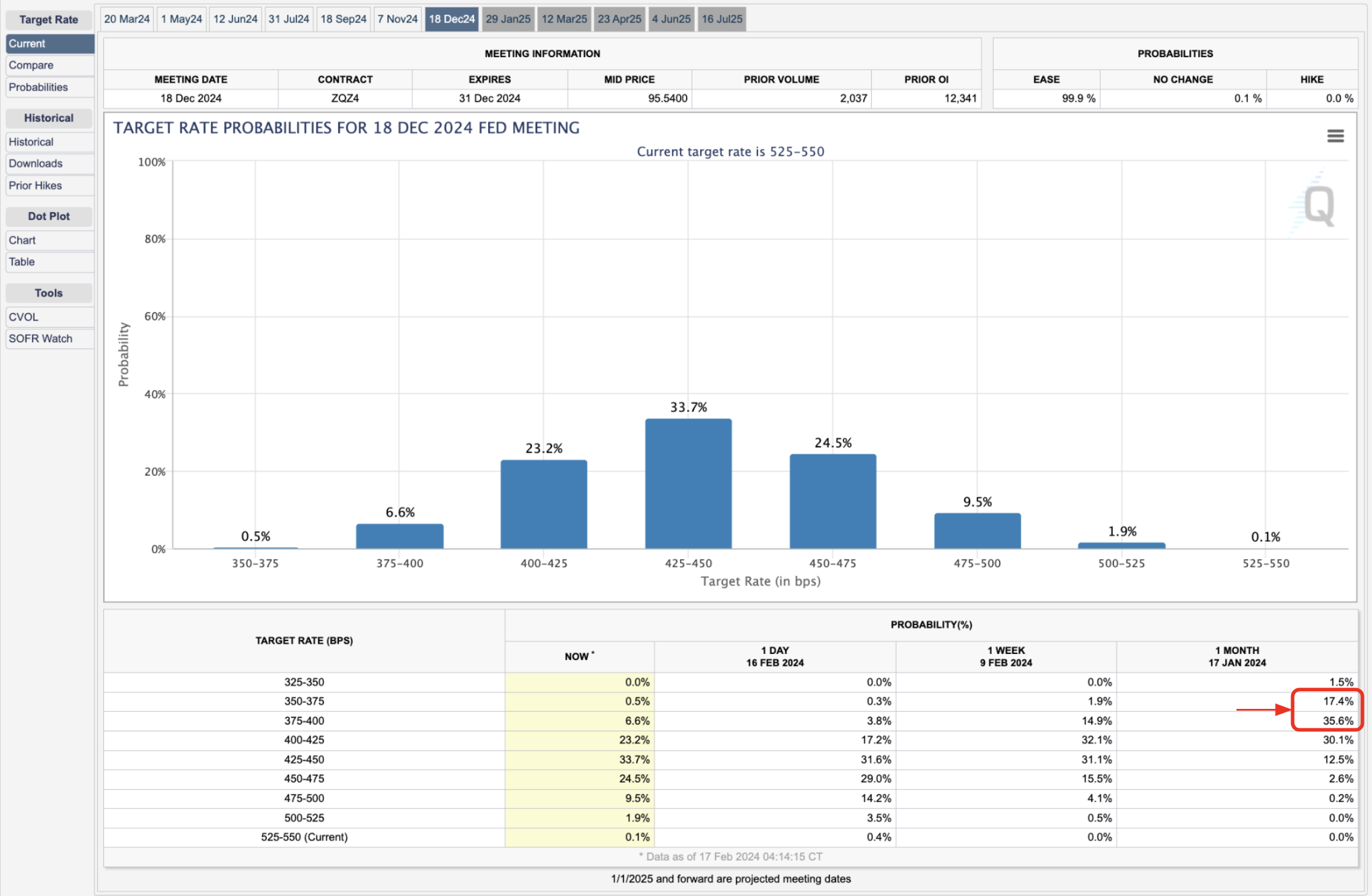

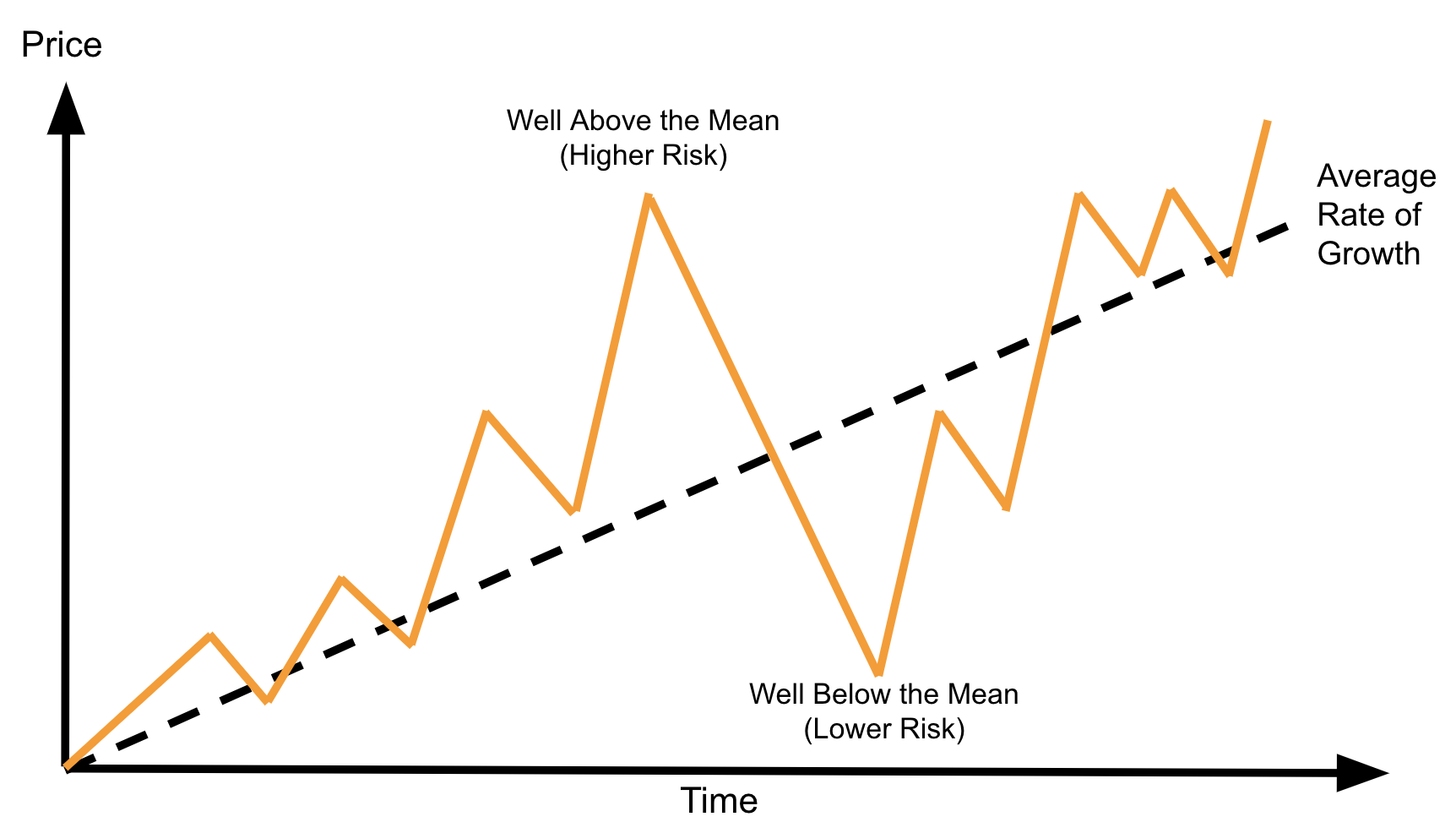

Milton Friedman coined the expression "monetary policy operates with long and variable lags". In the 1970s - he felt it was up to around two years before those effects are felt. Today it's believed to be sooner - given open transparency of Fed speak and data tools available. But is it? It's been two years since the Fed's first hike and we're just starting to see labor markets soften and consumer demand weaken. Have the full effects of tighter policy been absorbed? I don't think so.