How About Zero Rate Cuts this Year?

How About Zero Rate Cuts this Year?

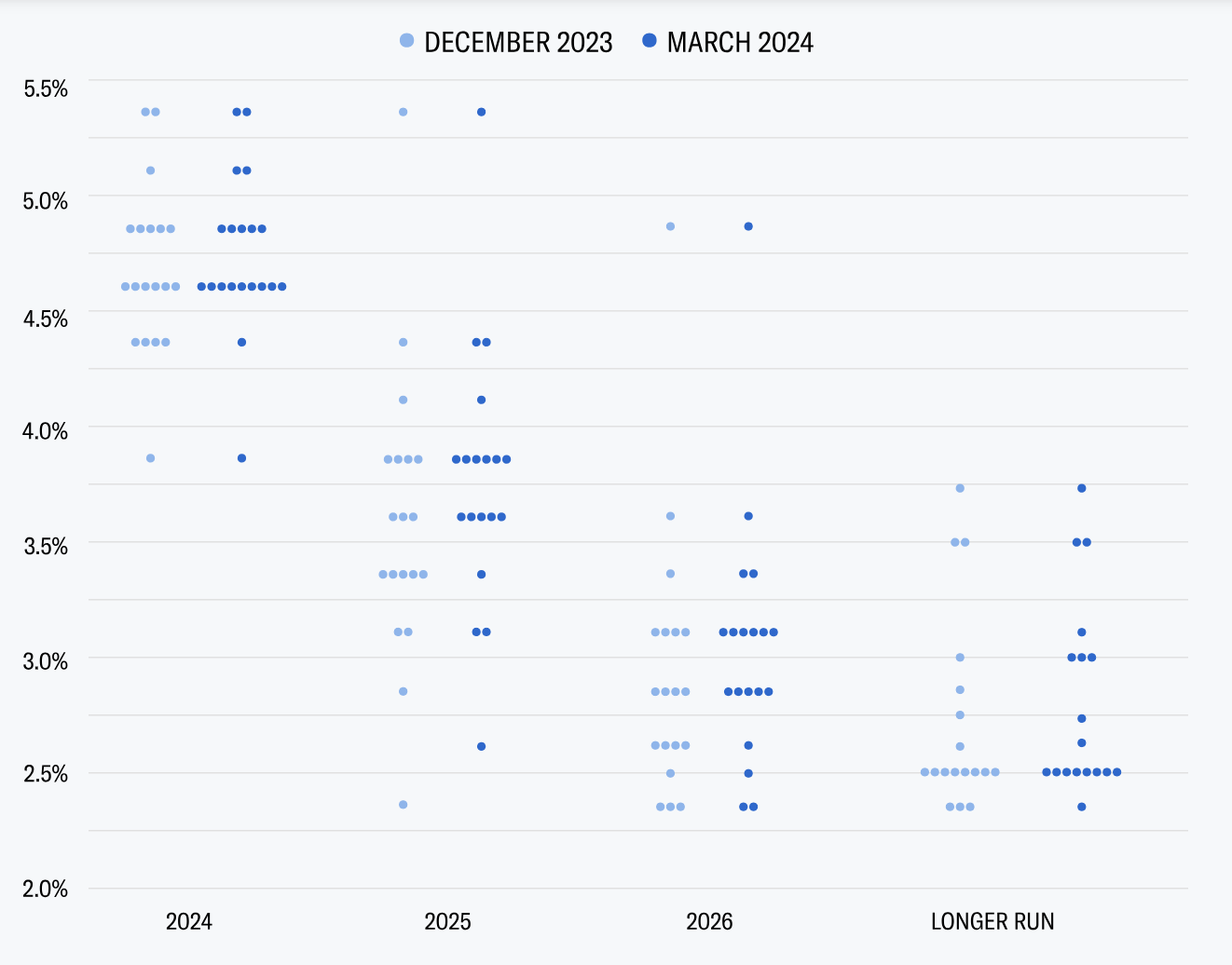

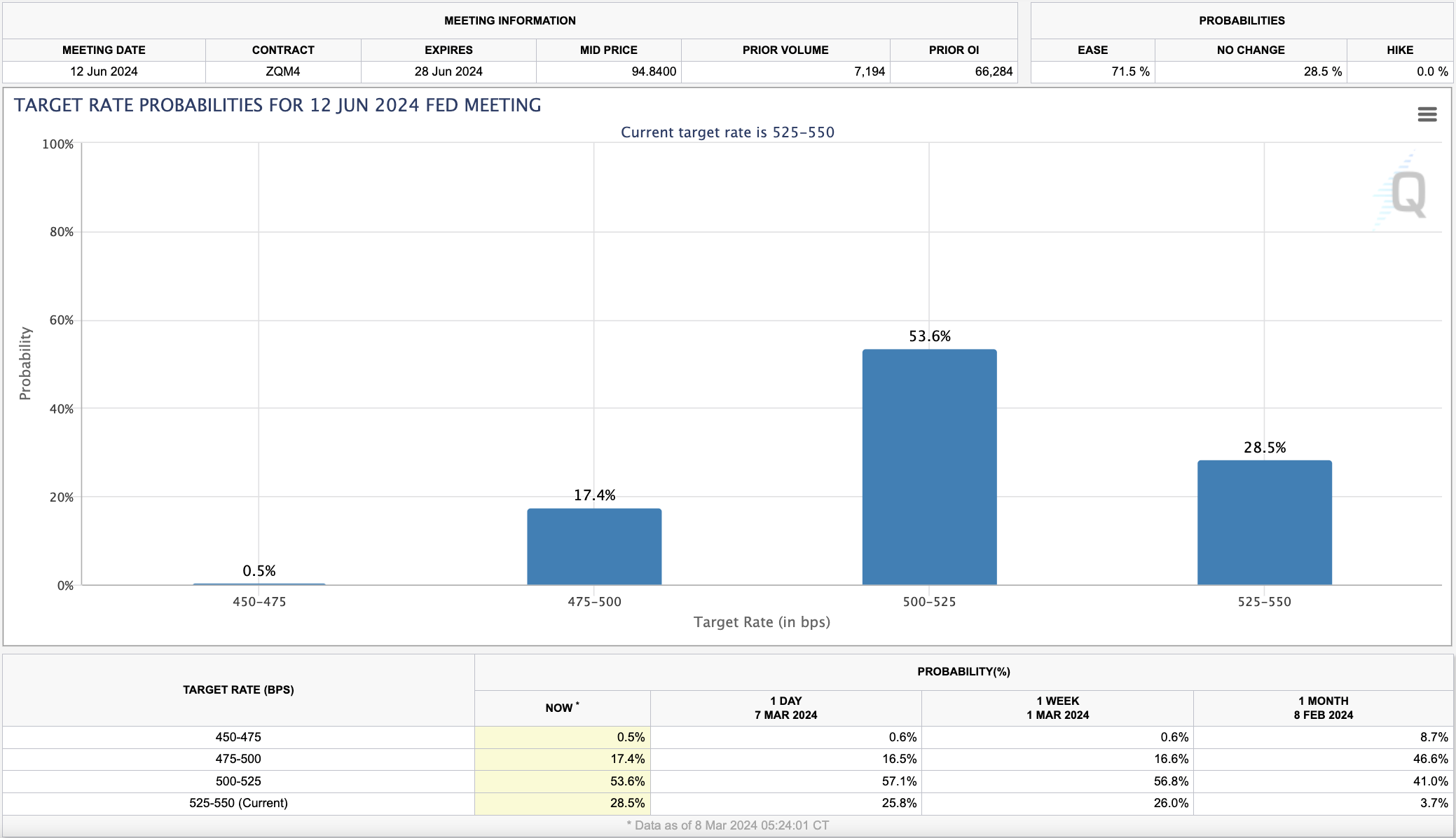

At the time of writing (April 7) - the market is pricing in three rate cuts this year. I don't see it. In fact, I think there is a very good chance of NO rate cuts this year. Now that is not a scenario the market is pricing in. However, with inflation likely to remain stubbornly high - where property prices are not falling - and the labor market remains tight - why would the Fed cut? Let's explore....