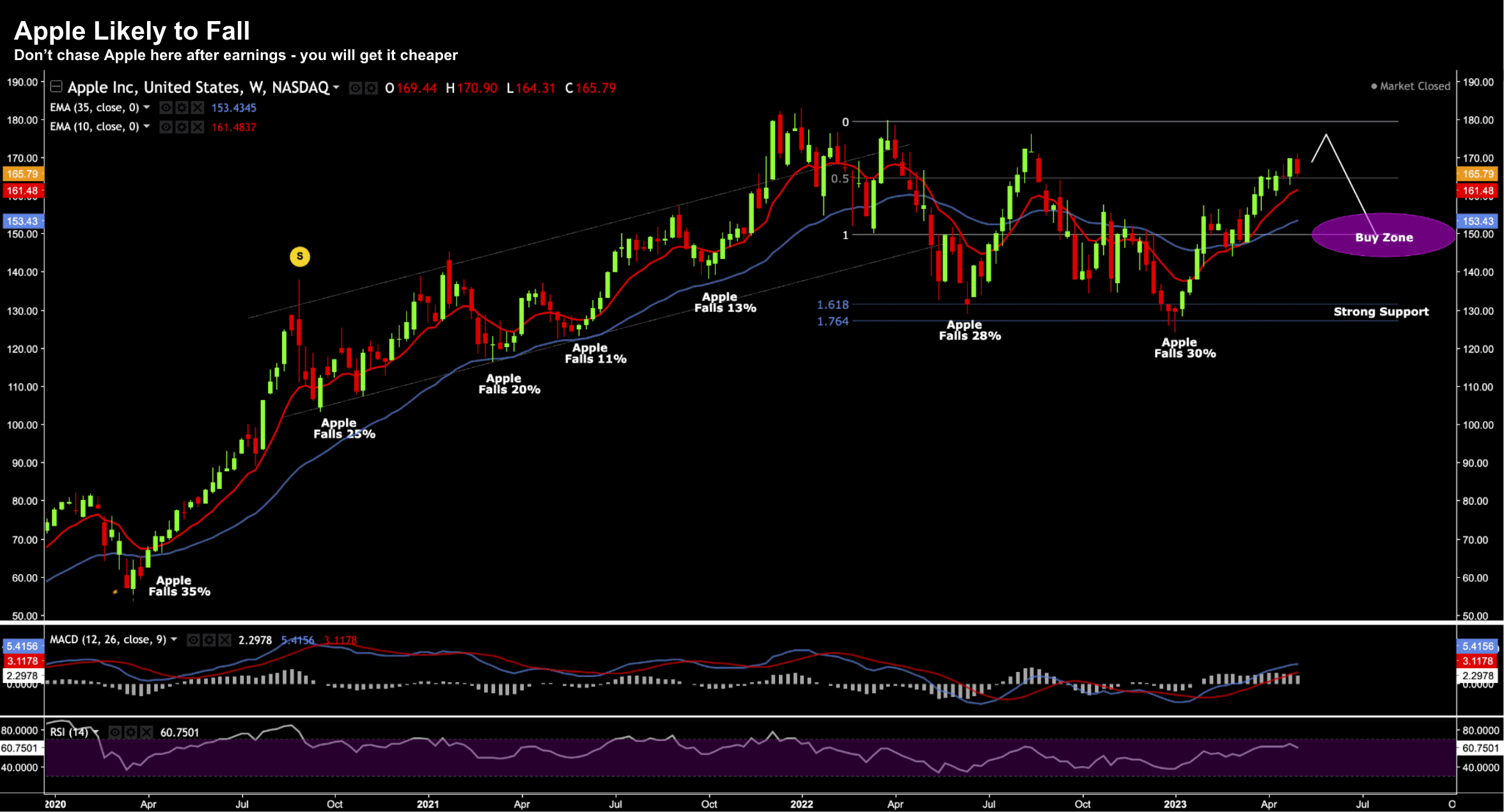

If the Apple Falls from the Tree… Does the Tree Fall?

If the Apple Falls from the Tree… Does the Tree Fall?

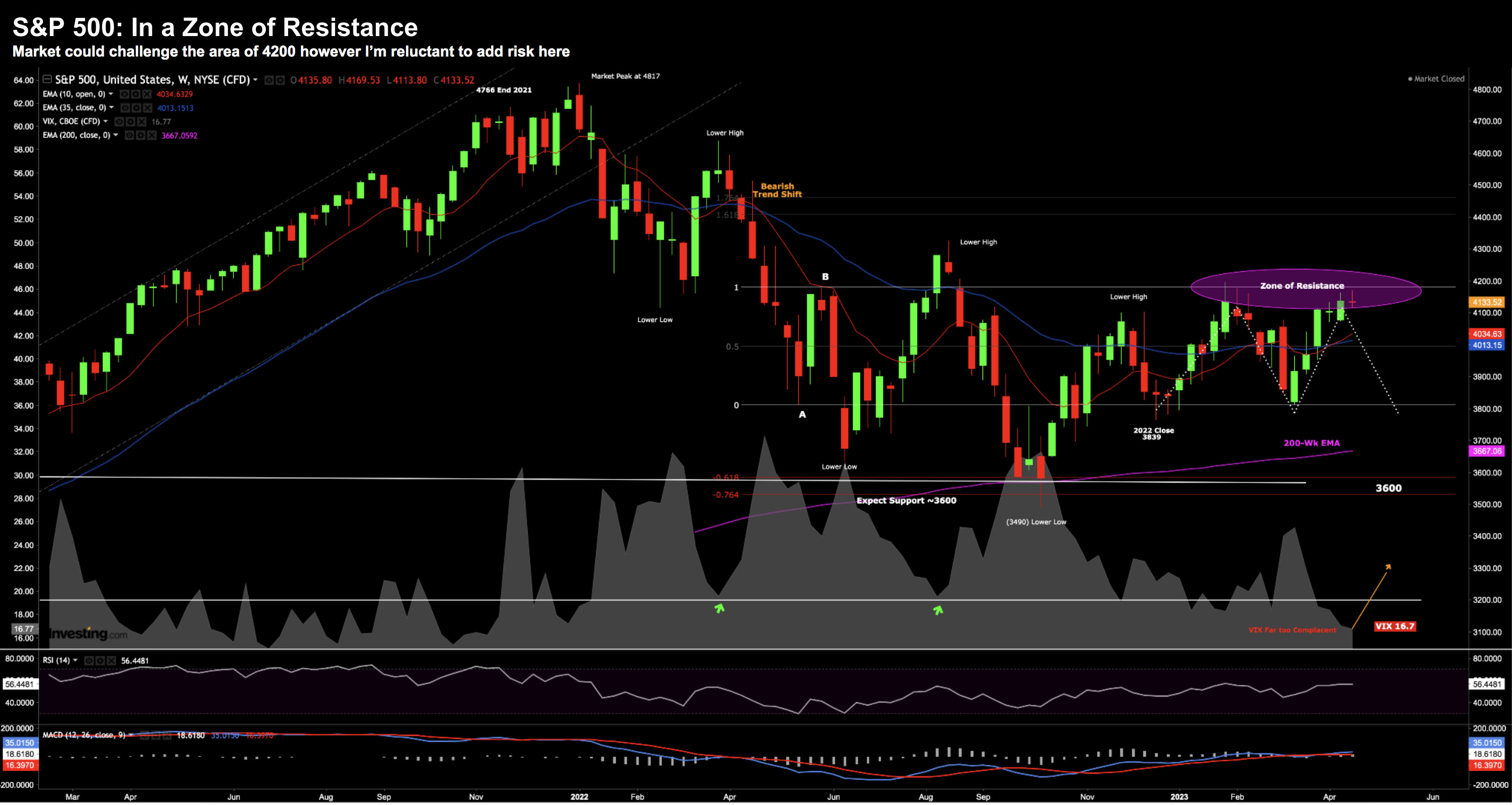

Apple managed to beat very low expectations. However, revenue fell for the second consecutive quarter. Nonetheless, the stock was slightly higher on the news. Consider it a safety trade. More broadly, stocks fell today as they wrestled with the threat of more regional bank failures and a committed Fed. Here's my basic question: will we see three rate cuts before the end of the year? My view is we won't see a single cut (let alone three). If I'm right (and I may not be) - there will be a painful adjustment in the market.