Why Bond Yields and Inflation are Challenging the Rate Cut Narrative

Words: 1,635 Time: 7 Minutes

- How about no rate cuts for the foreseeable future?

- Why headline job numbers are often misleading

- The S&P 500 has lost all momentum at peak valuations

A few months ago, Jay Powell effectively claimed victory over inflation. He indicated that the time had come to start easing rates, initiating a cycle with a 50-basis-point cut followed by subsequent 25-basis-point reductions.

Equity markets were thrilled. The prospect of "cheap money" returning led traders to price in as many as 6 or 7 rate cuts over the following 12 months, driving the market to new heights. But let"s pause and reflect on the necessity of those cuts.

The macroeconomic data simply didn"t scream "emergency." Employment was robust, GDP was expanding at a healthy clip (near 3.0%), consumer spending held up, and corporate net profit margins were hovering near record highs of 12%.

While equity investors were busy celebrating, the bond market was signaling a very different reality. The US 10-year yield moved in the opposite direction, steadily marching higher with the potential to retest the 5.0% mark.

I recently wrote a piece titled "What Could Possibly Go Wrong?", citing rising 10-year yields and a strengthening US dollar as major structural risks. Equities, however, seemed oblivious. The prevailing sentiment was: What risks? Who cares if the 10-year yield hits 5.0%?

This optimism is reflected in Wall Street"s consensus targets, which project the S&P 500 to trade at a lofty forward multiple of 25x, assuming aggressive earnings growth.

| Institution | Index Target | EPS | Fwd P/E |

|---|---|---|---|

| Oppenheimer | 7100 | 275 | 25.8 |

| Wells Fargo | 7007 | 274 | 25.6 |

| Deutsche Bank | 7000 | 282 | 24.8 |

| Soc. Gen | 6750 | 272 | 24.8 |

| BMO | 6700 | 275 | 24.4 |

| HSBC | 6700 | 268 | 25.0 |

| Bank of America | 6666 | 275 | 24.2 |

| ScotiaBank | 6650 | 255 | 26.1 |

| Barclays | 6600 | 271 | 24.4 |

| Evercore ISI | 6600 | 257 | 25.7 |

| Fundstrat | 6600 | 275 | 24.0 |

| Ned Davis Research | 6600 | 254 | 25.9 |

| RBC Capital Markets | 6600 | 271 | 24.3 |

| Citigroup | 6500 | 270 | 24.1 |

| Goldman Sachs | 6500 | 268 | 24.3 |

| JP Morgan | 6500 | 270 | 24.1 |

| Morgan Stanley | 6500 | 271 | 23.9 |

| UBS | 6400 | 257 | 24.9 |

| BNP Paribas | 6300 | 270 | 23.3 |

| Cantor Fitzgerald | 6000 | 267 | 22.5 |

| AVERAGE | 6617 | 268.0 | 24.6 |

Notice how everyone leans to the same side of the boat. There"s rarely a dissenting voice among the major institutions when momentum is strong. This is classic "groupthink"—a psychological tendency where the desire for conformity results in an irrational or dysfunctional decision-making outcome.

Here"s another way to think about the problem: What happens to these consensus targets if the fundamental inputs change? Recent data threw a potential spanner in the works. Headline jobs came in warmer than expected, and inflation expectations have risen from 3.0% to 3.3%.

Given this shift, what if the Fed does not implement a single rate cut in the near future? Would that alter these uber-bullish 25x multiple targets? Furthermore, if the US 10-year yield traded at 5.50% (which is historically plausible), how would that impact the valuation of equities?

Remember: It"s normal for the 10-year yield to trade ~1.25% higher than the Fed funds rate. If the Fed settles its rate at 4.0%, we could easily see the 10-year anchor itself above 5.0%.

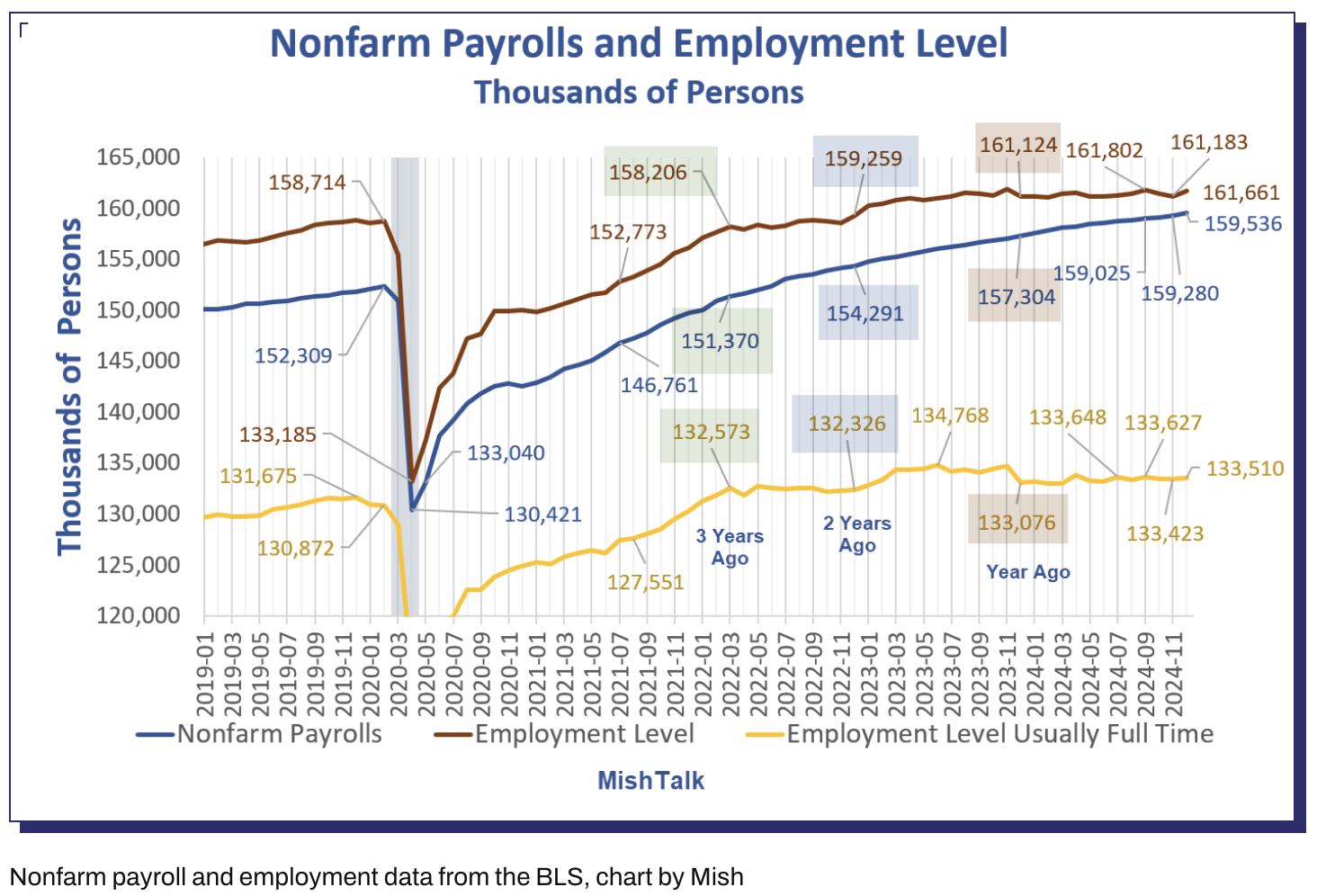

Jobs Data: "Stronger" than Expected?

Before taking headline numbers at face value, I encourage you to read Mish"s blog for a detailed breakdown of the payroll reports. While the headline figure of 256,000 jobs added looks robust, the reality beneath the surface is more nuanced.

Mish points out that half of the jobs added recently came from education, health services, and government. Retail also showed notable gains, but this is highly seasonal around the holidays, and those jobs often disappear in subsequent months.

More importantly, full-time employment has shown persistent weakness. The methodology behind these statistics is crucial. For example, if you work just one hour per week, you are officially categorized as "employed." Furthermore, if you don"t have a job and fail to actively look for one (which requires formal interviews or submitting resumes, not just browsing job boards), you drop out of the labor force entirely and are not considered unemployed.

These definitions can distort the true picture, artificially lowering the unemployment rate and boosting the payroll jobs report. Consider this long-term context:

- Nonfarm Payrolls are up significantly over the last three years.

- But actual employment gains are much lower.

- And crucial full-time employment has barely moved by comparison.

This is a massive divergence between full-time work and headline non-farm payrolls. In fact, since the peak in mid-2023, full-time employment has actually declined.

A Fed on Pause

Regardless of the nuances, the market interpreted the headline jobs number as "strong." Combined with rising inflation expectations, the market is quickly dialing back its bets on imminent, aggressive rate cuts.

Here is how Reuters summarized the inflation outlook:

U.S. consumers expect inflation to increase over the next 12 months and beyond, likely reflecting concerns that broad tariffs on imports… could raise prices for households. The University of Michigan"s survey showed consumers" one-year inflation expectations jumped to 3.3%, the highest level in months.

Investors should reframe the issue this way: Is the market adequately pricing in the possibility of rate increases? Currently, they aren"t on the radar. However, if these inflationary trends continue, the Fed may find itself in a difficult position.

With the benefit of hindsight, one might wonder if the initial aggressive rate cuts were premature. The bond market has been signaling that rates need to be higher, acting as a leading indicator while equities often lag in recognizing structural shifts.

US 10-Year Yield Trends

It is highly unusual for the long end of the yield curve to rally while the Fed is slashing short-term rates. This dynamic, often called a "bear market steepening," typically does not bode well for broader markets. Why?

- As long-term yields rise, borrowing costs increase for businesses and consumers, dampening economic activity.

- Companies with high levels of debt face higher interest expenses, eroding profitability.

- Higher long-term rates generally cause equity valuations to contract, especially for growth stocks, as future cash flows are discounted at higher rates.

We are seeing this play out with certain tech stocks, as their future cash flows are being heavily discounted by the bond market"s reality. All eyes will remain on incoming CPI data. If inflation proves sticky, the market will have to digest the reality of fewer rate cuts than anticipated.

We must also model potential inflationary risks stemming from policies like tariffs, labor market restrictions, and corporate tax adjustments. As I"ve noted before, what could possibly go wrong?

Market Momentum Stalls

Let"s conclude with a technical view of the broader market.

S&P 500 Momentum Indicators

As highlighted in previous posts, the index has met strong resistance at these elevated levels. The technical script remains unchanged:

- The weekly MACD and RSI show strong negative divergence (i.e., momentum is not confirming the price highs).

- The market remains extended from key moving averages like the 35-week EMA.

- Volatility (VIX) is showing signs of waking up, indicating traders are becoming more cautious.

There is technical room for stocks to trade lower, potentially finding initial support near the 35-week EMA. However, true value might require a deeper pullback before it becomes compelling.

Putting it All Together

When markets eventually recalibrate to more realistic valuation multiples, it will be the time to seek out quality. However, this means looking beyond the most hyped sectors.

If we assume a scenario where the 10-year yield remains elevated, perhaps above 5.0%, the future cash flows of high-growth, speculative tech names will be heavily discounted. This is where a disciplined approach is vital.

Instead of chasing momentum, focus on businesses that generate strong, consistent returns on capital over time. The principle of seeking companies with durable competitive advantages—those that can reinvest capital at high incremental rates of return without relying on excessive debt—remains paramount. This is the core philosophy behind focusing on high Return on Invested Capital (ROIC).

Remember: The risk of any investment is intrinsically linked to the price you pay. Knowing where to look for true value, rather than just popular narratives, will be key to navigating the cycles ahead.