Navigating Corrections: Valuation Anchors and the Margin of Safety

Words: 1,724 Time: 8 Minutes

- Why political shocks (like tariffs) are the ultimate test of your investing discipline

- The power of "Inversion" during the largest market washouts

- S&P 500 and QQQ buy zones: How to anchor to valuation, not emotion

From the moment blanket 10% tariffs and "reciprocal levies" hit the wires, we witnessed an immediate exodus from risk assets. The selling was sharp—the kind of violent reaction we hadn"t seen since the pandemic.

But rather than getting swept up in the news cycle or trying to predict the exact macroeconomic fallout, we need to use this as a masterclass in market psychology. When the market breaks, human nature compels us to ask the wrong questions.

Instead of asking, "When will the market rebound?" or "How much money can I make buying this dip?", we must practice inversion.

We should ask: "What actions today will guarantee a permanent loss of capital?"

The answer? Panic selling quality assets at a discount, or blindly catching a falling knife in heavily overvalued sectors without a margin of safety.

Political gambles—like playing a massive game of chicken with the US economy—are inevitable. They remind me of the Australian Treasurer, Paul Keating, in 1990 when he told us this was the "recession we had to have." Many years later, he admitted it was a mistake. Tariffs and trade wars are often a zero-sum game, potentially undoing decades of prosperity.

But should investors be surprised by these fresh taxes and shocks? No. Political risk is always present. The real danger is what these events do to overextended markets.

Less Than Magnificent: The Valuation Trap

For months leading up to this correction, I warned investors to reduce exposure to the market generals (the "Mag 7").

Invert the common thinking: Instead of asking, "Are these great companies?" (they absolutely are), ask, "At what price do these great companies become terrible investments?"

When you have businesses trading at forward PE multiples above 35x, your long-term risk-reward is heavily skewed to the downside. The market was pricing in perfection. When reality hit—whether via supply chain disruptions or slowing growth—those companies shed more than $1 trillion in market cap overnight.

Selling is always much harder than buying. It requires killing your ego. I sold my Apple position at $254 because Ben Graham"s "Mr. Market" was simply offering too much.

Today, even after a historic drop, I am still not a buyer of Apple at $200. I require a margin of safety. I get interested between $160 and $180 (roughly an 18x multiple on $8.17 earnings). At 15x, it"s a steal.

The same discipline applies across the board:

- Amazon: I will start nibbling between $150 and $170 (a forward PE of 19x to 20x).

- Nvidia: Despite the hype, I am less bullish on the eternal growth projections. I want to see the $70 to $80 zone.

The QQQ Setup: Waiting for the Washout

When markets begin to fall, it"s tempting to jump at the first sign of a discount. But let"s look at the technical setup I shared in "Buckle Up Buttercup" before the major downside materialized.

"Timing the market is very difficult to do… Therefore, you may want to establish a third of your ideal position size around today"s level ($472). And from there, if we see the price move lower to the upper trend channel – buy your next third (i.e., $400 to $440)."

Fast forward, and the market generals caved exactly as valuations dictated they eventually would.

Are we ready to back up the truck? Let"s invert again. Is the market completely exhausted of sellers?

If we observe the weekly RSI, we"re at 33.8. To signal a true washout—the kind that provides exceptional long-term risk-reward—we want to see that RSI dip below 30, as it did in late 2022.

S&P 500: Patience Over Panic

If you were over-exposed to stocks, severe red days are agonizing. But if you exercised patience and held cash, these are the days you wait for.

As the saying goes: "You buy when there is blood on the streets – even if some of that blood is your own."

Technically, the S&P 500 confirmed the negative divergence we noted in Markets Hedge as Momentum Wanes. But from a valuation perspective, the index is still overpriced.

If we trade down to the 5,000 zone, assuming earnings of ~$260 per share, that puts us at a 19x multiple. That is still above the 10-year average of 18x. It"s a place to start adding exposure, but the market is not yet fundamentally cheap.

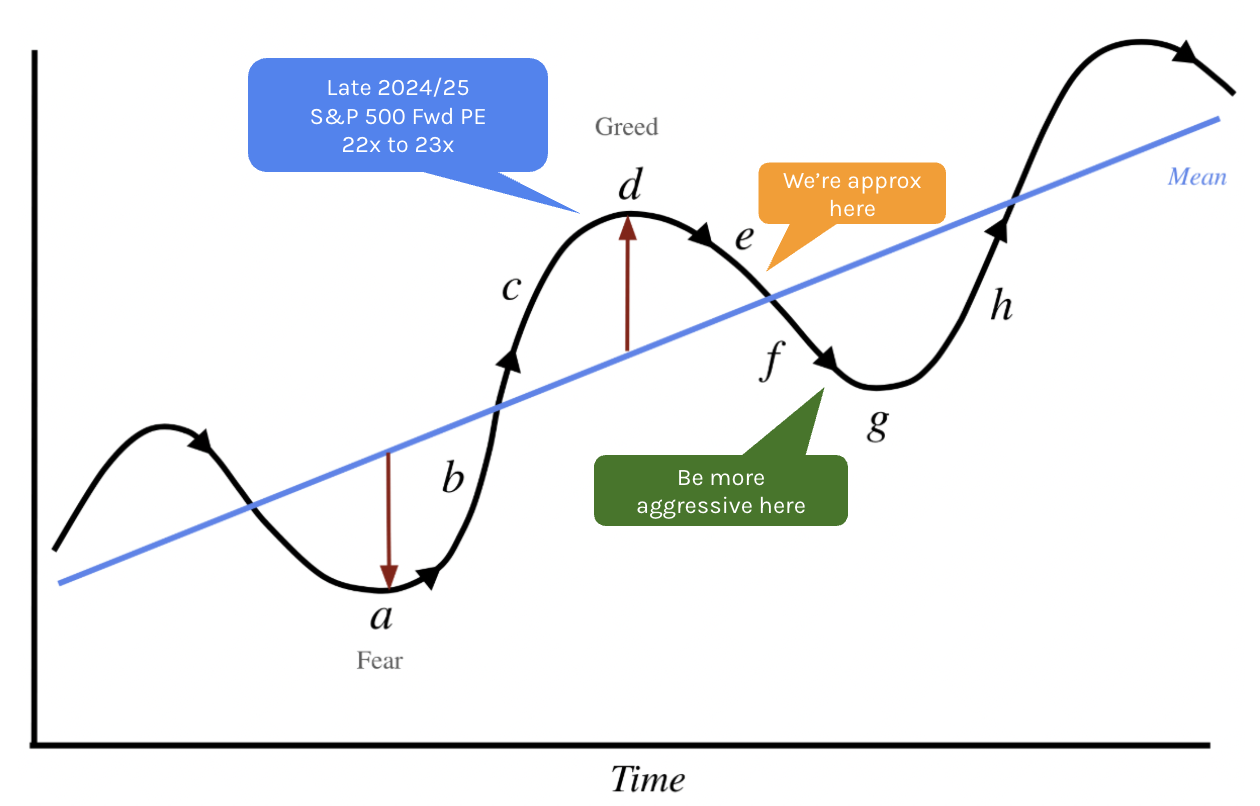

Putting it All Together: The Sentiment Cycle

Investing is a continuous battle between your analytical framework and human emotion. Let"s revisit the sentiment cycle.

We saw peak greed at "d" when the S&P 500 traded near a forward PE of 23x. The market genuinely believed trees could grow to the sky.

We are now moving towards point "e". But true opportunity lives closer to point "f". We want to see the VIX rise from ~21x to spike closer to 35x. We want widespread panic selling.

When that happens, you must have the courage to buy quality at a reasonable valuation. Ignore the instinct to pick the exact bottom. Your preferred quality stock may fall another 20% after you buy it. Use that opportunity to add to the position, provided the fundamentals remain intact.

If you"ve done the work, rely on your framework, sit tight for 3-4 years, and let compounding do the heavy lifting.