Trump’s Push for Lower Rates: Why the Bond Market and a 60% Recession Risk Stand in the Way

Words: 1,900 Time: 8 Minutes

- The Yield Reality: Are bond rates headed for a breakout or a breakdown?

- The Recession Trap: Why lower rates might cost more than they save.

- The $9.2T Refinancing Wall: The massive cost of servicing U.S. debt in 2025.

A familiar tension is returning to Washington: the President is demanding lower interest rates, and Federal Reserve Chair Jay Powell is holding the line. This showdown mirrors the friction of 2018, but the stakes are now significantly higher.

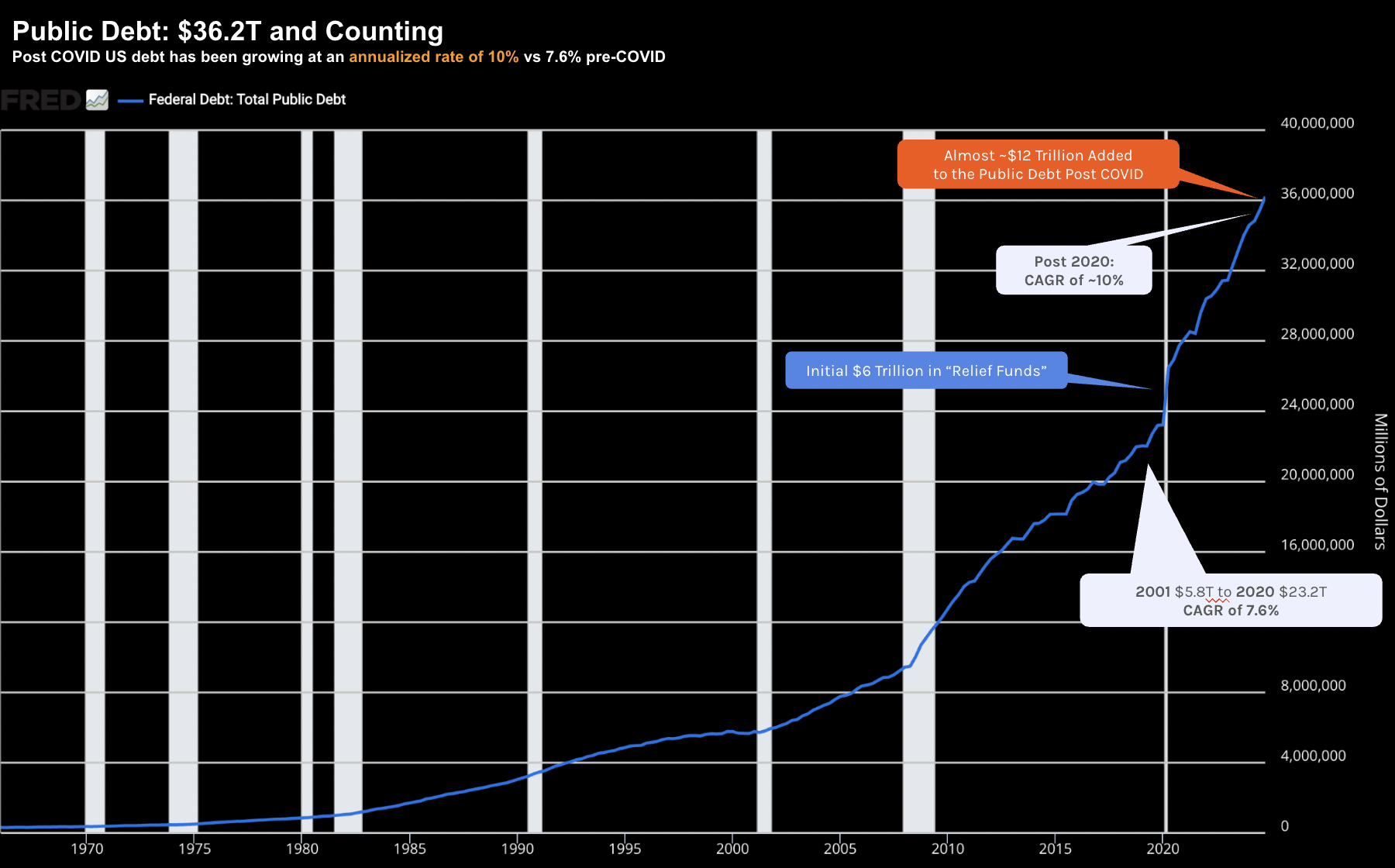

For an administration focused on growth and real estate, cheap money is the primary fuel. However, the macro-environment is flashing a warning sign that cannot be ignored: a national debt totaling $36.2 Trillion, coupled with a federal deficit of $1.9T (roughly 6% of GDP).

Fiscal Reality: April 17, 2025

While cost-cutting measures are a step in the right direction, the U.S. faces a massive immediate hurdle: refinancing approximately $9.2 trillion in debt this year alone. This represents over 25% of the total national debt. With roughly $6.5 trillion due in the first half of the year, the "benchmark" for success is the U.S. 10-year yield.

Much of this debt was originally issued during the era of near-zero rates. Today, with the 10-year yield hovering around 4.32%, the cost of rolling over that debt is soaring. Ironically, aggressive policy shifts are the very thing driving investors to demand higher yields as they weigh the risks of U.S. assets.

Why the Fed is Staying the Course

Despite political pressure, Powell has maintained that the Fed is in no hurry to cut rates. The central bank is adopting a "wait and see" approach to determine how new trade policies will impact the broader economy.

If universal tariffs are implemented, even at a 10% floor, we should expect the prices of goods and services to climb. This creates a perfect storm for inflation. Powell has been clear that his primary obligation is ensuring that a one-time price increase does not spiral into a persistent, ongoing inflation problem.

"Import taxes will probably lead to at least a temporary rise in inflation… our obligation is to make certain that a one-time increase does not become an ongoing problem." — Jay Powell

The Yield Breakout: A Structural Threat

The move in the 10-year yield from below 4.0% toward 4.50% is a signal that the market is reassessing the quality of U.S. government debt. When yields rise, the "gravity" of higher rates pulls down everything from corporate borrowing to home mortgages.

Market Benchmark: April 17, 2025

This is arguably the most important chart for the year. It dictates the opportunity cost of capital and defines the limits of government borrowing. We are also seeing technical pressure from the unwinding of "basis trades"—where hedge funds are forced to sell Treasury bonds to meet margin requirements, further pushing yields higher.

If the 10-year yield breaks above 5.0%, it is highly likely the Fed will be forced to step in as a "buyer of last resort" to prevent a complete freeze in the credit markets. Over the long term, erratic trade flows risk reducing the global appetite for U.S. debt, a structural shift that could keep rates higher for longer.

The Recession Paradox

There are two primary paths for bond yields from here: they either push higher due to inflation and bond selling, or they drop because the U.S. enters a recession. Currently, the probability of a recession is tracking at 60%.

While a recession would naturally lower interest rates and make that $9.2 trillion refinancing cheaper, it is a classic "be careful what you wish for" scenario. Lower borrowing costs are a cold comfort if they are accompanied by job losses and shrinking incomes.

Analysis from Apollo"s Torsten Slok highlights this trade-off: a 2% drop in rates might save the government $500 billion in interest, but the resulting recession would likely crater tax revenue and spike unemployment costs, leading to a $1.3 trillion net erosion of the budget.

In short, you cannot fix a deficit by crashing the economy. The "income" side of the ledger matters just as much as the "interest" side.

Equity Outlook: Mapping the Downside

Looking at the S&P 500, the technical script remains intact. We saw the index catch a bid around the 4,900 to 5,000 zone, but the 5,700 level remains a heavy ceiling of resistance. While volatility (VIX) has cooled to 29x, uncertainty is the dominant theme.

Technical Resistance: April 17, 2025

If we apply a "path to failure" analysis to current valuations: Consensus estimates of $275 EPS are likely too high if a recession materializes. A 15% drop in earnings would bring estimates closer to $230 or $240.

Applying a standard 18x multiple (within our 15x-20x guardrail for moated assets) to those revised earnings gives us a price target of ~4,320. This is why the current 5,000 level is only an "initial" entry point. A drop to 4,300 would represent the opportunity to build full, long-term positions.

Strategic Summary

The direction of the economy rests on whether trade policy continues to challenge the global order. The damage to business confidence may already be done. J.P. Morgan notes that the current tax hikes on U.S. households—driven by tariffs—represent the largest increase since World War II.

While the market hopes for a "soft landing," recessions are notoriously unpredictable. If the downturn mirrors the severity of 2008, the correction could be far more significant than the current 10-15% dip.

Stay within your areas of expertise: keep a close eye on bond yields as your primary indicator, and maintain the patience required to wait for the market to offer true fundamental value.