The Key to Growth: Business Investment

The Key to Growth: Business Investment

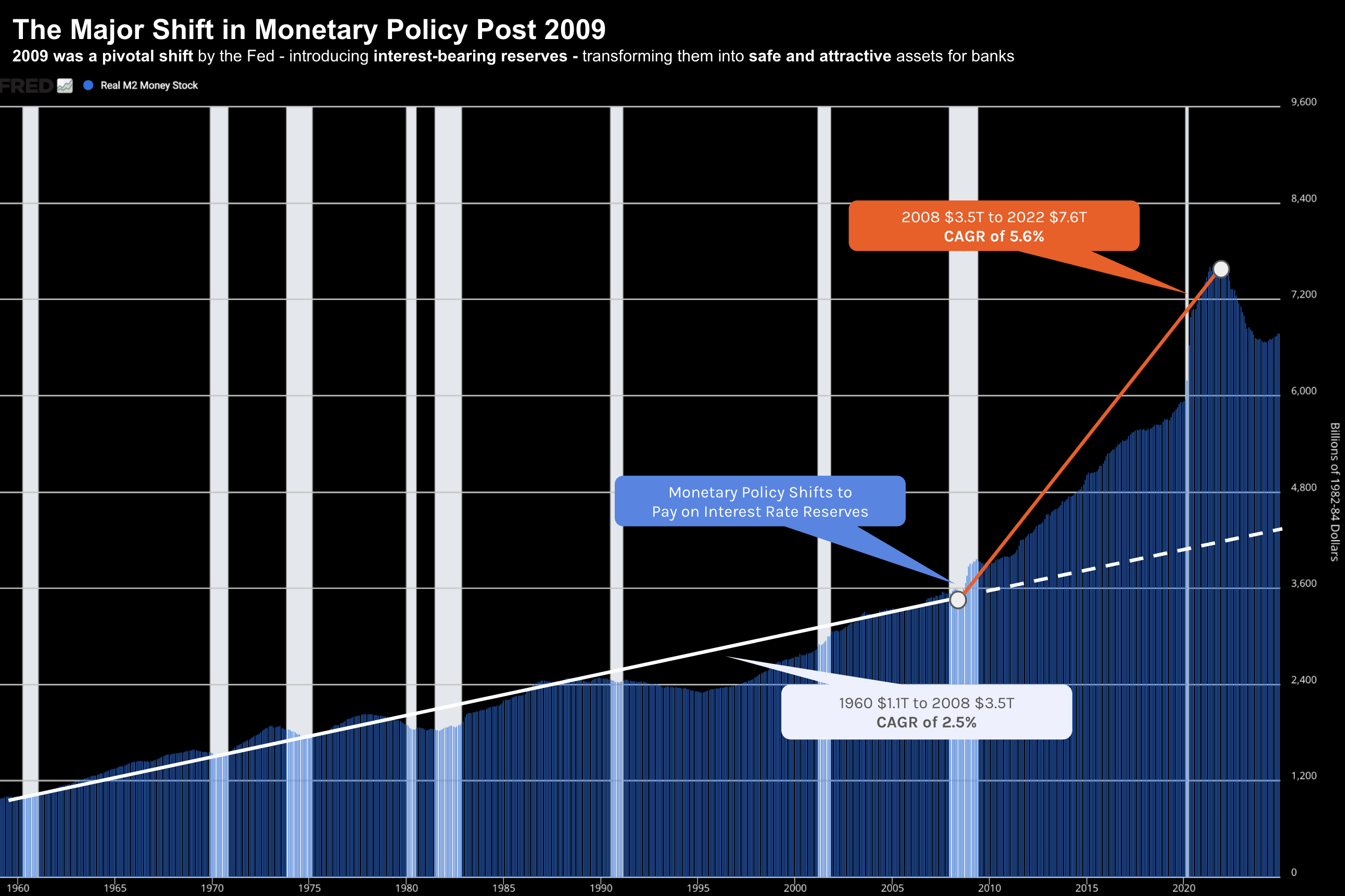

With 10-year yields trading around 4.50% (with the possibility to go higher) - why haven't equities sharply corrected? It's a good question. For e.g., on the surface, one might think equities would struggle given the zero risk premium investors are receiving. But that has not been the case. The stock market has withstood the sharp rise in bond yields (for now anyway). However, I believe there is a simple explanation. It's the amount of liquidity in the system. Liquidity is abundant - evidenced by the very low credit spreads in the market (participants see very little risk). Generally credit spreads widening are your first sign of trouble.