Baby QE & Fed Group Think: Why 23x Forward Earnings Signal a Decade of Zero Returns

Baby QE & Fed Group Think: Why 23x Forward Earnings Signal a Decade of Zero Returns

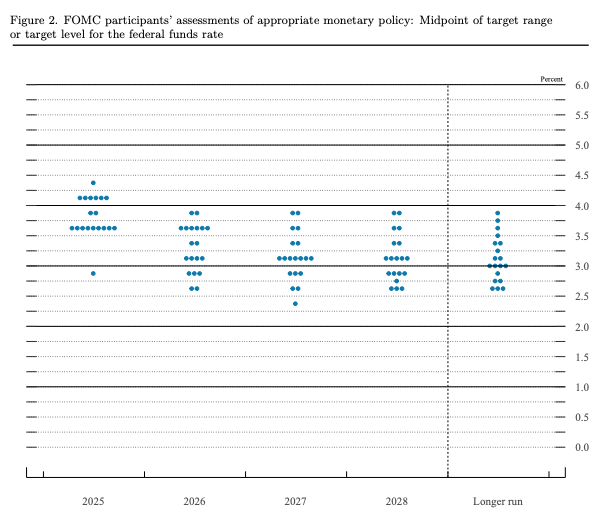

The Fed just delivered a "Christmas gift" with a 25bps cut to 3.75% and a surprise $40B monthly balance sheet expansion—essentially "Baby QE." While markets hit record highs, FOMC "group think" may be masking a deteriorating labor market and looming 2026 tariff inflation. With fwd PEs at ~23x, history warns that subsequent 10-yr returns are often near zero.