Are Recession Callers Back-peddling?

Are Recession Callers Back-peddling?

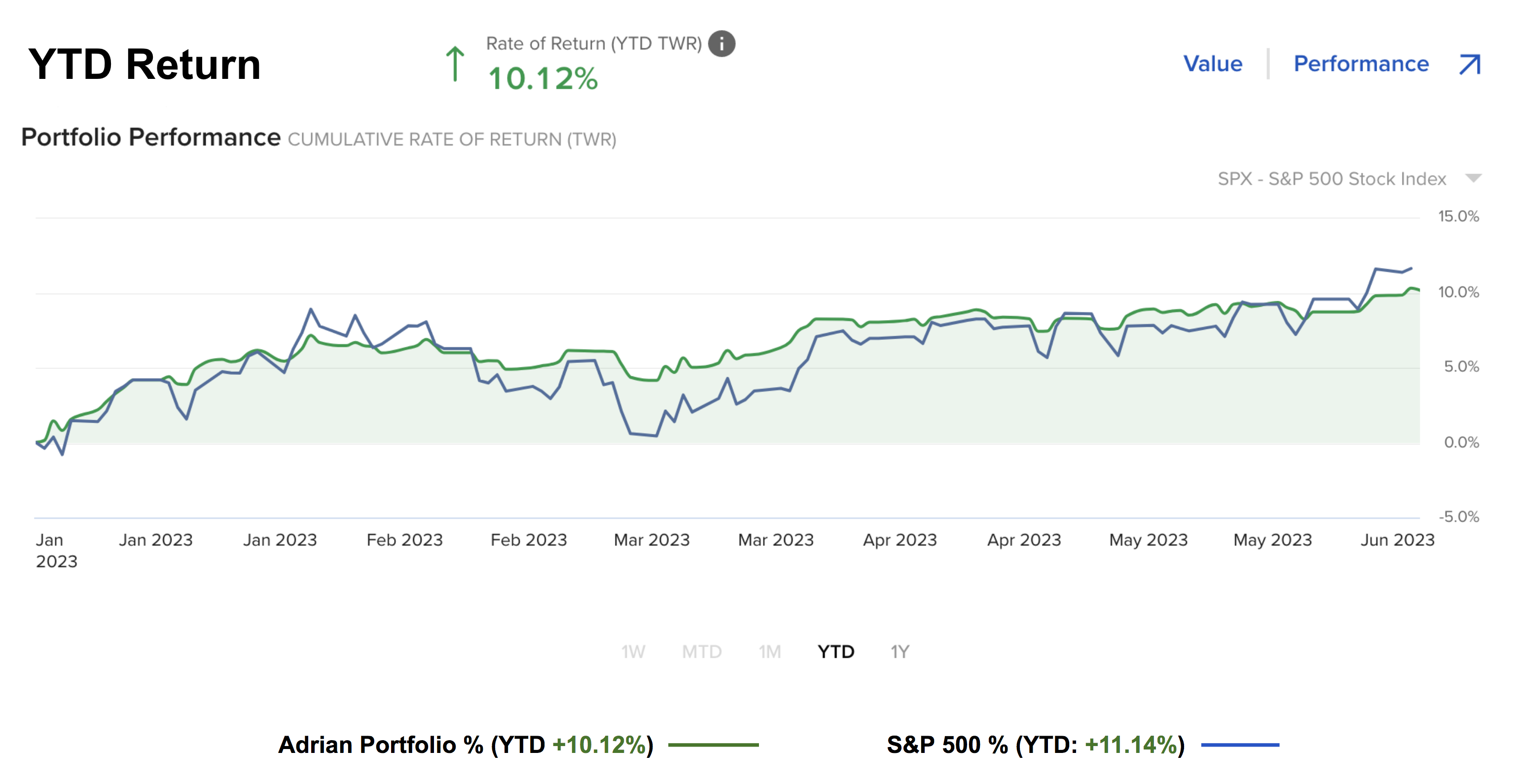

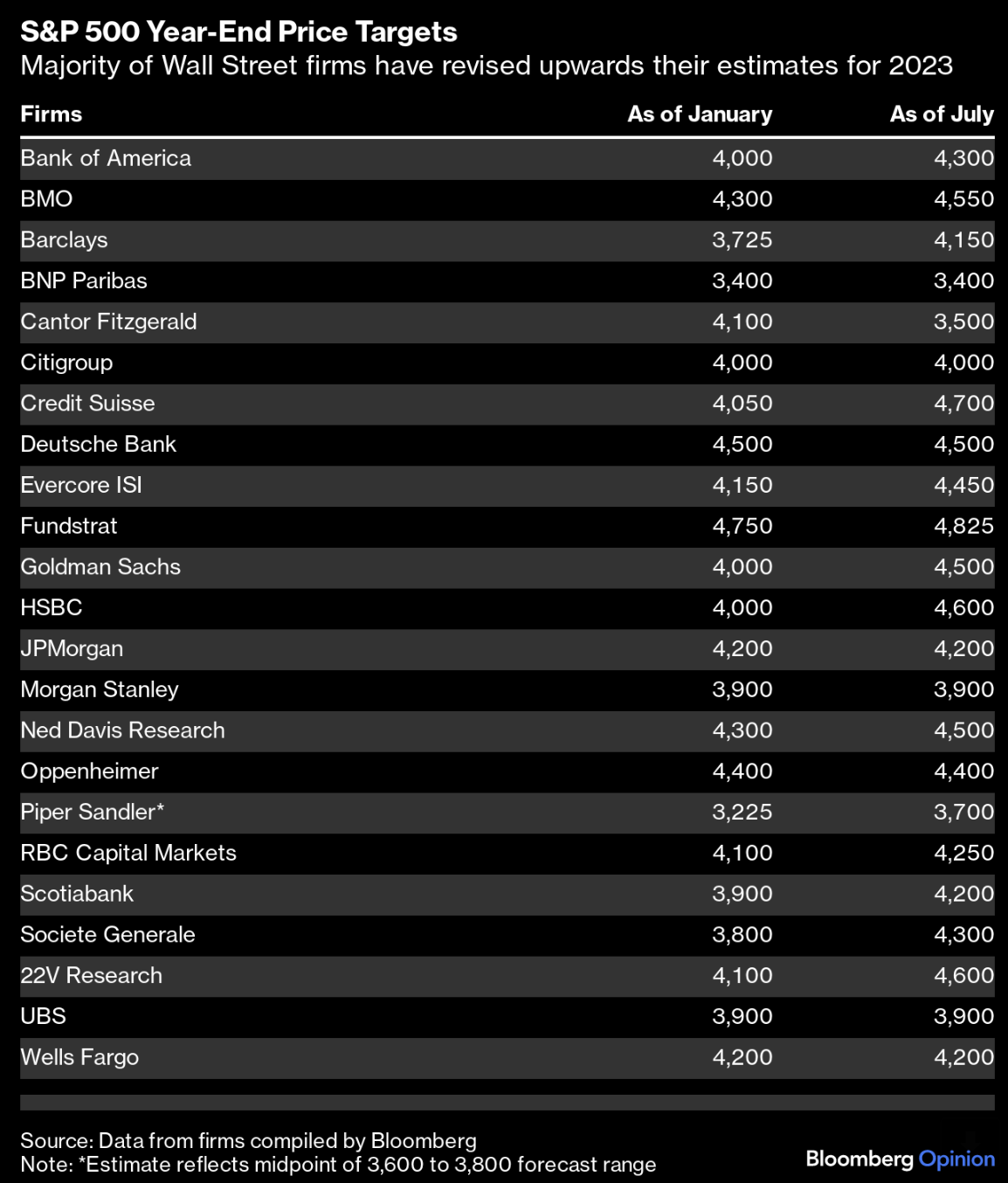

It's the rally everyone loves to hate. Why? Because very few got it right. Most fund managers missed this rally entirely... thinking it was only a matter of time before things collapsed. The thing is - they haven't. I will admit - I also got this wrong. My initial target at the start of the year was 4200. If that broke - I was looking at resistance around 4500. The S&P 500 now trades 4536 - making me look foolish (and it won't be the last time I am sure). We're now just past the mid-point of the year - with the S&P 500 up 18.2% YTD. Remarkable by any measure. What are Wall St saying about the second half?