Beware the “Bear Steepening” of the Curve

Beware the “Bear Steepening” of the Curve

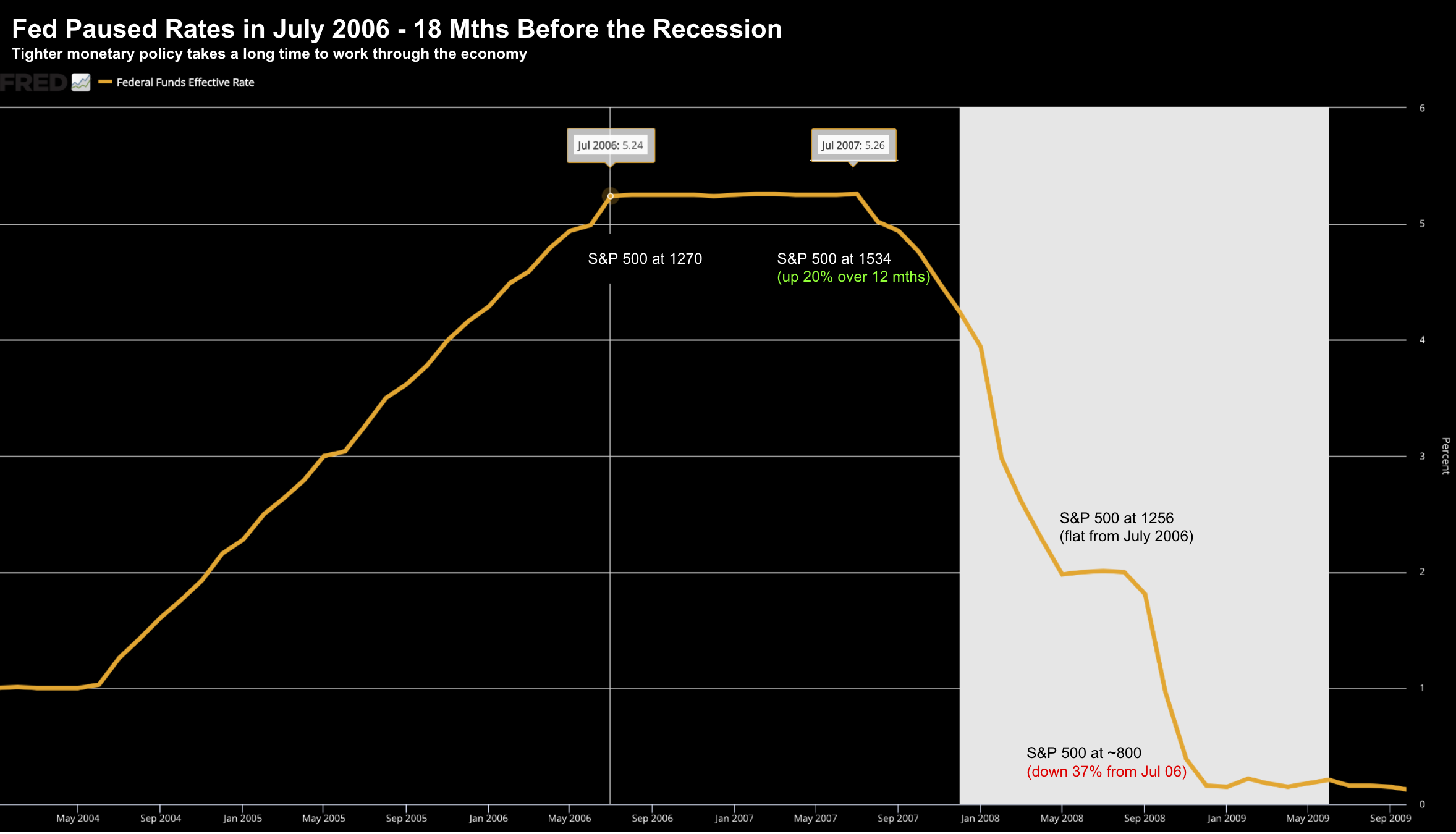

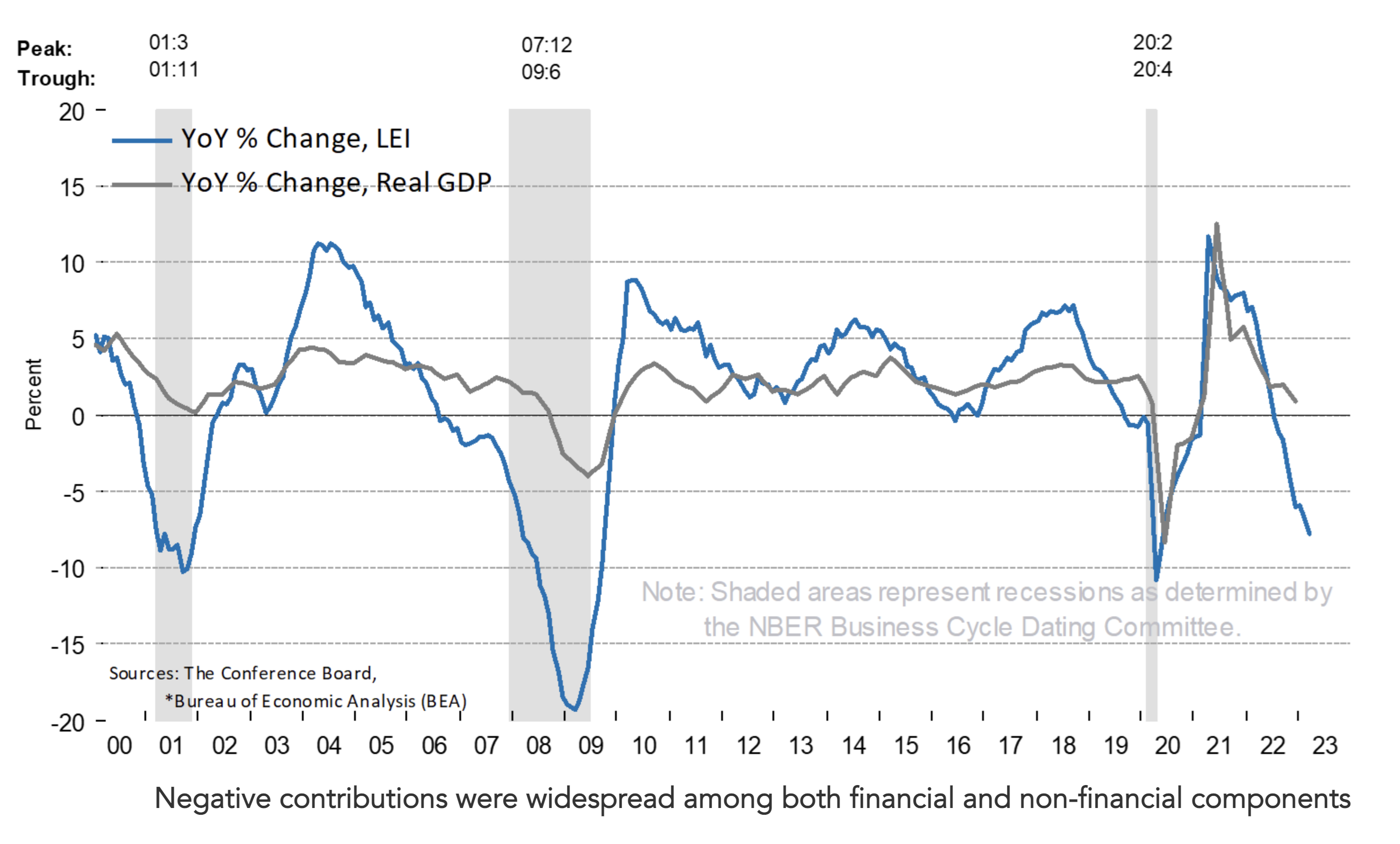

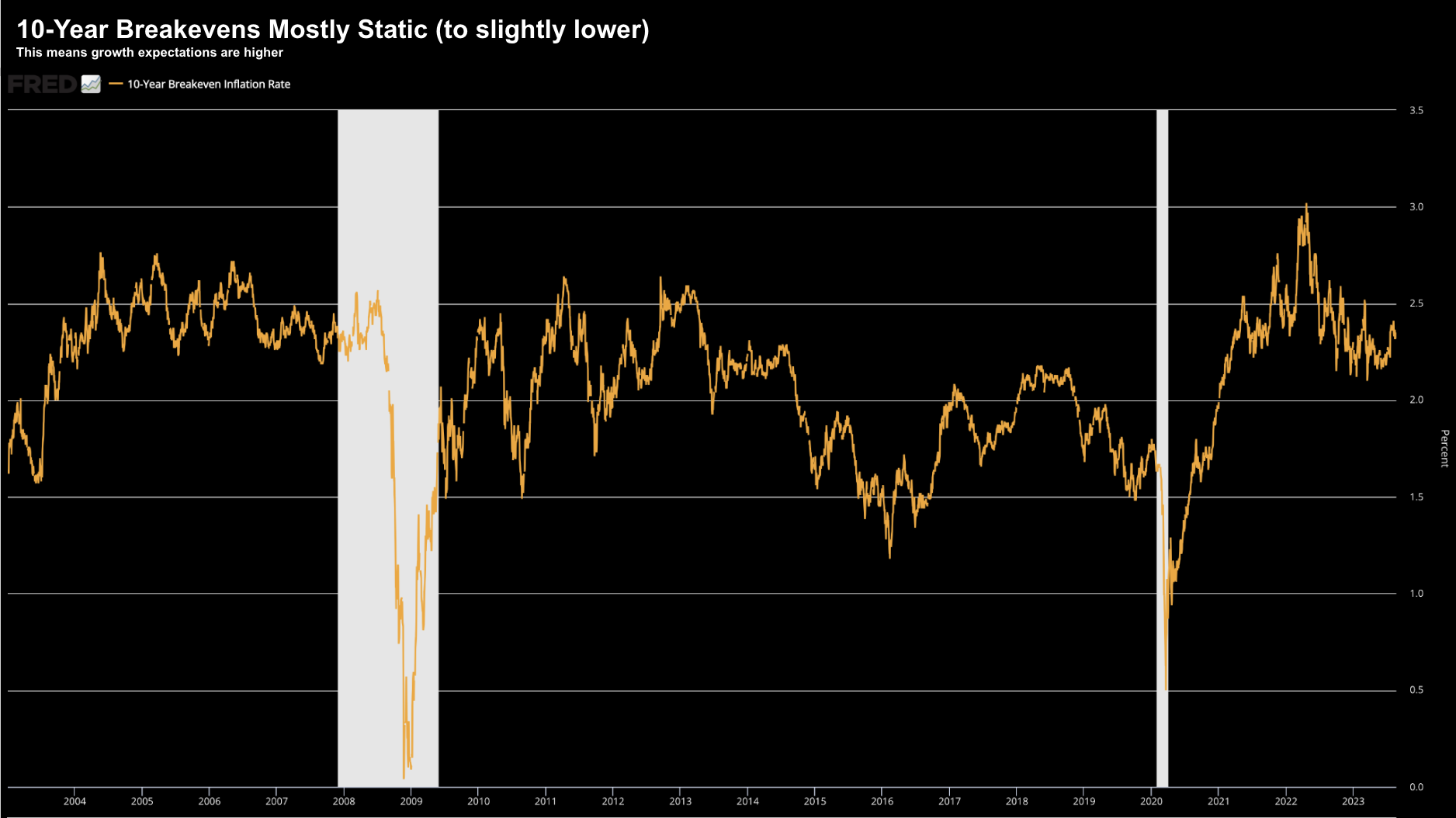

My last post talked about how the market is now taking its cues from bond yields (less so the Fed) Don't get me wrong... what the Fed does (or says) matters. We will hear more from Chair Jay Powell at the end of the week. Expect hawkish tones. To recap on what I shared earlier this week - globally long-term bond yields trade at their highest levels in 15 years. However, what's interesting is the shorter-end (e.g. 2-year and below) is not keeping pace. This has net the effect of "steepening" the all-important 10/2 yield curve. Question is - will that be a problem? History may offer some clues.