One Case for Bond Yields Falling in 2024

One Case for Bond Yields Falling in 2024

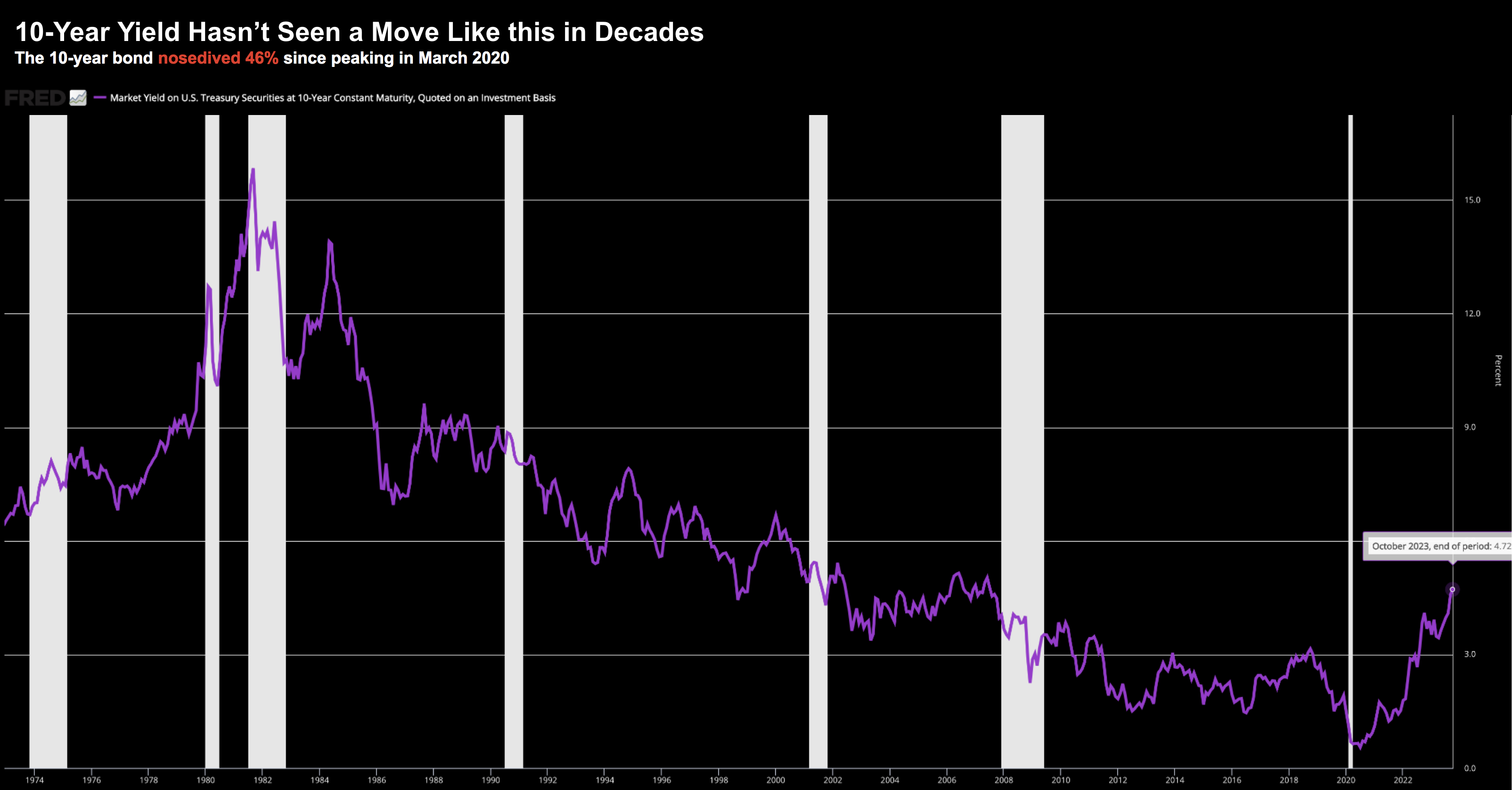

It's been a horrible 3-years for bond / fixed income investors. In short, they have been slaughtered as yields shot higher. For example, losses in long-maturity bonds (e.g. greater than 10 years in duration) are close to historical levels. Consider the all-important US 10-year treasury.... an asset which underpins every financial asset. It has plunged 46% since peaking in March 2020. Put another way, these yields went from ~0.5% at their lows to ~4.8% last week. What we've seen in the bond market is one of the most severe market crashes on record. 30-year bonds have plunged ~53%. As a parallel, the equity market crashed 57% during the 2007-09 financial crisis