Lesson: Don’t Try and Pick ‘Tops or Bottoms’

Lesson: Don’t Try and Pick ‘Tops or Bottoms’

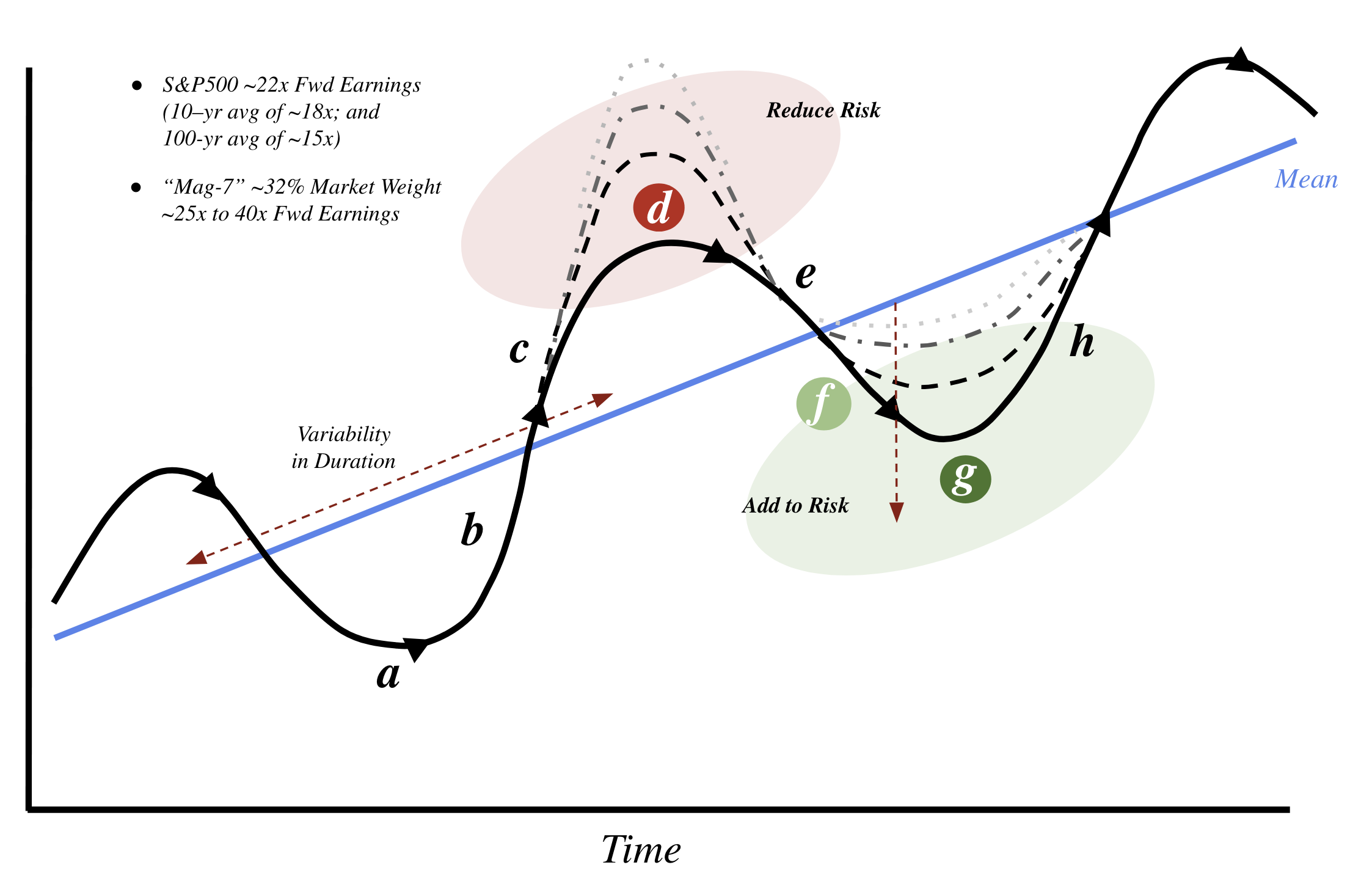

Everyone makes mistakes. In fact, I love 'collecting' mistakes - whether they are my own or from someone else. It's the only way I learn. This post shares two 'mistakes' from a popular media personality. His name is Jim Cramer who hosts a show called "Mad Money". Earlier this week he said "the bottom is in for CrowdStrike". Big call given recent events. Fast forward a few days and the stock is 16% lower than when Jim called the bottom. So what can we learn from this?