What Does Kolanovic See That Others Don’t?

What Does Kolanovic See That Others Don’t?

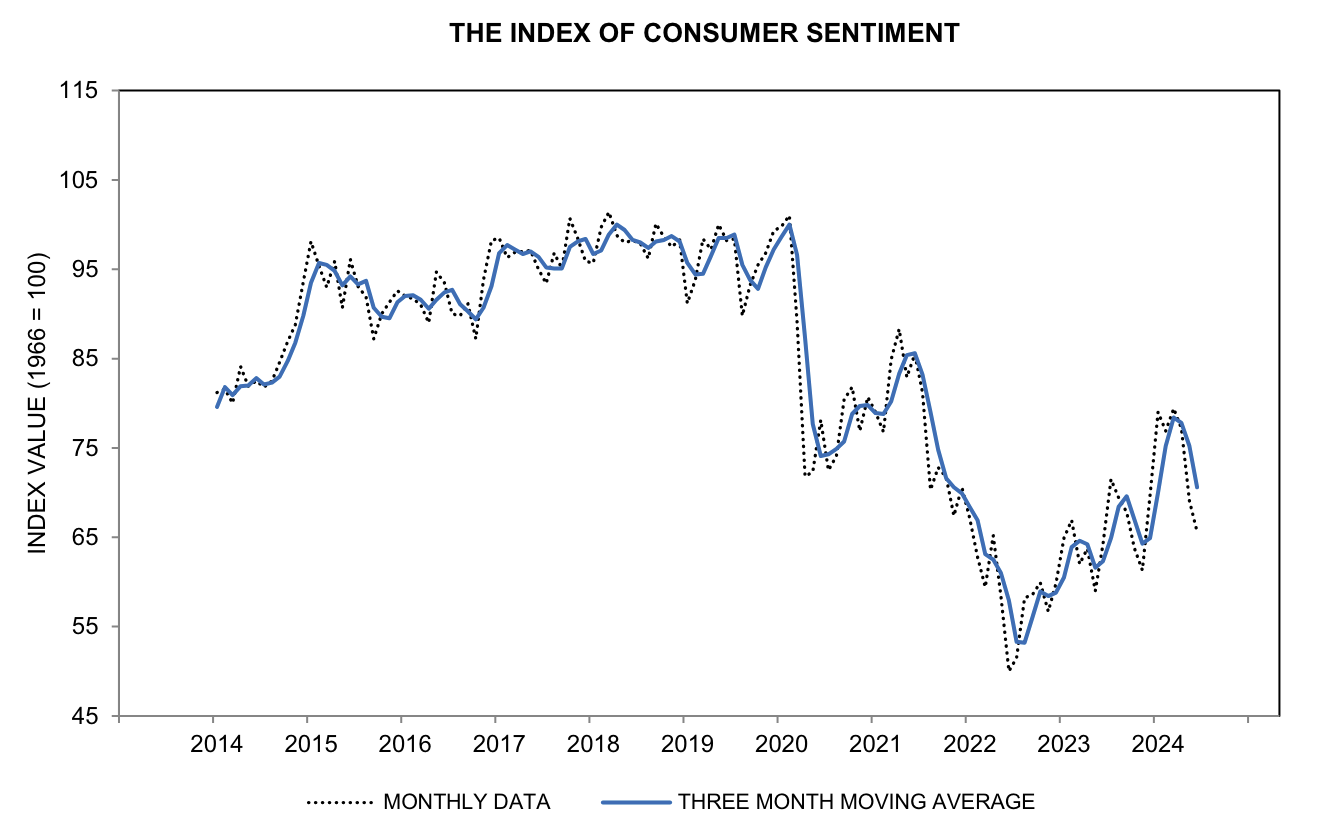

Most analyst year-end S&P 500 targets range from 4200 to 5600 for equities; and 3.00% to 4.75% for 10-year yields. My guess is we will land somewhere in between these zones. On the whole, it's fair to suggest Wall Street feels 'comfortable' with holding equities. Consensus year end targets average 5400 - which tells me most don't expect stocks to do much between now and year's end. More important - they don't expect stocks to lose any ground. This post expands what I think is the single most important variable (and risk) with these forecasts: the relative health of the US consumer and their ability to continue spending.